Change State is now part of Recruitics! Learn more

Subscribe to get more insights

Happy New Year!  I hope you ushered in 2025 with a little bit of this energy! January often feels like the first page of a new book, and this month our newsletter has a new look. We’re now framing our monthly updates as Change State’s Labor Market Insights, with a sharper focus on how macroeconomic trends—like inflation, unemployment, and interest rates—impact job seekers and employers. If, however, you’re looking for commentary on international trade and stock market performance, I know a guy. As we evolve this newsletter throughout 2025, I’d love to hear your feedback or suggestions—feel free to connect with me and share your thoughts!

I hope you ushered in 2025 with a little bit of this energy! January often feels like the first page of a new book, and this month our newsletter has a new look. We’re now framing our monthly updates as Change State’s Labor Market Insights, with a sharper focus on how macroeconomic trends—like inflation, unemployment, and interest rates—impact job seekers and employers. If, however, you’re looking for commentary on international trade and stock market performance, I know a guy. As we evolve this newsletter throughout 2025, I’d love to hear your feedback or suggestions—feel free to connect with me and share your thoughts!

On that note, our 2025 Talent Acquisition Trends Survey is closing this week. If you haven’t had a chance yet, we’d love to hear your perspective on the challenges and opportunities shaping the future of talent acquisition. Your input will help us deliver meaningful insights to the community. Take the survey here  2025 Talent Acquisition Trends Survey​

2025 Talent Acquisition Trends Survey​

In the meantime, if you haven’t locked in a resolution just yet, NPR’s Life Kit has a list of fun and practical suggestions to get you started. As for the economy, let’s get into it.

Cheers,

Nicole

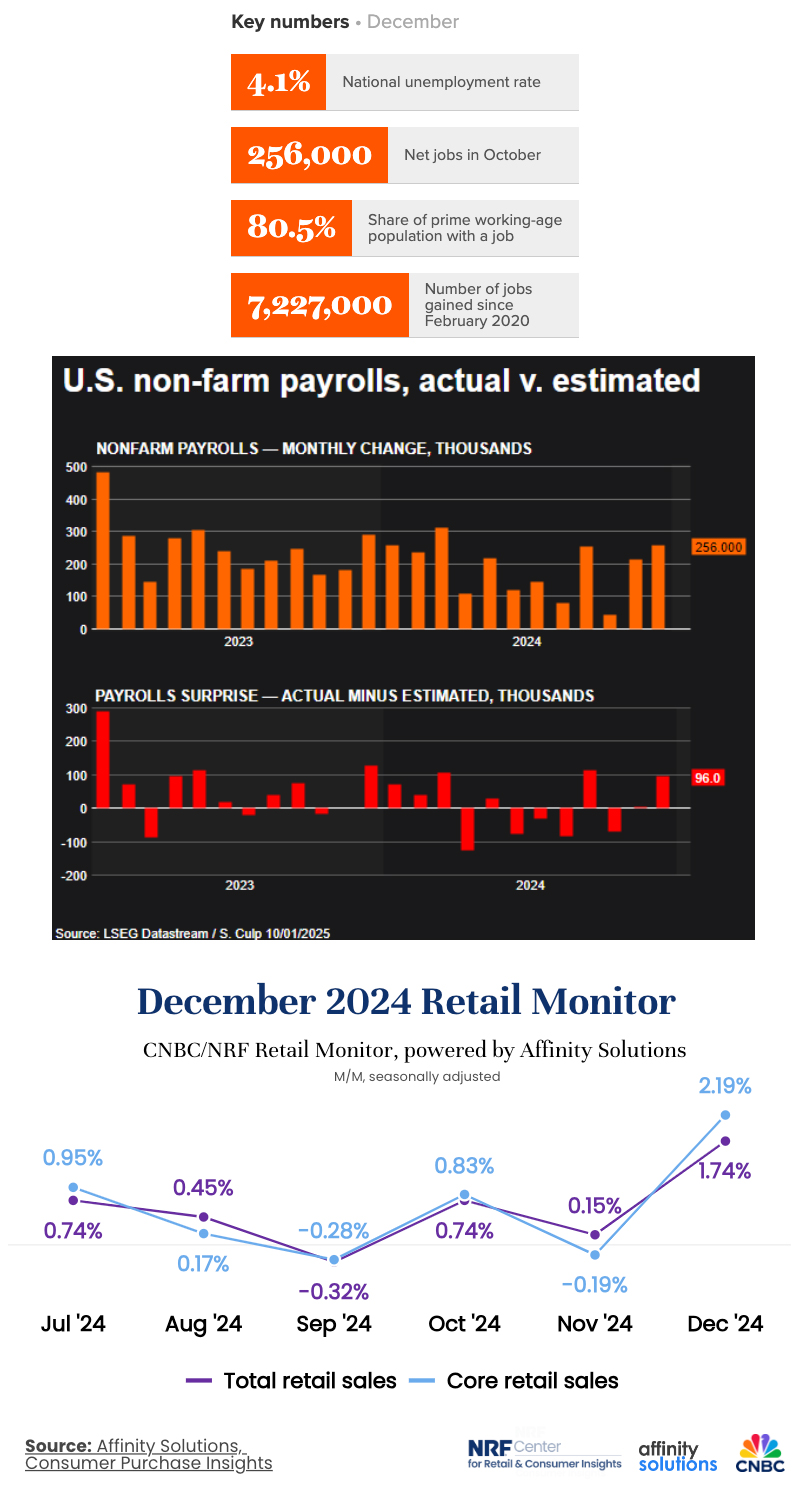

The 2024 labor market stuck the soft landing in December, adding a total of 256,000 jobs – far more than the consensus forecast of 155,000 (for context, monthly job growth averaged 186,000 last year). November totals were revised downward to 212,000, while October’s were revised up to 43,000. Unemployment somewhat unexpectedly ticked back down to 4.1%, reversing the small rise in November. While a lot has been made of fluctuations in the employment rate lately, it’s actually remained between 4.0% and 4.3% since last May. December also saw a modest lift in the prime age (25 to 54) employment-to-population ratio from 80.4% to 80.5%, almost equal to the pre-pandemic high of 80.6%.

The US economy has been churning out jobs at a steady rate: in total 2.2 million jobs were created last year. That number has tapered since the market generated 3 million in 2023, 4.5 million in 2022 and a record 6.4 million in 2021, however last year’s average monthly job gains still exceeded the average of 182,000 in the handful of years just before the pandemic.

Growth in December was bolstered by the usual sectors: health care, government, social assistance, and leisure and hospitality. After an unusually lackluster November due to a shortened period between Thanksgiving and the holiday season, retail sales rebounded in December and the sector added 43,000 jobs. While December beat expectations overall, some sectors continue to struggle: “Manufacturing is still getting crushed,” noted Brian Jacobsen, chief economist at Annex Wealth Management. “The macroeconomy may be fine,” he said, “but each individual’s microeconomy could look very different.”

​Nominal wage growth came in at 3.9% and does not appear to be re-accelerating as it remains roughly where it has been for three consecutive months. From a wages perspective, growth is in line with Fed inflation targets, though as quit rates continue to decline, we may see further deceleration in wage growth. The average workweek hours remained steady at 34.3, above the four-year low of 34.2 last year. Notably, both the quit rates and layoffs remain low – at 1.9% and 1.1% respectively, they are both well below pre-pandemic levels. What remains to be seen is how this will affect job growth over time: employers have less need to hire if people don’t quit.

Diving deeper into the report we can find other encouraging details: a decrease in the unemployment rate came from more people finding employment, rather than more people choosing to exit the workforce. A broader measure of unemployment, which includes individuals working part-time but who would prefer full-time work seems to have leveled off after reaching a peak of 7.8% last summer. In addition, temporary help services have started adding jobs in recent months, reversing a multi-year downward trend, and suggesting that employers anticipate growing demand and are adding contingent labor accordingly.

All in all, economists found little fault with December’s report:

Yet last month’s story can be interpreted with a more pessimistic lens…depending on who you ask. Good news for the economy can be bad news for investors, as the saying goes, and markets slumped last Friday after the report’s release. December’s data underscores that the economy and hiring were able to grow at a solid pace in spite of persistently high interest rates, making the Fed less likely to issue more rate cuts in the near term. Too much of a good thing could prove to be bad for Wall Street by keeping interest rates high – but if you were worried about the potential for recession, December’s good news is, in fact, good news.

The US economy has been churning out jobs at a steady rate: in total 2.2 million jobs were created last year. That number has tapered since the market generated 3 million in 2023, 4.5 million in 2022 and a record 6.4 million in 2021, however last year’s average monthly job gains still exceeded the average of 182,000 in the handful of years just before the pandemic.

Growth in December was bolstered by the usual sectors: health care, government, social assistance, and leisure and hospitality. After an unusually lackluster November due to a shortened period between Thanksgiving and the holiday season, retail sales rebounded in December and the sector added 43,000 jobs. While December beat expectations overall, some sectors continue to struggle: “Manufacturing is still getting crushed,” noted Brian Jacobsen, chief economist at Annex Wealth Management. “The macroeconomy may be fine,” he said, “but each individual’s microeconomy could look very different.”

​Nominal wage growth came in at 3.9% and does not appear to be re-accelerating as it remains roughly where it has been for three consecutive months. From a wages perspective, growth is in line with Fed inflation targets, though as quit rates continue to decline, we may see further deceleration in wage growth. The average workweek hours remained steady at 34.3, above the four-year low of 34.2 last year. Notably, both the quit rates and layoffs remain low – at 1.9% and 1.1% respectively, they are both well below pre-pandemic levels. What remains to be seen is how this will affect job growth over time: employers have less need to hire if people don’t quit.

Diving deeper into the report we can find other encouraging details: a decrease in the unemployment rate came from more people finding employment, rather than more people choosing to exit the workforce. A broader measure of unemployment, which includes individuals working part-time but who would prefer full-time work seems to have leveled off after reaching a peak of 7.8% last summer. In addition, temporary help services have started adding jobs in recent months, reversing a multi-year downward trend, and suggesting that employers anticipate growing demand and are adding contingent labor accordingly.

All in all, economists found little fault with December’s report:

Yet last month’s story can be interpreted with a more pessimistic lens…depending on who you ask. Good news for the economy can be bad news for investors, as the saying goes, and markets slumped last Friday after the report’s release. December’s data underscores that the economy and hiring were able to grow at a solid pace in spite of persistently high interest rates, making the Fed less likely to issue more rate cuts in the near term. Too much of a good thing could prove to be bad for Wall Street by keeping interest rates high – but if you were worried about the potential for recession, December’s good news is, in fact, good news.

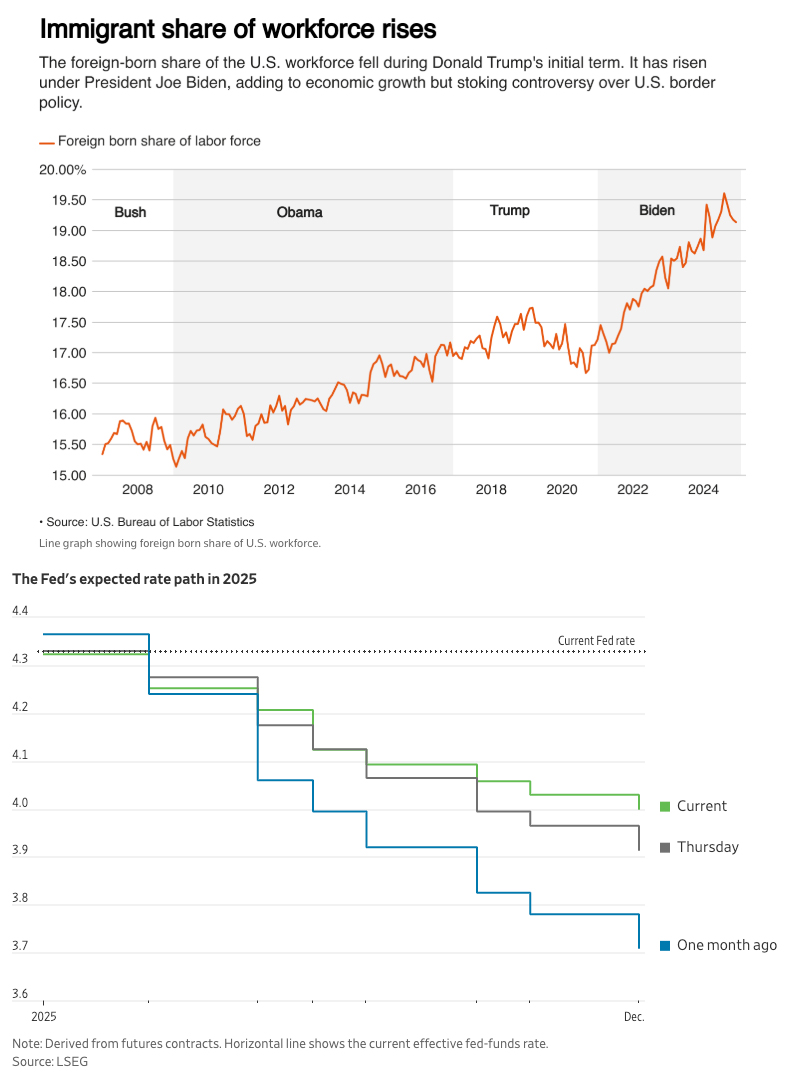

Indeed, over the past few years, the resiliency of the US economy has been a welcome and unexpected surprise. Reacting to skyrocketing inflation, the Fed raised interest rates to the highest level in more than twenty years and experts expressed concern for the future. But then the opposite happened: the widely predicted recession disappeared into thin air as companies kept hiring and consumers kept spending. In fact, US GDP has expanded at a robust annual pace of 3% or more in four of the last five quarters.

Unfortunately, a key factor behind the economy’s strength could heighten the uncertainty in the months to come. “If you believe the economic growth in excess of trend is from immigration, it is going to be hard to get numbers as large as we saw in the latter part of the Biden administration,” remarked Karen Dynan, an economics professor at Harvard University. Policy changes that could negatively impact inflation have taken center stage, prompting the Fed to deliver a conservative outlook on monetary easing last month. Given Trump’s plans and the economy’s resilience, skepticism is mounting over how much room the Fed will have to reduce rates, if at all.

Investors now await a slate of data this week on inflation, weekly jobless claims, and retail sales for clues on the Fed’s next move. Consensus estimates expect December CPI to rise to 2.9%, which taken alongside jobs growth will eliminate the possibility of a cut at the January 29 meeting. Experts are now pricing in just one interest-rate cut this year, most likely in June and then expect the Fed to hold course for the remainder of the year. A growing minority of Wall Street traders speculate that the Fed might refrain from cutting rates entirely in 2025.

One thing appears clear: hardly any experts find evidence in the data to support near-term rate cuts:

​Patience may well be our guiding principle as we enter the new year, giving the economy time to settle into its soft landing. We’ll have more insight into the Fed’s thinking at the next FOMC meeting in late January.

​​“[W]e shouldn’t expect to see another rate cut coming out of the next few FOMC meetings[…] the jobs report underscored that this is a strong economy that doesn’t currently need meaningful additional policy easing to see its expansion persist”

(Sources: Economic Policy Institute, MSNBC, The Wall Street Journal, J.P Morgan, Center for Economic and Policy Research, AP News, The National Retail Federation, The New York Times, Forbes, Federal Reserve Bank of St Louis, RSM, CNBC)

What Else for January?

Do you know someone who would like this newsletter? They can subscribe here​

​(Sources: Economic Policy Institute, Greenhouse, Lightcast, McKinsey, James Ellis via Substack, LinkedIn, Indeed, Symphony Talent, Pickle.ai)

Software Solutions

Copyright © 2025 Charge State. All rights reserved.

Software Solutions

Copyright © 2025 Charge State. All rights reserved.