Economic Update: April 2024

Change State Friends

Welcome to April!

Did you watch the eclipse yesterday? And, if you weren’t in the path of the totality, did you celebrate with one of these bizarre eclipse-themed foods? If these spectacular celestial events have given you a renewed sense of connection to nature – remember it’s Earth Day this coming April 22nd: get out there and enjoy the natural world and plant some plants, if you have the space to do so. If you need some inspiration – check out Kevin and the team at Epic Gardening for fun and practical advice, or find a local Master Gardener volunteer (hint: they often set up a booth at the farmer’s market or offer classes at your locally-owned garden center).

In the meantime, time to shake off the winter chill, embrace the fresh energy of spring, and see what’s blooming in the economy. Let’s get into it.

Cheers,

Nicole

Economic Snapshot

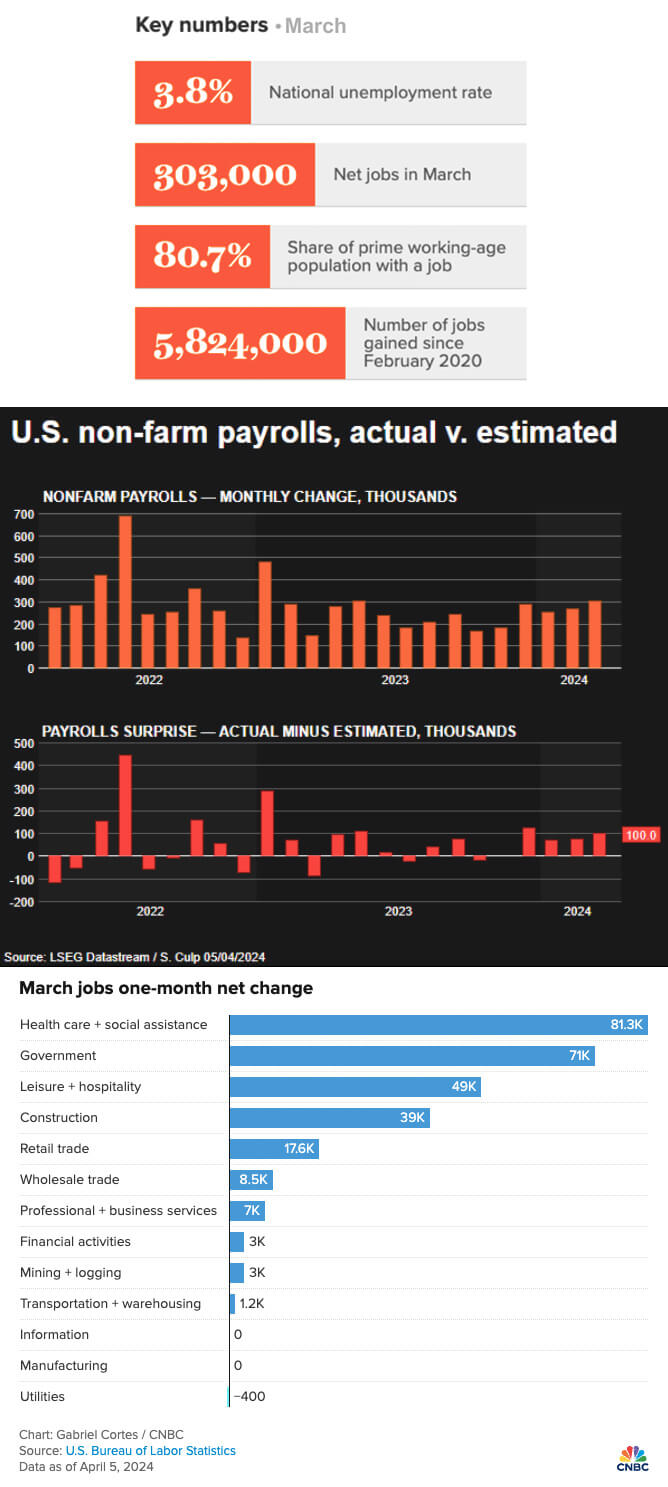

The 303,000 jobs the economy added in March represent the largest jobs gain since May of 2023. At the risk of sounding like a broken record, this once again surprised economists who had forecast closer to 200,000 new jobs. Meanwhile, unemployment once again dropped from 3.9% to 3.8% as both labor force participation and employment increased. Unemployment has now remained below 4% for 26 straight months, the longest streak since the 1960s. And this is all in spite of the fact that over 469,000 jobseekers entered the labor force in March. This surge of talent increased the ratio of Americans who have a job (or are looking for one) from 62.5% in February to 62.7%. The employment-to-population ratio, generally viewed as a benchmark of how efficiently an economy creates jobs, also climbed to 60.3% from 60.1% in February. That’s good news, as a larger labor force tends to ease the pressure to hike wages, thereby slowing inflationary tension.

March continued a 39-month streak of job growth, and what’s more, the US economy now has three million more jobs than predicted before the pandemic upended everything. Some experts have worried that as a quick labor market boom subsides, gains would be relegated to just a few sectors. The opposite appears to be true today, with growth proving more balanced: about 59.4% of industries added jobs last month.

Despite persistently high interest rates, the construction industry added 39,000 jobs, about twice its typical monthly gain, probably at least partly due to the Biden administration’s investment in large-scale projects. Meanwhile, healthcare added 72,000 jobs, government expanded by 71,000 and retail added 18,000. But the most notable story in March is how leisure and hospitality’s gains have been outstripping the rest of the labor market: employers made the most hires on record in entertainment and recreation in February, and the industry has accounted for nearly 1 in 6 new jobs created in the last year.

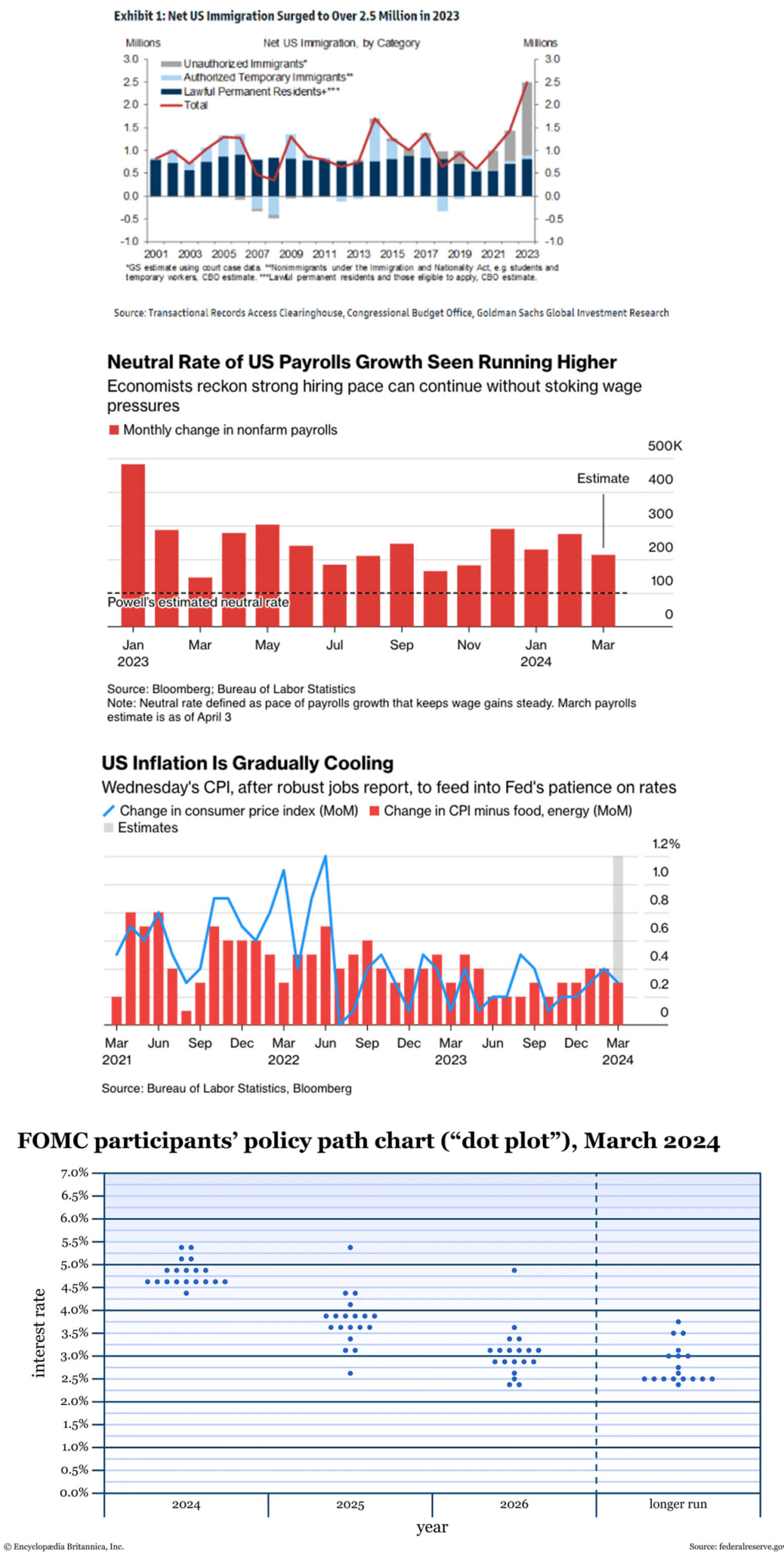

After some erratic blips in the last few months, the household and establishment surveys are now back in tandem. Economists attributed the divergence to an increase in labor supply through immigration that was not yet captured in the household survey. In fact, immigration is now a front page US economic headline and prominent experts have been weighing in on the impact. “Recent adult immigrants are more likely to be young or prime age (90%) than the native-born adult population (62%) […] They have both higher labor-force participation rates and higher unemployment than the native-born population” noted Goldman Sachs economist Elsie Peng. “Last year, half of the growth in the labor force came from net immigration. There were 5.2 million additional jobs last year, thanks to net immigration. It’s been the key to rebalancing the labor market. It’s a huge part of the reason we’ve got the growth that we’ve got and the disinflation that we’ve had,” concurred Stony Brook University professor Stephanie Kelton.

We discussed last month how the influx of immigrants has likely doubled the capacity of the labor market without risk of overheating. It now appears that this impact is starting to recalibrate the floor for “expected” monthly job gains. Economists have been benchmarking the monthly break-even pace at roughly 100,000 to keep up with population growth – a pace Fed Chair Powell identified in 2022. According to recent analysis, accelerating immigration has been raising the monthly break-even rate and the Brookings Institution has recently estimated that employers could now add 160,000 to 200,000 jobs per month this year without sending wages and inflation into an upward spiral. Other experts such as JPMorgan’s Michael Feroli now suggest underlying payroll growth is closer to 200,000 per month, and Ellen Zentner of Morgan Stanley has projected a break-even rate of 265,000 well into 2025.

The Fed Chair himself has highlighted immigration’s role in the economy’s “remarkable” performance last year. “It’s a bigger economy, not a tighter one […] Our economy has been short labor, and probably still is,” however immigration “explains what we’ve been asking ourselves, which is, ‘How can the economy have grown over 3 percent in a year where almost every outside economist was forecasting a recession?’”

In all, most experts seem to be viewing March’s report favorably, perhaps even admiringly:

- “This report is like the macroeconomist’s Holy Grail,’’ said Julia Pollak, chief economist at ZipRecruiter.“It suggests that the Fed can walk and chew gum at the same time, bringing down inflation without crippling the labor market.”

- “The vanishingly few areas to criticize this labor market are melting away,” declared Andrew Flowers, labor economist at Appcast.

- “Clearly, the job market has plenty of gas in the tank in terms of demand, and also has room to run in terms of worker supply […] that’s a good thing for all of us” said Nick Bunker, economic research director for North America at Indeed Hiring Lab.

- “Were it not for the post-pandemic inflation spike and high interest rates, [this economy] would be hailed as one of the greatest turnarounds in history” noted Daniel Alpert, managing partner of Westwood Capital.

Consistently, the message from Fed leaders has emphasized patience above all, with a close eye on how the data unfolds. Officials have previously demonstrated a watchfulness on labor demand as a possible precursor to rate cuts – one can imagine that March’s payroll surge may invite questions over the impact on inflation. We should know more soon however, as tomorrow’s US consumer-price data is projected to show a very gradual tapering in underlying inflation. Bloomberg’s economic team suggests we’ll see welcome progress: “We expect the March CPI report to show a modest slowdown in the monthly pace of core inflation to 0.3% — which is still consistent with the Fed’s annual core PCE inflation target of 2.0%. Even if annual headline inflation flutters around 3.0% through year-end, persistent disinflation in the core should allow the Fed to cut rates this summer.”

Nancy Vanden Houten, lead US economist at Oxford Economics, infers that strong job growth is not at all incompatible with rate cuts and the focus should shift towards reliable signs that inflation is abating: “The Fed does not need to see a weak labor market to begin cutting rates but will be guided by readings on wage growth and inflation, which we expect to show more progress toward the central bank’s objectives in the next few months”.

As a group, Fed officials continue to be somewhat of a mixed bag in their predictions of how aggressive rate cuts will be this year. Something new and helpful I learned this month: the central bank publishes a graphic representing their rate projections four times each year. This so-called “dot plot” shares insight into the Fed’s collective expectations on interest rates over time – a useful tool as we look to anticipate rate moves in the next few months. March’s dot plot shows ten officials are currently forecasting three cuts in 2024, while nine anticipate two or less. A new chart to bookmark perhaps, as we continue to peer into the crystal ball in 2024.

The FOMC next meets on April 30-May 1 and are generally expected to stay the course on rates…for now.

“There is no weakness in the job market which would impel the Fed to quickly cut, but no tightness which would prohibit a cut either […] Fed decisions in upcoming meetings will hinge mainly on the inflation data.”

(Sources: Economic Policy Institute, Reuters, AP News, World Bank, The New York Times, The Washington Post, The Wall Street Journal, Bloomberg, CNBC, The Brookings Institution, ZipRecruiter, Indeed Hiring Lab, Market Watch, Britannica Money, Morningstar)

What else?

What Else for March?

- X (née Twitter) commentary on the January jobs report from the EPI here.

- If you are a fan of the meditation app (I am!), you may want to give Headspace’s new Workforce State of Mind report a read for more on how workplace stress affects employees, and what organizations can do to positively impact employee mental health.

- Mercer’s 2024 Global Talent Trends for insights into how C-suite leaders intend to weather the turbulent talent market ahead, including an increased emphasis on well-being in the workplace. One notable (though perhaps not surprising) insight: employees state their top two impediments to productivity are: “too much busy work—tasks that lack value” and “too many interruptions/not enough thinking time.”

- Deloitte’s 2024 Global Human Capital Trends similarly looks at “human sustainability” in 2024 – moving beyond productivity to capture the more nuanced and holistic concept of human performance.

- More than 10 million Americans who are 65 or older are currently employed, and people who are 65 or older now represent the fastest-growing segment of the labor force—by far. This new HBR article addresses why older workers are commonly overlooked, and addresses how to tap into this “hidden talent pool” and create a successful multigenerational workplace.

- Qualtrics’ 2024 Employee Experience Trends Report shares updated employee feedback and expectations for the year ahead. Key finding: employees who work five days in an office or on-site location had the lowest EX metrics while those who work a hybrid schedule had the highest scores.

- Check out ZipRecruiter’s 2024 Labor Market Outlook report for an industry-by-industry analysis of trends, demographic changes and advice on attracting industry talent.

- Check out Edelman’s 2024 Trust Barometer for insights into the global landscape on trust and how, globally, most individuals now believe innovation is more likely to be mismanaged than well-managed.

- And if you just want to harken back to a simpler and more child-like time, perhaps you may wish to go on the internet and review sticks. Yes, sticks.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Headspace, Mercer, Deloitte, Harvard Business Review, Qualtrics, ZipRecruiter, Edelman, The New York Times)