Economic Update: December 2024

Change State Friends

The Change State team wishes you a holiday season filled with cheer and happiness! Whether you’re gathering with family, friends, or both, we hope it’s a time of joy and togetherness. And if it feels like it’s going rather quickly, you’re not wrong: this year’s calendar has the fewest days possible between Thanksgiving and Christmas. For those not especially fond of certain holiday songs getting stuck in your head, perhaps that’s a good thing. Should you need help in that department, I invite you to check out the Earworm Eraser, a 40-second audio track designed to help you shake their infectious grip. As for the economy, let’s dive into what’s been happening as we wrap up the year.

Here’s to a sparkling New Year ahead – we’ll see you in 2025.

Cheers,

Nicole

Economic Snapshot

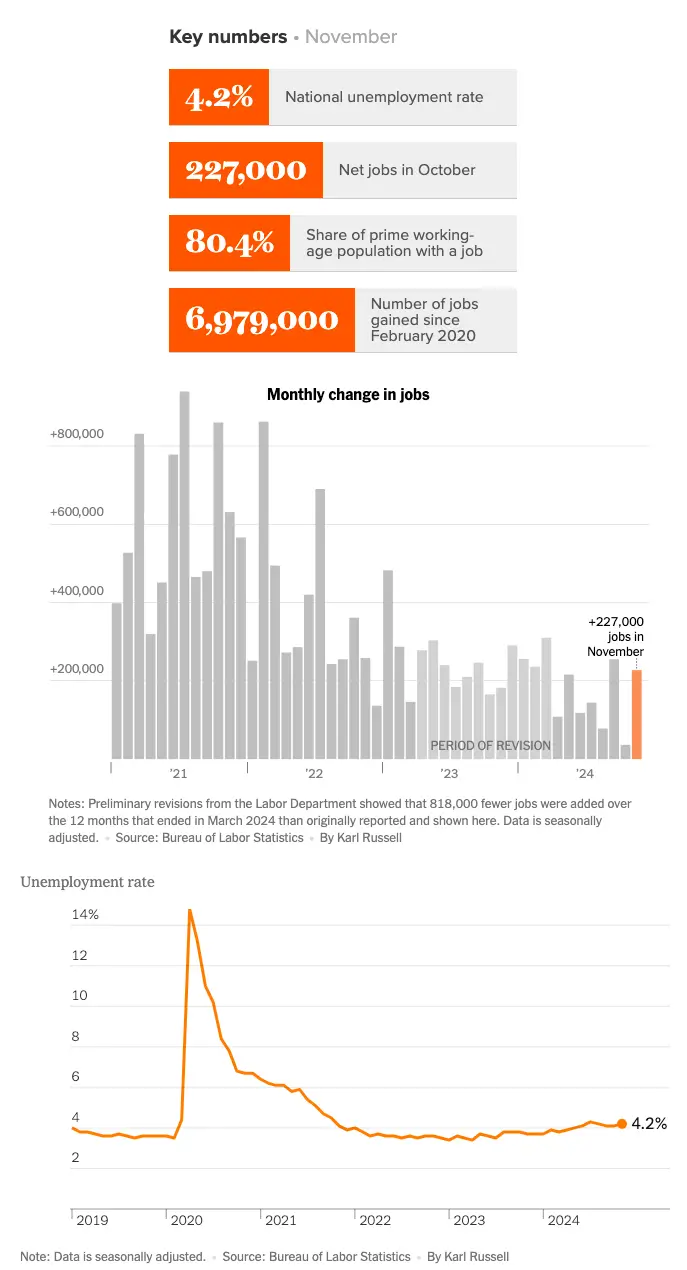

After a quite soft-looking October, November bounces back, adding 227,000 jobs and beating forecasts of closer to 200,000. Revisions to October and September added a further 56,000 jobs. Hourly wages also rose 0.4% from October and 4% year over year which came in slightly above expectation. But before we paint an overly rosy picture, it’s worth remembering that the inevitable rebound from October’s strikes and hurricanes likely boosted last month’s payrolls by 60,000, and the “true” jobs growth figure may be closer to 140,000-150,000 for November. Guy Berger, director of economic research at the Burning Glass Institute, also suggests that data from the Quarterly Census of Employment and Wages may mean we’ll see further downward revisions to 2024’s jobs totals. Meanwhile, the unemployment rate again ticked up to 4.2 %, from 4.1% and the prime working-age employment to population ratio fell to 80.4%, its lowest level of the year.

More than 70% of November’s job gains were clustered in just four sectors including healthcare and social assistance. About 37,000 workers ended strikes just after the October survey, and the recovery from Hurricanes Helene and Milton was likely to have played a role in the 53,000 jobs created in leisure and hospitality. The retail sector lost 28,000 jobs, mostly at general merchandise stores, which include Target, Costco, and Walmart – potentially signaling a weak holiday shopping season ahead.

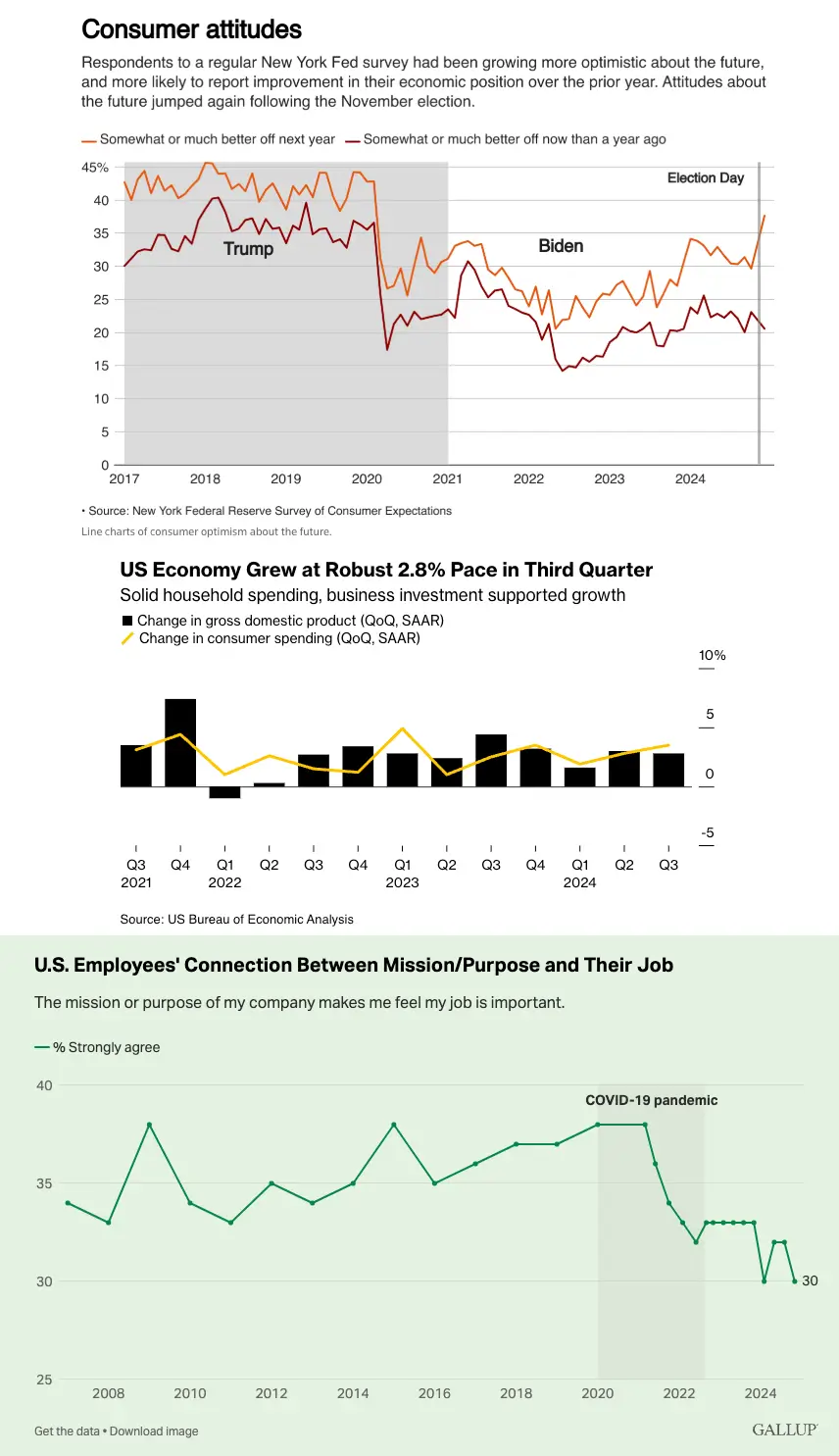

That seems hard to believe as until today, the US consumer has been propelling the economy and has shown little signs of slowing down. GDP grew at 2.8% in the third quarter and consumer spending increased by 3.5%, the most this year. The University of Michigan’s consumer sentiment index revealed a seven-month high in its early December reading, after climbing for five consecutive months. Similarly, the New York Fed’s November Survey of Consumer Expectations found the number of respondents expecting a better financial situation in the year ahead is now at the highest level since February 2020.

“This was a recovery month […] When you mix everything together, you have still have a moderately expanding jobs market. … The labor market is stable,” remarked Robert Frick, an economist at Navy Federal Credit Union.

Layoffs remain historically low and fell to just 1.6 million in October, below the lowest levels seen in the last twenty years. The rise in the unemployment rate certainly creates a mixed picture for November, but it’s lukewarm hiring, rather than rising layoffs causing the increase. Last month did see job openings rebound from September’s 3.5-year low, indicating hiring is still a priority for businesses, even though demand has slackened. We’ve also seen a simultaneous deceleration in the number of people working through temporary staffing services, which has lost nearly 600,000 positions since March of 2022.

Many experts are pointing out a stark divide in the labor market right now. If you have a job, you’re likely experiencing higher than normal job security: wages are rising and the layoff rate is lower than we ever saw pre-pandemic. In comparison, the unemployed are increasingly struggling to find work. In November the average unemployed American had been out of work for 23.7 weeks, the longest such stretch in 2.5 years, and the number of Americans on unemployment for more than 27 weeks has grown by 1.2 million this year. There’s another rift, too: the declining availability of white-collar jobs has made it increasingly difficult for college-educated Americans to find work, while blue-collar jobs are more plentiful. “The group of people in their early 20s [who have recently graduated] are bearing the brunt of a lot of cooling labor market […]We’re not used to those people bearing the pain of a cooling labor market” observed Guy Berger.

As we head into 2025, the “Great Resignation” of the pandemic era has given way to what Gallup has coined the “Great Detachment”. Employees increasingly report feeling stuck and disconnected from their work and their employer. So although turnover may have temporarily slowed, it may rebound with a vengeance when hiring picks up again.

New inflation data released just this week highlighted that the Federal Reserve’s job is not yet over. The Consumer Price Index climbed 2.7% in November, a modest uptick from the 2.6% reading in October. Core inflation – the Fed’s preferred measure – rose 3.3% over the year ending in November. But while those figures showed minimal progress, encouragingly, the shelter index finally moderated last month as cost increases climbed at the slowest monthly pace since 2021. As shelter costs put significant upward pressure on inflation, this is a hopeful sign we may soon see CPI numbers fall.

The path forward for interest rates will nevertheless remain uncertain with the looming change in administration. “A lot of the labor market focus is moving to what we call Trump’s trio of deportations, tariffs and tax cuts […] In the short term, immigration policy impact looms the largest because that could really have significant declines in the supply of workers for those industries that rely heavily on unauthorized immigrant labor. … We’re monitoring that in real time” noted Andrew Flowers, chief economist at Appcast.

Any ambiguity about the future is unlikely to derail the Fed’s final rate cut this month, with markets betting on a roughly 90% chance of a quarter-point cut at the December meeting, followed by a likely pause in January. “Growth is definitely stronger than we thought, and inflation is coming a little higher […] The economy is strong, and it’s stronger than we thought it was going to be in September […] The good news is that we can afford to be a little more cautious lowering interest rates to the point that they neither restrict nor spur economic growth,” Fed Chair Powell said in a Q&A session last week.

For today, most economists generally agree with his assessment:

- “These data clear the path for the Federal Reserve to further reduce the policy rate in December–nothing in these jobs data supports a pause in normalization. The labor market has stabilized and remains stronger than all of the naysayers have led people to believe. A stable labor market supports a strong consumer-based economy, and that’s exactly what the data have shown all year long” observed Jamie Cox, managing partner at Harris Financial Group.

- “The economy continues to produce a healthy amount of job and income gains, but a further increase in the unemployment rate tempers some of the shine in the labor market and gives the Fed what it needs to cut rates in December” said Ellen Zentner, chief economic strategist for Morgan Stanley Wealth Management.

It’s December, and since we’re all busy here’s your TL:DR for today: The economy is stable but not “great” and inflation remains persistent. You can count on a final 2024 interest rate cut, but the Fed is likely to pause and maintain a cautious pace entering 2025. Whether there’s a curve around the corner is anyone’s guess.

- Gus Faucher, the chief economist for PNC Financial Services Group.

(Sources: Economic Policy Institute, The Washington Post, The New York Times, AP News, Fast Company, Guy Berger via Substack, Forbes, Bloomberg, The University of Michigan, The New York Fed, Reuters, The St. Louis Fed, Gallup, Straight Arrow News, Barron’s CME FedWatch, The Wall Street Journal, CNBC)

What else?

What Else for December?

- X (née Twitter) commentary on the November jobs report from the EPI here.

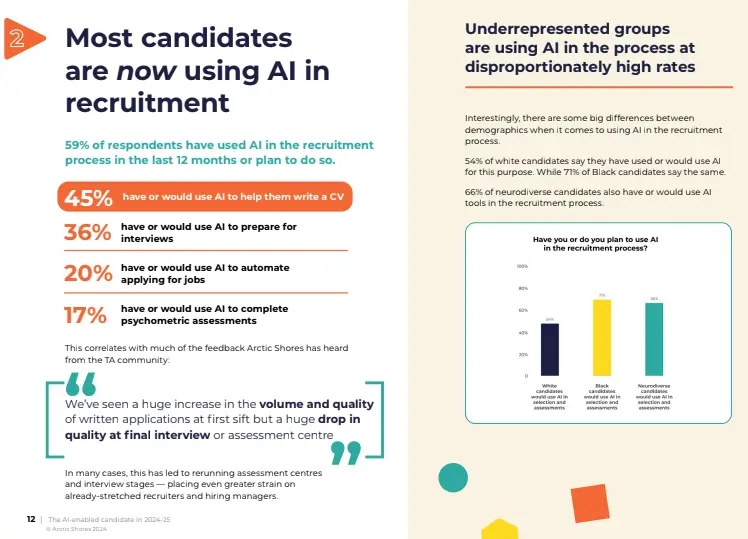

- In The State of the AI-Enabled Candidate, assessment provider Arctic Shores details how candidates have already adopted AI in the application process – and what TA teams must do to adapt and evolve.

- LinkedIn’s new Work Change Snapshot showcases business leader and professional sentiment regarding the pace of change in the workplace and predictions for how our jobs will change in the next five years. The key message? Even if you’re not changing jobs, your job is changing on you.

- Mercer’s 2024 Voice of The CHRO showcases what’s on the minds of head HR executives next year. In the top spot: building leadership capabilities within the organization.

- A new Maturity Model from Lightcast supports organizations on the journey to becoming a skills-based organization, including four key dimensions that organizations should consider for their skills-based hiring initiatives.

- Last month Glassdoor published their Worklife Trends 2025 report detailing 5 key trends expected over the next year. Trend #1? Two out of three employees feel “stuck” in their current role – Glassdoor suggests that once hiring does pick up, we may see a large wave of quits shortly thereafter.

- Tis’ the season for trend reports, so we’ll squeeze in one more from a partnership between Recruiter.com and Findem: Future of Talent Acquisition and Recruitment 2025. One particularly interesting nugget: 84% of recruiters report being disillusioned with the diminishing returns of a legacy sourcing technology – noting that despite being the primary tool used, it consistently delivers less than 40% of hires.

Do you know someone who would like this newsletter? They can subscribe here

(Sources: Economic Policy Institute, Artic Shores, LinkedIn, Mercer, Lightcast, Glassdoor, Findem)