As we enter the final stretch of 2024 (ugh, I know), November is the time we typically practice gratitude for the events of the year behind us. On the list of things you may not be grateful for? If you’re a parent of a young child ( ), you might say “the end of daylight saving time last weekend”. Indeed, ditching DST to move to permanent Standard Time is growing in popularity, despite backing from the retail and hospitality industry. Here’s what to know about the debate to abolish the practice, which costs the US over $670M annually in accidents and injuries alone

), you might say “the end of daylight saving time last weekend”. Indeed, ditching DST to move to permanent Standard Time is growing in popularity, despite backing from the retail and hospitality industry. Here’s what to know about the debate to abolish the practice, which costs the US over $670M annually in accidents and injuries alone  .

.

We’ll get to the economy shortly, but first: I wish you a cozy Thanksgiving, filled with all your favorite things!

Cheers,

Nicole

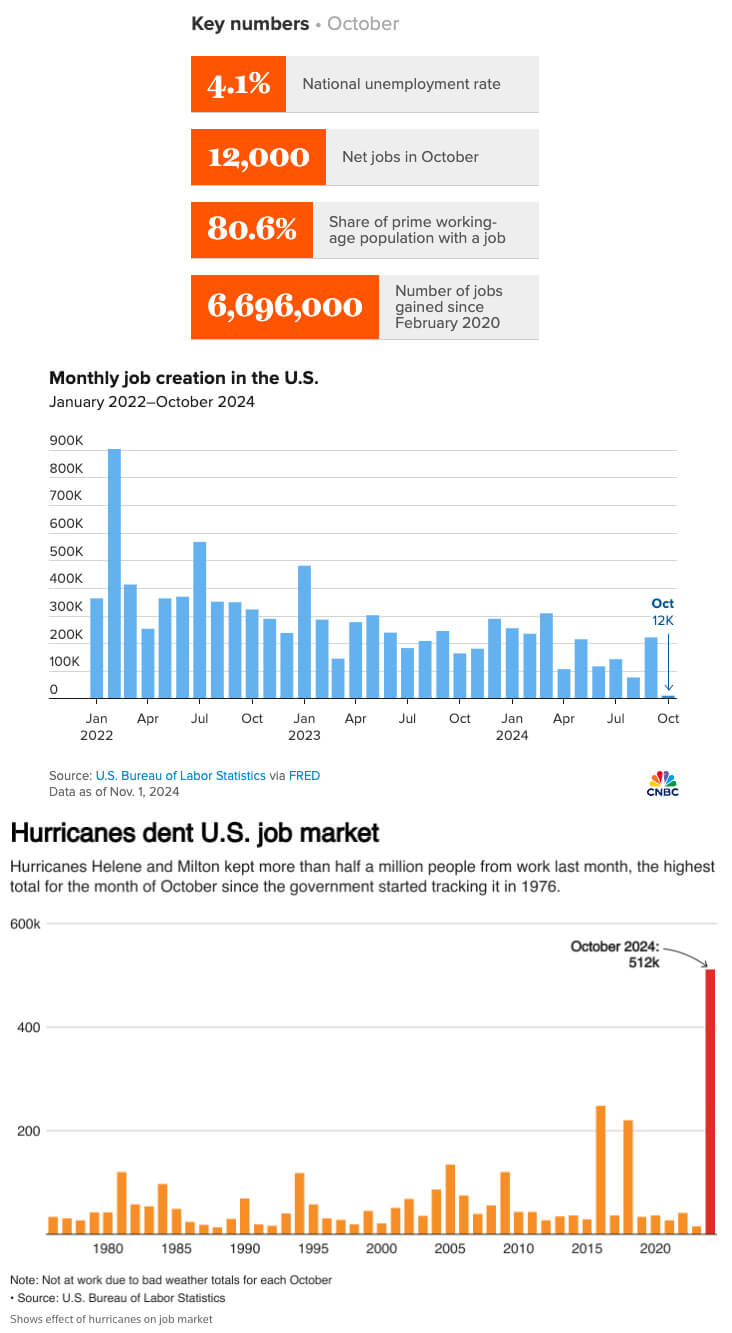

In an about-face from September, job creation last month slowed to the weakest pace since late 2020, adding just 12,000 payrolls, well below the Dow Jones estimate of 100,000. October was already expected to be a somewhat lackluster report given significant disruptions due to weather and strike activity. Still, it also included substantial downward revisions from previous months, lowering August and September gains by a total of 112,000. And while the unemployment rate held steady at 4.1%, that was because more people left the labor force.

“This is not the clarifying report on the economy that Americans and markets needed before next week’s election to answer whether voters are better off than they were four years ago […] The one thing we can rule out is that the dramatic slowdown in nonfarm payroll jobs does not indicate the economy is at a tipping point and in danger of falling over the cliff and into recession” said Christopher Rupkey, chief economist at FWDBONDS.

Job gains were concentrated in just two service-related sectors, health care and government, adding 52,000 and 40,000 positions respectively. Several sectors, like manufacturing, also saw losses and temporary help services reduced by 49,000 payrolls (a measure economists watch closely for early signs of labor market inflection). Before Friday’s report, job creation had averaged closer to 200,000 a month during 2024.

Meanwhile, the number of permanently unemployed people grew to 1.8 million, suggesting that it’s becoming more difficult for those unemployed to find a new opportunity. Last Tuesday’s JOLTS report showed that only 3.1 million Americans quit their jobs in September, (the fewest in more than four years), hinting at a lack of jobseeker confidence in the market. In tandem, the Labor Department reported that employers posted only 7.4 million job openings in September, the fewest openings since January 2021. “The big one-off shocks that struck the economy in October make it impossible to know whether the job market was changing direction in the month. But the downward revisions to job growth through September show it was cooling before these shocks struck” noted Bill Adams, chief economist at Comerica Bank.

Unlike hurricanes, the direct impact of worker strikes on job totals is more apparent. Last month manufacturing employment fell by 46,000, driven mainly by a Boeing strike that has pulled at least 33,000 workers onto the sidelines since September.

This brings us to the heart of our discussion this month – the impact of dual hurricanes Milton and Helene. The household survey from which the unemployment rate is calculated found that 512,000 people were unable to work in October, and about 1.4 million people who usually work full-time reported only working part-time because of the weather. Both data points represent an all-time high for the month of October. The storms likely also affected average hourly earnings, which grew 0.4% over the month, as the loss of lower-paid hourly workers during weather disruptions could have changed the overall composition of the data.

The BLS report acknowledged the weather impact but said “it is not possible to quantify the net effect” of the storms on the jobs total. This seems to be somewhat of a sticking point for experts opining on this latest round of data. Most experts cited in recent articles (along with Fed Board Governor Chris Waller) appraised storm impact on job loss at around 100,000, roughly the delta between the net 12,000 gain and initial job gain predictions of 110,000. However not all economists agree it’s that simple to quantify. Guy Berger of The Burning Glass Institute would agree with the BLS, and suggests a concrete estimate is something of a fool’s errand, as “we just don’t know”. For example, hourly workers who do not get paid when absent from work do not count as employed in the establishment survey, but do count as employed in the household survey, leading to a temporary depression of payroll numbers. Another factor complicating the picture is the October establishment survey response rate, which dropped to 47.4%. This was the lowest participation level since January 1991 and well below the five-year October average participation rate of 69%. It’s unclear how – if at all – the smaller sample size impacts the data.

“At first glance, October’s jobs report paints a picture of growing fragility in the U.S. labor market, but under the surface is a muddy report roiled by climate and labor disruptions […] While the impacts of these events are real and should not be ignored, they are likely temporary and not a signal of a collapsing job market.” said Cory Stahle, economist at the Indeed Hiring Lab.“This is what a soft landing looks like in the month of a hurricane.” said Justin Wolfers, an economist at the University of Michigan.

To be sure, many experts are suspending firm predictions until the next analysis comes out in December. As for now, today’s decision on a quarter-point rate cut is all but certain, with CME FedWatch rating it at a 98% possibility. But future meetings remain less certain. Policymakers face a stubborn economic puzzle that will determine the future rate of cuts. The crux of the problem? The labor market continues to show signs of cooling, while the economy has simultaneously been buoyed by consumer spending that has defied expectations of a slowdown in 2024. And finally, the US election outcome this week makes the path forward all the more challenging, with most economists viewing Donald Trump’s plans for steep tariff hikes and mass deportations of migrants who have been propping up labor supply since the pandemic – as inflationary.

We’ll know more (perhaps) after today’s news conference, and as the holiday hiring and shopping season unfolds.

(Sources: Economic Policy Institute, The Conference Board, CNBC, US News, JP Morgan, The Guardian, AP News, PBS, The Washington Post, Reuters, The New York Times, Federalreserve.gov, Guy Berger via Substack, Indeed Hiring Lab, CNet, The Wall Street Journal, Bloomberg, MSN)

What Else for November?

Do you know someone who would like this newsletter? Share it with them!

(Sources: Economic Policy Institute, TalentNeuron, Josh Bersin, KPMG, Stanford Institute for Economic Policy Research, McKinsey, Gartner, The New York Times)

Software Solutions

Copyright © 2025 Charge State. All rights reserved.

Software Solutions

Copyright © 2025 Charge State. All rights reserved.