Economic Update: June 2024

Change State Friends

Welcome to summer! Do you have exciting travel plans, or are you staying closer to home this year? With a new puppy in our household, we’re a bit limited on activities far from home – at least for the next month or so. If you too, are staying local, here are some suggestions on ways to take advantage of the summer season by creating a fun routine, building your leisure reading list, selecting a theme for the summer or finding your seasonal anthem (That’s that me, espresso ).

).

For its part, the US economy keeps dropping surprises like the kid at a summer BBQ who just discovered the watermelon seed spitting contest.  Let’s get into it.

Let’s get into it.

Cheers,

Nicole

Economic Snapshot

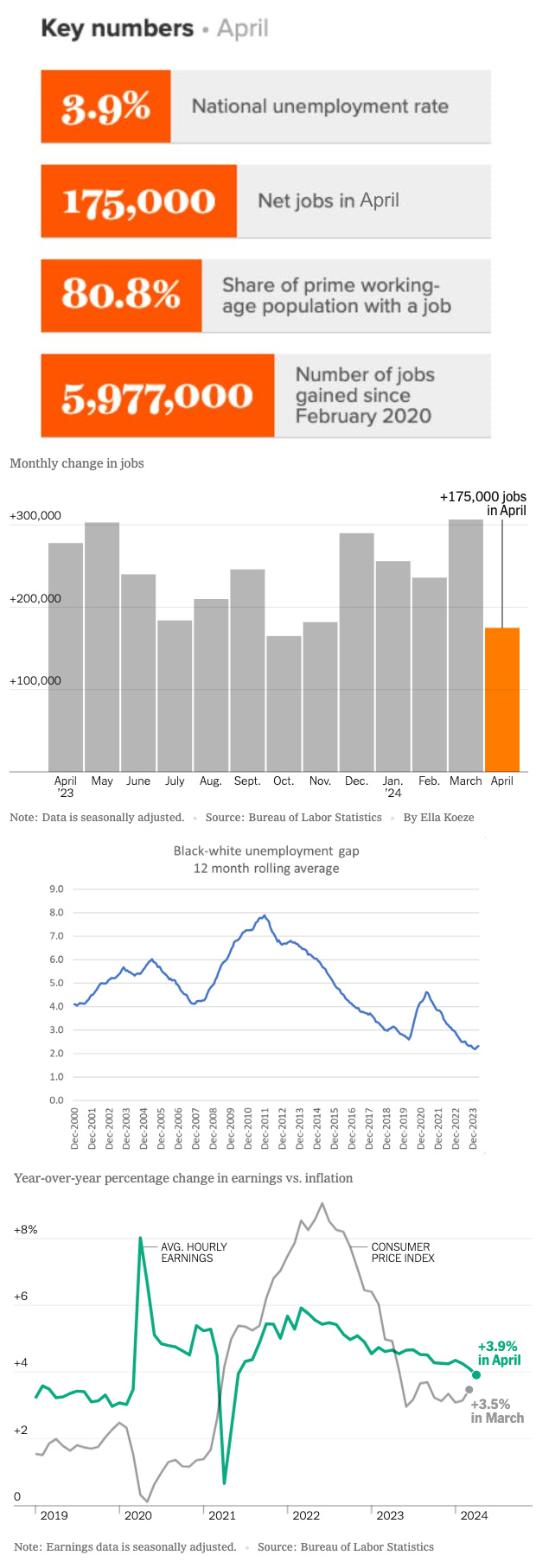

Employers added 272,000 jobs in May, much more than in April and significantly higher than the 190,000 that economists had predicted. It’s also an increase from the 232,000 monthly average across the last year which complicates the picture of an otherwise cooling economy. The rise in the unemployment rate also received top billing in May’s report, ticking up to 4 percent and ending a 2+ year record of historically low joblessness. Nevertheless, it’s important to remember that unemployment has remained at or below 4.0% for 30 months in a row, and can be a more volatile measure month to month (as it is also derived from the smaller household survey). And women’s prime employment continues to smash records, with 78% of those aged 25 to 54 currently employed or seeking work – the highest level since documentation started in the 1950s. This is likely due in part to the strong job gains in sectors that tend to employ more women, including health care, government, and leisure and hospitality.

“So much for slowing. The headline payrolls number is eye popping…. The Fed will take this to mean that they can still focus squarely on inflation without worrying much about growth,” remarked Brian Jacobsen, chief economist at Annex Wealth Management.

Indeed, hiring was spread broadly across the economy in May, with sector diversity at its highest level since January last year, as measured by the BLS Diffusion Index. Healthcare accounted for the lion’s share of growth with adding 68,000 jobs and, remarkably, has accounted for 18.6 percent of overall job gains in the last two years. Government hiring rebounded, adding 43,000, and for one of the biggest surprises in an already rather surprising report: leisure and hospitality soared by 42,000 jobs. By contrast, the sector produced only 12,000 in April and an average of 36,000 monthly in the last year. The sector may continue to expand in the coming months if forecasts for summer travel have anything to say about it.

Yet strong jobs growth in May is also confounding because it follows a recent series of lackluster economic reports, including soft income and spending data for the month of April and a weak reading on manufacturing, which faced a contraction in May. The household survey also showed 408,000 fewer people working in May than in April, suggesting job gains will face revisions over time. Finally, job openings fell to a three-year low in April, according to a separate report from the Labor Department last week. “The employer and household surveys should tell a similar story, but it’s too early to tell whether the recent divergence is a sign of deeper cracks appearing in the foundation of the labor economy or a temporary anomaly,” observed Jim Baird, chief investment officer at Plante Moran Financial Advisors.

One factor that may account for some weakness in the household survey may be young adults in their early 20s, who saw employment participation fall in May. As employers hold on to their workers and quit rates are down, there is less opportunity for those with slim work experience. We can look to see if it recuperates next month.

Average hourly wage growth rebounded in May, to $34.91, up 4.1% year over year, reversing the recent cooling trend and possibly adding to concerns the labor market remains too hot. Looking back in time a year ago however, growth was closer to 4.8%-5.3%. Wages have certainly decelerated over time, though experts are less clear if this trend will continue.

Something that may throw a wrench into labor market dynamics before long: President Biden’s new plan to restrict the number of asylum seekers. “Immigration has played a very important role in bolstering our economy […] If we do see a curtailment of immigration, then I would expect that would create a tighter labor market. That would likely send the unemployment rate down and cause wages to rise,” cautioned Joe Brusuelas, chief economist for the accounting firm RSM US.

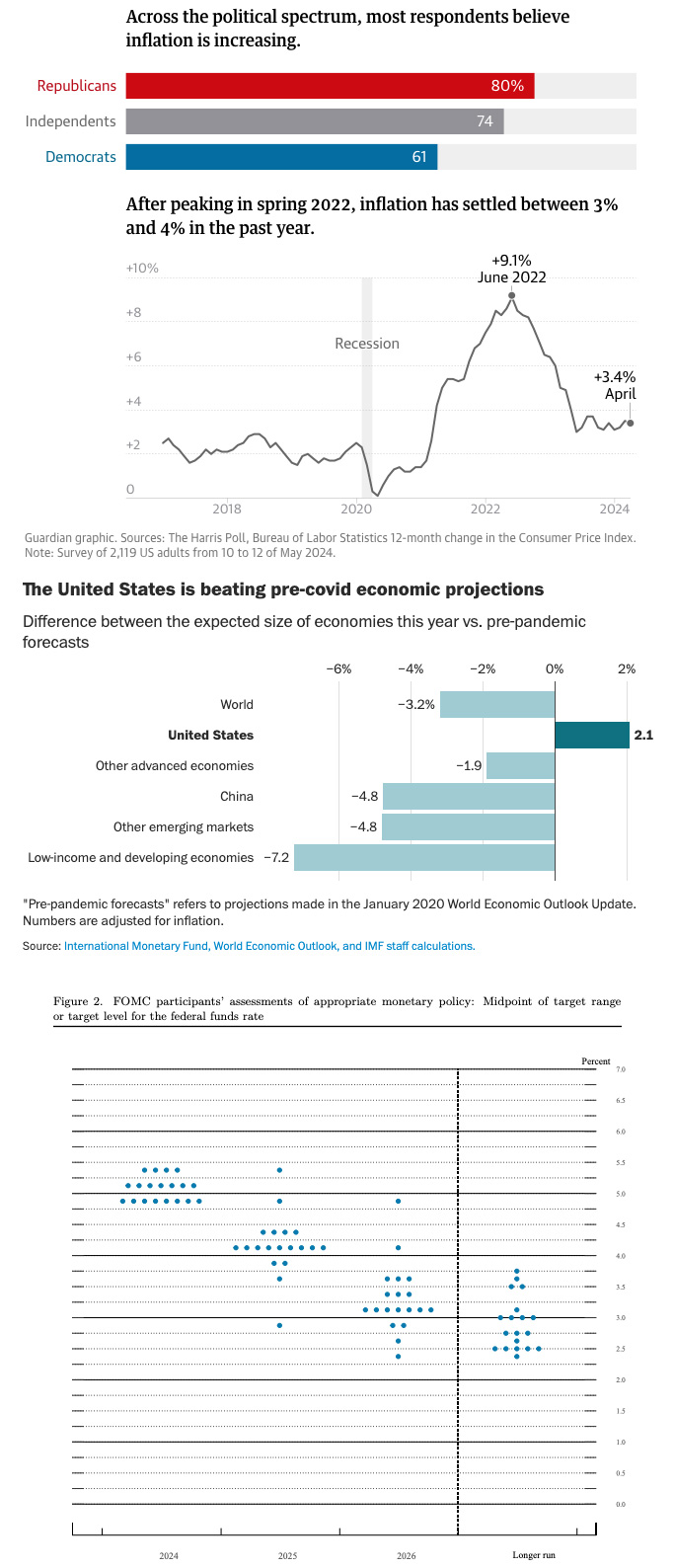

While experts may squabble about the particulars in the recent report, just about everything average Americans believe about the economy is wrong, according to a recent Harris-Guardian poll. Puzzlingly, most Americans think the economy is shrinking, while the truth is the US is surpassing expectations, outperforming other advanced economies and exceeding pre-pandemic forecasts of where we would be today. The poll also found that roughly half of Americans believe the unemployment rate is at a 50-year high when in fact it’s been at or below 4 percent for the longest stretch of time since the Nixon administration. A majority of those surveyed also believed the country is in a recession, while only about 5% of surveyed economists agree. Why? It could be a well-documented phenomenon known as “negativity bias” or a widespread economic pessimism dubbed the “vibecession” as prices at the pump and high borrowing costs lead many to feel the economy is not getting better, at least as far as their wallets are concerned.

In summary, Friday’s release was probably largely not what Fed officials were hoping for: instead of slowing job and wage growth May delivered accelerating job and wage growth, and rising joblessness. But then again, prior to this week’s meeting, a July cut was already pretty much out of the question. As expected, the Fed elected to hold rates steady this week.

Some hope may be on the horizon as the Labor Department reported on Wednesday that inflation improved last month – essentially flat from the month before and up 3.3% year over year. Core prices, which exclude volatile food and energy items, posted their mildest gains since 2021 and rose 0.2% from April, which fell below economists’ expectations. The reduction in auto insurance prices was a key contributor to May’s lower reading, and an example of how inflation has been propelled by pandemic disruptions, rather than exaggerated consumer demand or spiking wages. On that note, inflation may continue to cool as more Americans have signaled they will be curtailing spending. Major retail and restaurant chains have already responded by announcing price cuts.

Following this week’s FOMC meeting, officials predicted just one interest rate cut in 2024, suggesting there is really no hurry to slash rates. The quarterly Summary of Economic Projections, also known as the “dot plot,” is a collection of forecasts offered by the Fed governors and regional Fed presidents. In this week’s dot plot, eight officials penciled in two cuts, seven had one cut, and four predicted no change to the rate this year. By contrast, the much more optimistic March “dot plot” saw 10 of 19 officials projecting at least three cuts in 2024. Woof.

An increasingly hawkish outlook notwithstanding, we may see rates may come down before long with many experts suggesting September may be in play:

- Preston Caldwell, chief U.S. economist at Morningstar: “Logically, then, today’s news would seem to open the door to a July rate cut, although we still think that’s very unlikely given hawkish rhetoric from the Fed recently. But rate cuts starting by September should now be cemented as overwhelmingly likely.”

- Ronald Temple, chief market strategist at Lazard: “A September rate cut is very much back in play, as May’s core inflation was only 16 basis points month-on-month, which is less than half of the first quarter run-rate. Importantly, there were no major anomalies that skewed the results positively. This report is exactly what the Fed needed to increase its confidence that inflation is subsiding and rate cuts are warranted in the months ahead.”

What direction did the Fed Chair give in his remarks following the close of the meeting? Very little. “Powell deftly avoided being painted into a corner by saying flat out that he wouldn’t be specific about a number of months of good data, or about specific changes in the labor market data that would start to worry them …Essentially the guidance boiled down to ‘we’ll know it when we see it’ … The lack of specific guidance is frustrating, but also quite understandable,” observed Thomas Simons, US economist at Jefferies.

The Fed will convene four more times in 2024. Let us hope officials find what they are looking for as inflation data unfolds in the coming months.

“It remains difficult to get a clear picture of the economy. A broader view of the labor market, considering information from the Job Opening and Labor Turnover Survey (JOLTS) and weekly jobless claims, would indicate demand for labor is shifting lower. This should limit any impact to the Fed’s expected rate path as we still target September as the most likely for an initial rate cut.”

(Sources: Economic Policy Institute, The Wall Street Journal, The New York Times, The Washington Post, Reuters, Fast Company, TSA.gov, AP News, CNN, Guy Berger’s Substack, MSN, The Guardian, FederalReserve.gov, Federal Reserve Bank of St. Louis, FTxBooth US Macroeconomists Survey, Psychology Today, Kyla Scanlon’s Substack, Bloomberg, Bureau of Labor Statistics, Barron’s, MarketWatch)

What else?

What else for June?

- X (née Twitter) commentary on the May jobs report from the EPI here.

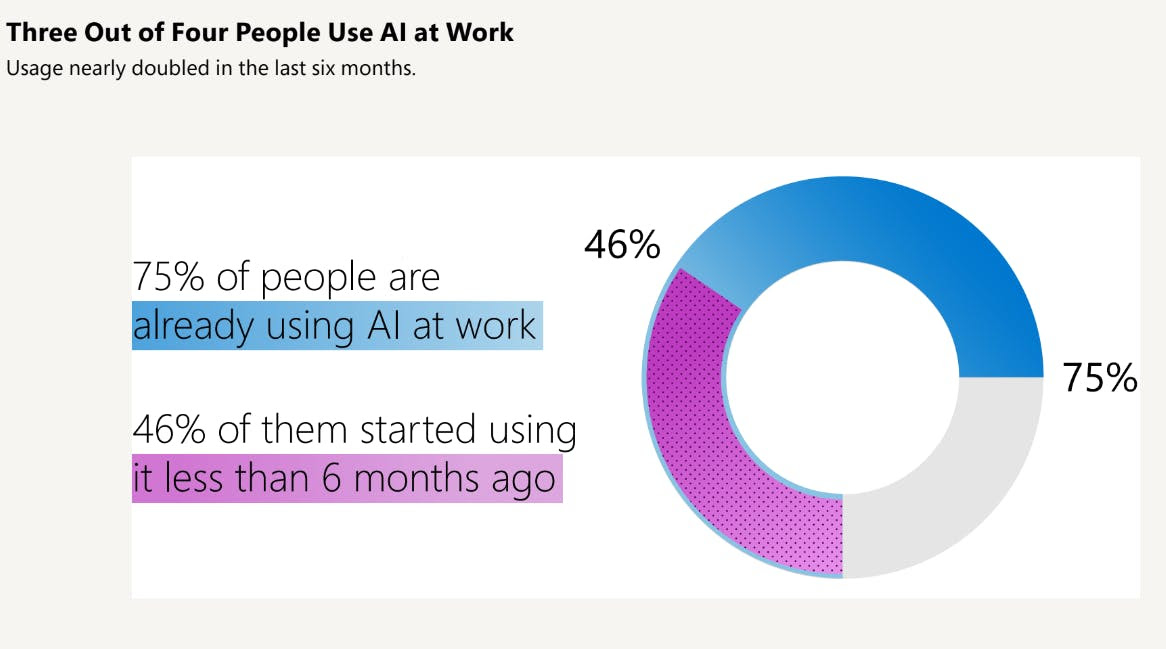

- Check out the new 2024 Work Trend Index Annual Report from Microsoft and LinkedIn, which surveyed 31,000 people across 31 countries, combined with behavioral data from users of Microsoft 365. Main takeaway: employees are prioritizing using generative AI at work, with usage doubling in just the last 6 months, and with 75% of knowledge workers reporting using AI at work today.

- The latest poll from Gallup shows that US employee engagement has dropped to a new 10-year low, and interestingly the employee categories that showed the greatest decline are younger workers under 35, exclusively onsite workers, and exclusively at-home workers.

- Indeed Hiring Lab shares recent insights that as employers continue to move to prioritize skills-based hiring, more and more are declining to include tenure requirements in job descriptions. In fact, less than a third of job postings on the platform included tenure requirements, down 40% year over year.

- A new article from HBR and Ernst & Young shares some suggestions for taking a data-backed approach to designing hybrid work arrangements.

- After falling to a record low in 2023, the number of job seekers relocating for opportunities spiked in early 2024, according to firm Challenger, Gray & Christmas. Higher wage earners are driving this increase, most probably due to increased layoffs as part of cost-cutting measures and increasing return-to-office mandates.

- A new cheat sheet from SeekOut: 5 ChatGPT Mistakes Recruiters Make and How To Fix Them.

- No soup for you: pommes frites will not be on the menu at the olympic games in Paris this year, as head chefs consider health and climate change as top priorities when designing the menu.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Microsoft, LinkedIn, Gallup, Indeed Hiring Lab, Harvard Business Review, Challenger Gray & Christmas, SeekOut, The New York Times)