Change State is now part of Recruitics! Learn more

Subscribe to get more insights

Happy New Year!

Happy New Year!

We hope you enjoyed your end-of-year celebrations and are looking forward to a fantastic 2024 ahead! Now is the time we typically take stock of things we’d like to leave behind in 2023 and set intentions or goals for the year ahead. If you’re still looking for inspiration, check out NPR Life Kit’s interactive guide to planning a resolution this year, or sign up for a 6-day Energy Challenge to explore some attainable ways to feel better in 2024. Already locked in on your targets for the year? Then have some fun exploring predictions on trends for the months ahead from NPR, The New York Times, The Washington Post, or The Wall Street Journal.

On that note, if you have any feedback on what else you’d like to see from this newsletter this year, I’m all ears. Send me a note to let me know your thoughts!

Cheers,

Nicole

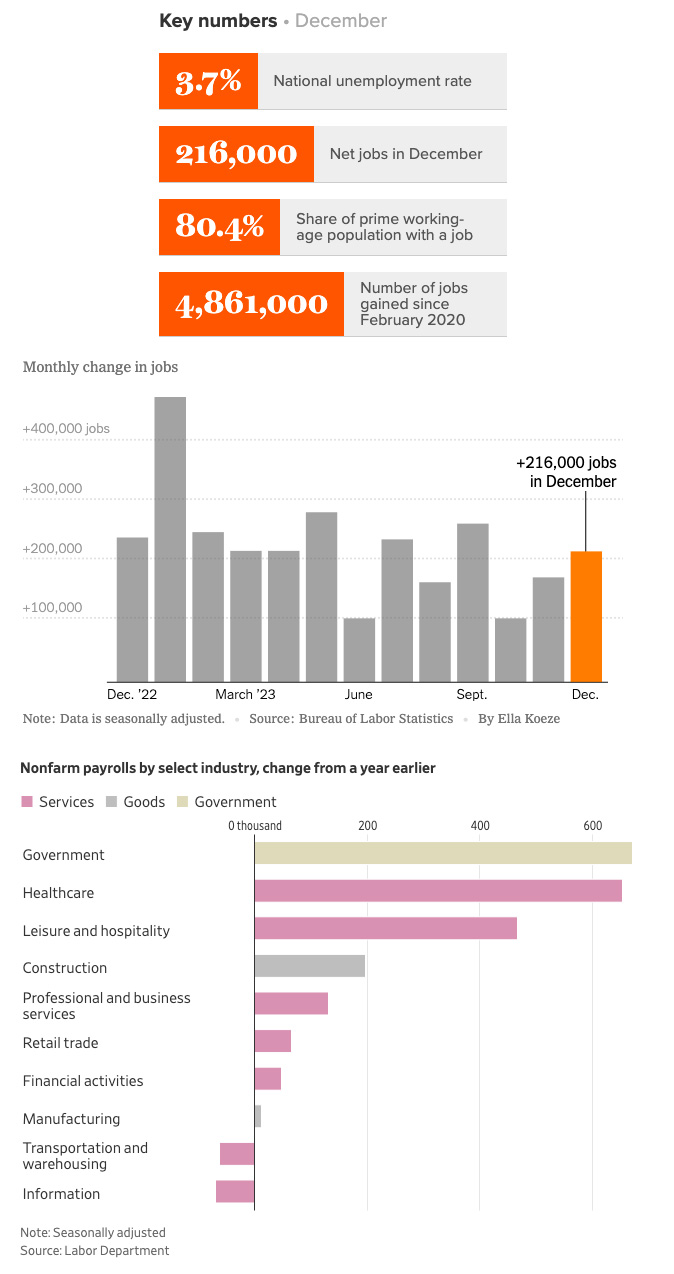

2023 came to a strong close, with December beating general predictions and adding 216,000 jobs, the most in the last three months. November and October’s numbers were revised lower by a combined 71,000, though a relatively modest reduction. The unemployment rate held steady at 3.7%, against expectations for a rise to 3.8%. Employers added 2.7 million jobs last year, decelerating from the 4.8 million added in 2022, yet still higher than in the years immediately preceding the pandemic. Following these generally healthy numbers, we once again note a divergence in the data in the household survey, with employment dropping by 683,000 and LFPR slumping to 62.5%, the lowest level since February.

December’s payroll gains were primarily monopolized by three categories: education and health, leisure and hospitality, and government, with more than half of last month’s gains coming from healthcare and government alone. Healthcare hiring continues to accelerate as market forces such as the aging of the U.S. population and Covid-19 fuel demand. Meanwhile, leisure and hospitality have maintained the highest hiring rate among all industries since 2020 and are slowly inching closer to their pre-pandemic levels. However, even though job growth continues to be promising, its concentration in just a few industries across 2023 is a likely sign that the labor market is beginning to lose some steam. December recorded further job losses in the transportation and warehousing industry and saw temporary help services cut 33,000 jobs. As we’ve discussed before, temp help services can often be the canary in the coal mine for broader changes ahead as companies attempt to avoid laying off permanent staff.

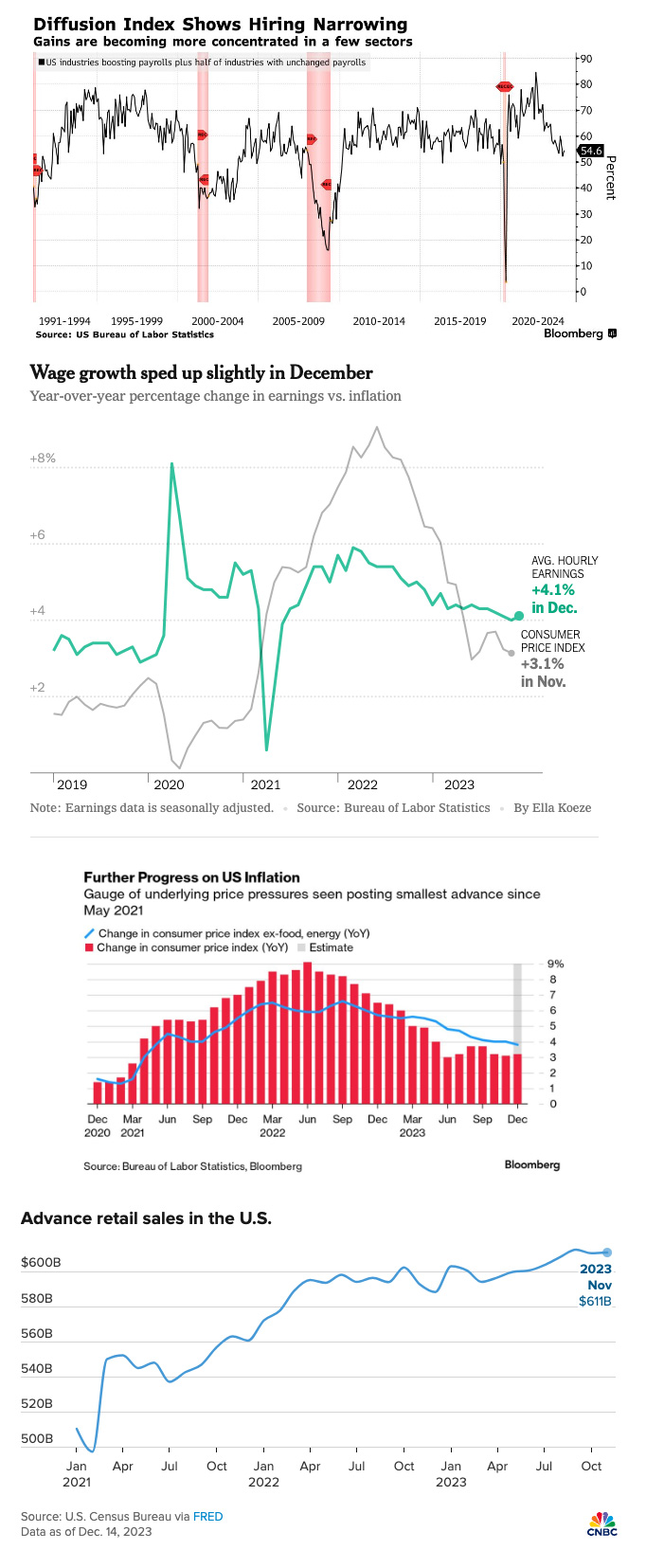

Wage gains were surprisingly robust last month, with average hourly wages rising 4.1% annually, a good tick above predictions of 3.9%. While good news for workers, Fed Chair Jerome Powell believes readings above 4 percent remain troublesome for inflation reduction, so December’s report will likely keep officials on their toes.

Now, briefly back to the divergence in the two surveys last month: the household survey is again countering the otherwise strong December establishment survey, with the chief concern being the dramatic dip in the participation rate. But as we discussed in October, it is essential to remember that the small sample size of the household survey makes it a more volatile series.

Inflation is also showing some signs of continued easing. The latest consumer price index (excluding the more volatile food and fuel measures) increased 3.8% in December over last year, representing the smallest increase since May 2021. That’s good news, as it appears we’re continuing to see the Fed’s tightening campaign pay off.

Looking into the rearview mirror to 2023, how should we think about the way the year concluded?

“The way it’s played out, we’ve kind of had an economy where we’ve had our cake and been able to eat it too… [2023 was] an exceptional year in terms of labor supply, and it’s hard to see that persisting” observed Jonathan Millar, senior economist at Barclays.

2023 began with unemployment at 3.4%, matching lows not seen since the late 1960s, and remains restrained despite the slight uptick in the year’s final months. An expanded pool of available talent drove the tight labor market’s easing as immigration levels rebounded and more prime-age Americans returned to the workforce, helping to reduce labor shortages. And while inflation continues to be a primary pain point for consumers, the inflation rate has cooled significantly in the last 12 months. At the same time, actual wages rose throughout the year, eventually outstripping price increases. The US consumer overall has remained resilient: last year marked the first that travel rebounded since the pandemic, with the recent Thanksgiving travel period shattering previous records. Those pay increases likely buoyed the year’s surge in consumer spending, though continued robust spending in 2024 seems less likely, with household debt also at an all-time high. Lastly, we can probably declare victory over the possibility of imminent recession – at least for now. Entering 2023, economists and experts nearly unanimously predicted that a recession was coming. Today, according to a December poll by the National Association for Business Economics, most economists (76%) believe that the chance of a recession in the next 12 months is 50% or less.

It is probably safe to say that 2023 was a year of unexpected and mostly welcome surprises.

December’s payroll gains were primarily monopolized by three categories: education and health, leisure and hospitality, and government, with more than half of last month’s gains coming from healthcare and government alone. Healthcare hiring continues to accelerate as market forces such as the aging of the U.S. population and Covid-19 fuel demand. Meanwhile, leisure and hospitality have maintained the highest hiring rate among all industries since 2020 and are slowly inching closer to their pre-pandemic levels. However, even though job growth continues to be promising, its concentration in just a few industries across 2023 is a likely sign that the labor market is beginning to lose some steam. December recorded further job losses in the transportation and warehousing industry and saw temporary help services cut 33,000 jobs. As we’ve discussed before, temp help services can often be the canary in the coal mine for broader changes ahead as companies attempt to avoid laying off permanent staff.

Wage gains were surprisingly robust last month, with average hourly wages rising 4.1% annually, a good tick above predictions of 3.9%. While good news for workers, Fed Chair Jerome Powell believes readings above 4 percent remain troublesome for inflation reduction, so December’s report will likely keep officials on their toes.

Now, briefly back to the divergence in the two surveys last month: the household survey is again countering the otherwise strong December establishment survey, with the chief concern being the dramatic dip in the participation rate. But as we discussed in October, it is essential to remember that the small sample size of the household survey makes it a more volatile series.

Inflation is also showing some signs of continued easing. The latest consumer price index (excluding the more volatile food and fuel measures) increased 3.8% in December over last year, representing the smallest increase since May 2021. That’s good news, as it appears we’re continuing to see the Fed’s tightening campaign pay off.

Looking into the rearview mirror to 2023, how should we think about the way the year concluded?

“The way it’s played out, we’ve kind of had an economy where we’ve had our cake and been able to eat it too… [2023 was] an exceptional year in terms of labor supply, and it’s hard to see that persisting” observed Jonathan Millar, senior economist at Barclays.

2023 began with unemployment at 3.4%, matching lows not seen since the late 1960s, and remains restrained despite the slight uptick in the year’s final months. An expanded pool of available talent drove the tight labor market’s easing as immigration levels rebounded and more prime-age Americans returned to the workforce, helping to reduce labor shortages. And while inflation continues to be a primary pain point for consumers, the inflation rate has cooled significantly in the last 12 months. At the same time, actual wages rose throughout the year, eventually outstripping price increases. The US consumer overall has remained resilient: last year marked the first that travel rebounded since the pandemic, with the recent Thanksgiving travel period shattering previous records. Those pay increases likely buoyed the year’s surge in consumer spending, though continued robust spending in 2024 seems less likely, with household debt also at an all-time high. Lastly, we can probably declare victory over the possibility of imminent recession – at least for now. Entering 2023, economists and experts nearly unanimously predicted that a recession was coming. Today, according to a December poll by the National Association for Business Economics, most economists (76%) believe that the chance of a recession in the next 12 months is 50% or less.

It is probably safe to say that 2023 was a year of unexpected and mostly welcome surprises.

As for the next several months, it is seeming less and less likely we’ll see a rate cut from the Fed in the first half of the year. Officials have indicated they are planning to keep rates high as they await more robust data that confirms inflation is moving towards their 2% target. At the meeting last month, most officials earmarked at least three rate cuts in 2023. Undoubtedly though, the strength of last Friday’s report will do little to accelerate cuts and points to the Fed holding steady at the next several meetings. Former New York Fed President William Dudley said the first Federal Reserve rate cut is more likely to come in May than March.

Other economic experts agree with the Fed’s hold fast approach:

It would seem we’ve skirted the worst of the economic fallout from the pandemic. How and when we’ll see interest rates cut however, remains the debate. We’ll have to wait until the next policy meeting later this month to see how officials interpret December’s numbers, and whether they offer us any glimpse at the path forward.

“It’s a labor market that showed substantial resilience while cooling to levels that were much more acceptable from the Fed’s perspective […] It was about as good of an outcome for the labor market as you could have hoped for in 2023.”

(Sources: Economic Policy Institute, NPR, The New York Times, The Washington Post, The Wall Street Journal, Bloomberg, US Chamber of Commerce, MSN, Bureau of Labor Statistics, RSM, CNBC, Axios, NPR, AP News, Statista, National Association for Business Economics, Fortune, Barrons, Reuters, CNN)

What Else for January?

Software Solutions

Copyright © 2025 Charge State. All rights reserved.

Software Solutions

Copyright © 2025 Charge State. All rights reserved.