Economic Update: August 2024

Change State Friends

It’s August, so back to school we go! As we bid farewell to lazy summer days, it’s time to dust off the backpacks, sharpen the pencils, and dive into new adventures. Curious how your recent back-to-school shopping compares to the national norm? Visit the National Retail Federation’s annual back-to-school survey for insight into this year’s spending trends. And if you are feeling a little left out, here are some ways grown-ups can harness that back to school excitement for themselves.

While parents may be breathing a sigh of relief with kids back in school (me! ) it might also be time to take a few deep breaths on the economy. Let’s get into it.

) it might also be time to take a few deep breaths on the economy. Let’s get into it.

Cheers,

Nicole

Economic Snapshot

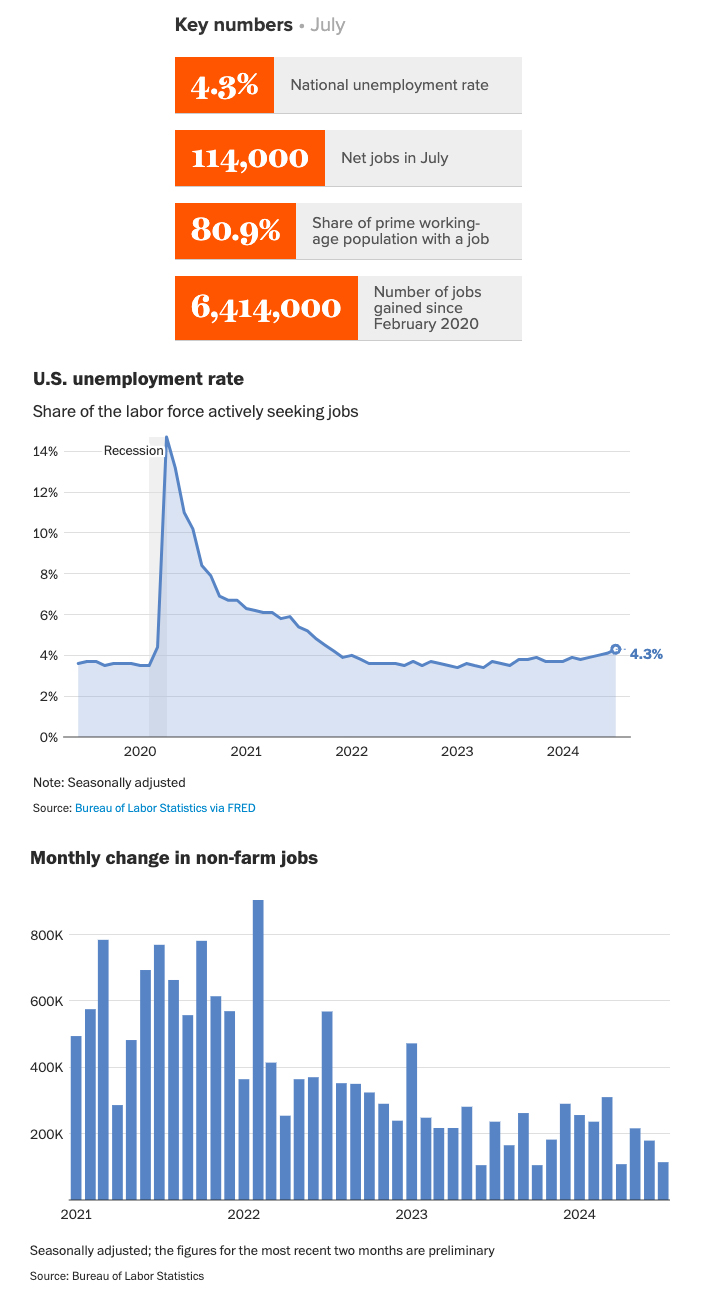

The economy seems to have hit a sudden inflection point, adding just 114,000 jobs in July – far short of the 175,000 jobs forecasted. In addition, unemployment spiked to 4.3%, the highest level since 2001. The report added to growing concerns that Fed officials have left interest rates too high for too long while monitoring inflation data, potentially tipping the labor market into a difficult to control freefall. But while there is a lot of gloom to see in July’s numbers, prime age EPOP remains a bright spot: at 80.9% it’s at the highest level in 20 years.

The uptick in unemployment is receiving a lot of analysis as the closely watched recession indicator, the “Sahm Rule”, has finally been triggered (that is: a half-percentage-point rise in the unemployment rate over three months). The theory is that rising unemployment has a dampens consumer spending, which in turn can create additional job loss and further economic shrinkage. Claudia Sahm, the former Fed economist who created the rule does not believe that recession is necessarily imminent (just “uncomfortably close”), and suggests the Fed should have cut rates this past July.

Other cooling signs can be found in the report. Job gains are becoming less broad as the diffusion index for July came in below 50: or in other words, less than half of industries added jobs. Health care and social assistance continue to lead gains with an increase of 64,000 jobs in July. Notably, the average length of the private sector workweek fell to 34.2 hours, matching the lowest level in more than a decade, and wage growth also slowed considerably in July, the weakest growth since May 2021.

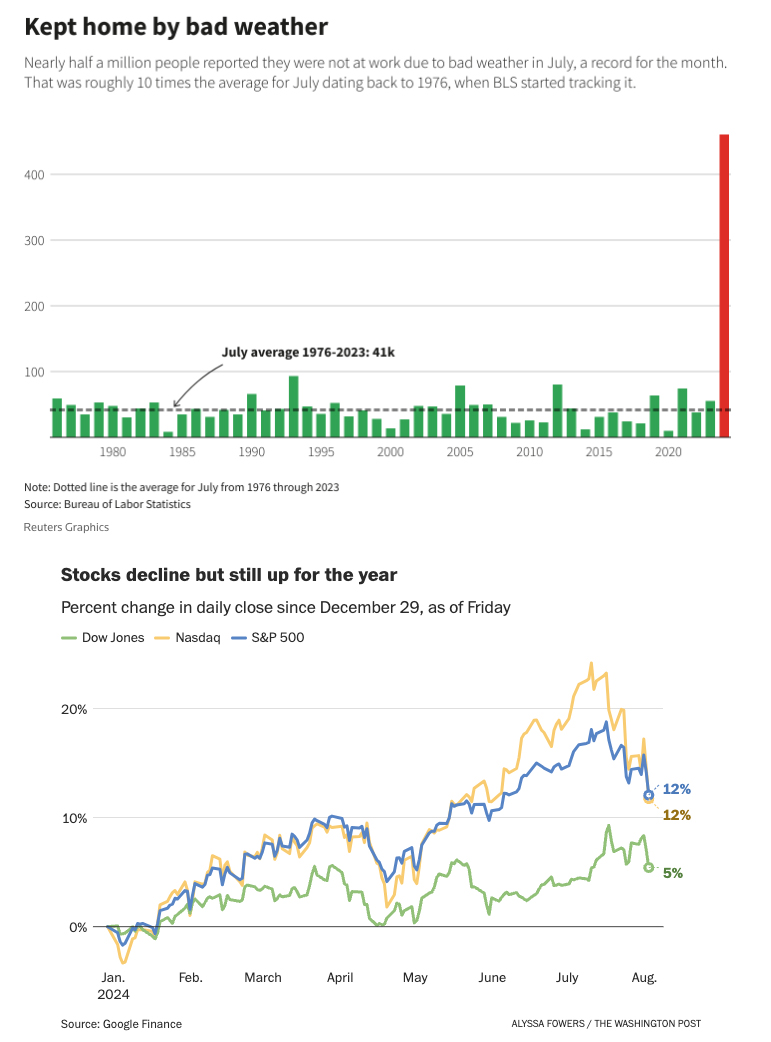

Much has been made of whether the dip in July’s jobs gains was a weather-related aberration. The BLS added a curious footnote to last week’s release to say Hurricane Beryl – which left nearly 3 million homes and businesses without power for days – “had no discernible effect” on the month’s data. If you’re thinking “huh?”, you’re not alone. Many economists called attention to the startling number of nonfarm workers who reported not being at work due to bad weather: 436,000 which is more than ten times the July average dating back to 1976 when BLS started tracking this metric. The San Francisco Fed estimated that job growth would have otherwise fallen somewhere between 130,000 and 150,000.

As you might have noticed, last week’s report also sent global markets into a tailspin on Monday as two major US indexes had their worst days in nearly two years. It’s worth mentioning that market volatility is often disconnected with economic reality, and many experts still believe the labor market is solid: “The labor market is still in a good spot right now, but all indications are that it’s unlikely to stick around here,” said Nick Bunker, economic research director at the jobs site Indeed.

All the hoopla has caused a sudden shift in expectations of how much the Federal Reserve might cut interest rates next month. Economists caution that tanking global markets could set off a chain reaction that could cause consumer and business spending to withdraw further. As policymakers evaluate the magnitude of labor market softening, they will also be watching one factor in particular: labor hoarding. Employers remember all too well the difficulty in hiring staff during the pandemic, but that dynamic may be slackening with weekly hours declining last month. “Employers have an intermediate lever they can pull, which is hours worked […] If they start to feel that things are slowing down and they’re going to stay slowed down, at some point they’re going to start letting workers go” remarked Richard Moody, chief economist at Regions Financial Corp.

“I’m not pushing the panic button at this point,” said Robert Frick, economist at the Navy Federal Credit Union. “But it is a cause for concern, and it certainly indicates the Fed is behind the curve in cutting rates.”

Sentiment does seem to be coalescing around the Fed being rather late to the game on rate moves. The Fed isn’t supposed to cut rates in reaction to cracks in the labor market. It’s supposed to cut rates to anticipate cracks in the labor market […] We fear that the Fed is so behind the eight ball here that they made a mistake not cutting rates in July” observed Bilal Baydoun, director of policy and research at the Groundwork Collaborative.

At July’s policy meeting,Fed Chair Powell acknowledged the delicate equilibrium policymakers are trying to maintain: “Wait too long or don’t go fast enough, and you put at risk the recovery …It’s a rough balance.” But by Monday morning’s market panic, some critics were also wondering whether the bank might make an emergency move before then. That’s probably an unlikely scenario as the last time Fed officials changed rates between official policy meetings was early in the COVID-19 pandemic when the economy was plummeting. “The Fed’s response will be determined by two factors: the extent to which downside risks to the real economy materialize, and whether the sharp sell-off in financial markets causes something to break,” noted Neil Shearing, economist at Capital Economics.

Regardless, the growing expectation is that the Fed will now cut rates multiple times before the end of the year. Goldman Sachs now predicts three cuts, one at each of the remaining FOMC meetings in September, November and December. Markets estimate the first cut at half a percent next month, an increase over the quarter-point cut investors had projected up until then.

“The jobs market went from tapping the brakes to leaving skid marks […] This should lock in not only a September rate cut, but perhaps a deeper cut in September and accelerate the schedule of cuts this year and next.”

(Sources: Economic Policy Institute, CBS News, The Washington Post, The New York Times, Guy Berger via Substack, Reuters, Bloomberg, Indeed Hiring Lab, MarketWatch, CNN, Federal Reserve Bank of San Francisco, The Street, MSN)

What else?

What Else for August?

- X (née Twitter) commentary on the July jobs report from the EPI here.

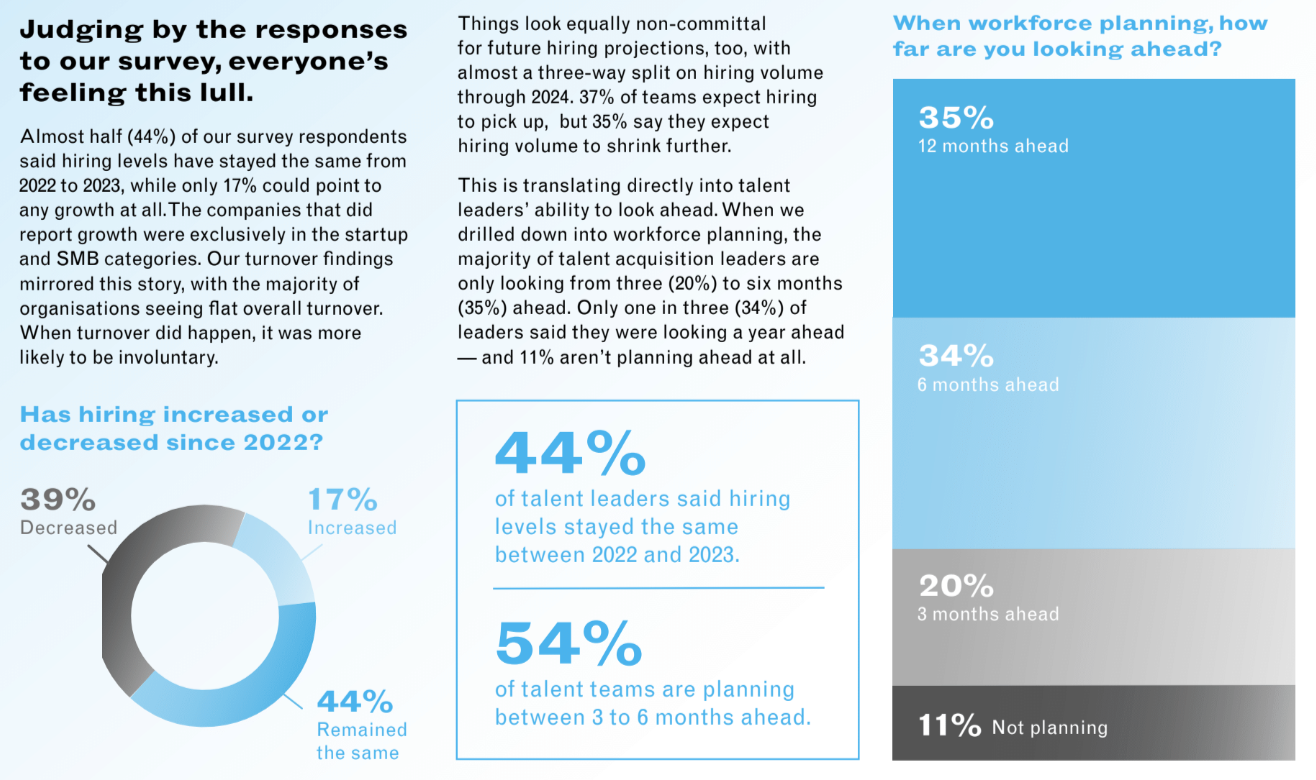

- Higher’s 2024 State of Talent Acquisition Report highlights how the uncertainty in the market is driving a pullback on hiring: Almost half of survey respondents said hiring levels have stayed the same from 2022 to 2023, while only 17% could point to any growth at all.

- This comprehensive paper from McKinsey analyzes labor market conditions across 30 economies in Asia, Europe, and North America. It outlines current labor market conditions, future prospects, and strategic actions to mitigate talent shortages.

- A new HBR article makes the case for reskilling as a strategic imperative and shares results from a reskilling survey conducted with chief human resources officers from approximately 1,200 U.S. organizations and 200 business leaders, revealing that 56% of respondents report active reskilling efforts.

- ZipRecruiter’s quarterly Job Seeker Confidence Survey finds job seeker optimism has fallen to its lowest level since Q2 2023, alongside cooling conditions in the labor market.

- Gem’s 2024 Recruiting Technology Trends evaluates AI adoption and candidate experience trends, with suggestions for prioritizing technology investments for maximum impact.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Higher, McKinsey, Harvard Business Review, ZipRecruiter, Gem)