Economic Update: March 2023

Change State Friends,

What a time to be covering jobs and the economy! Before you ask, no, we’ll not be talking (much) about the collapse of Silicon Valley Bank today. It’s somewhat beyond the scope of what we usually cover in this forum, and I’m sure it’s already dominating your newsfeed in one form or another. If you are eager for more information however, then allow me to placate you with a recommendation instead: Matt Levine’s Money Stuff. If you like to dive deep (and I mean really deep!) into the inner workings of Wall Street, finance, SPACs, crypto, fraud – all with a side of humor – give his free newsletter a subscribe. With that being said, we still have plenty to discuss today, so let’s get into it.

P.S. We’re hiring! Know someone with a strong talent acquisition background who is curious, skilled with data, and client-obsessed? Introduce us!

Economic Snapshot

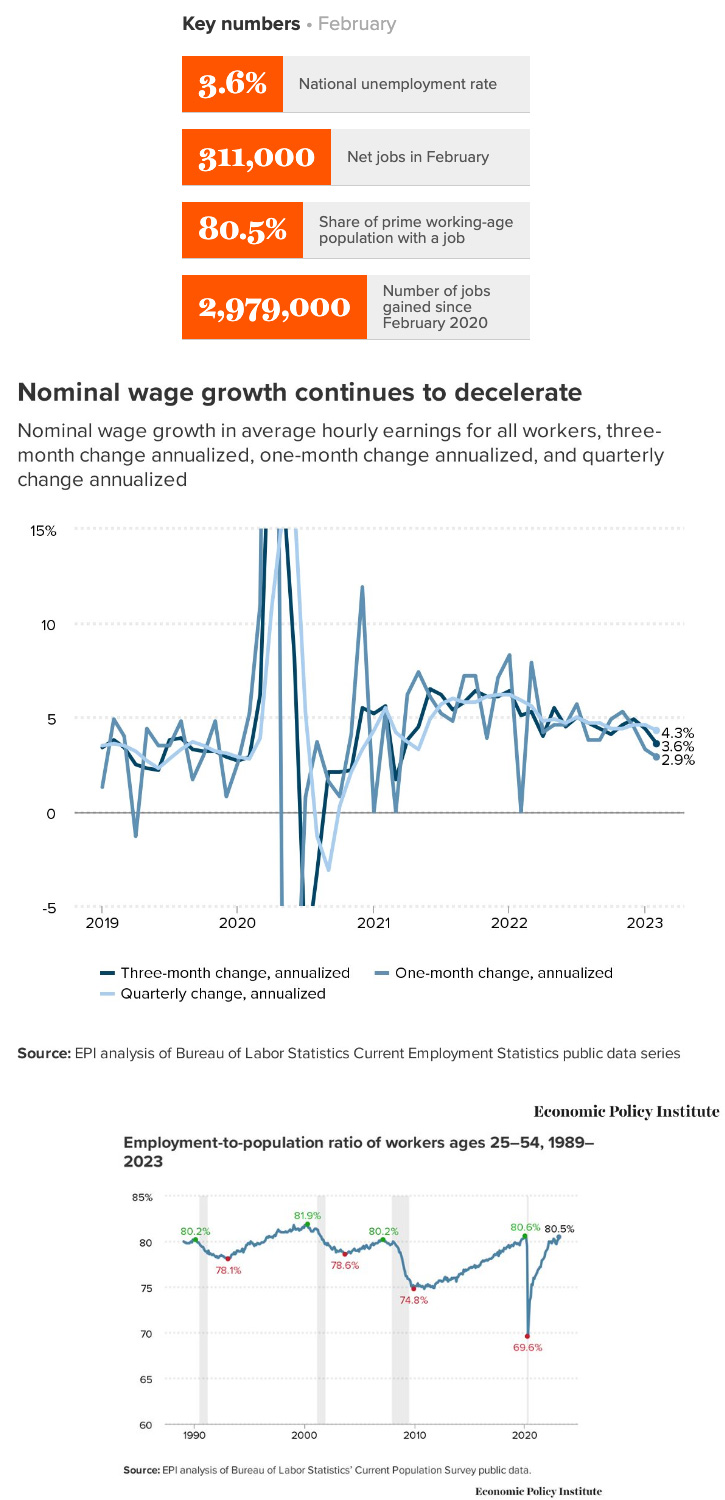

The US economy is up 311,00 jobs in February and unemployment ticked up slightly to 3.6%, up from last month’s record low – a good thing as 400,000 people joined the workforce. Nominal wage growth (that is, wages unadjusted for inflation) is slowing and inflation is slowing faster than wage growth is slowing, indicating real wages are rising (good news). Prime age EPOP (employment-to-population ratio) is also up, sitting just below pre-pandemic levels. LFPR for the 25-54 age group rose to 83.1%, the highest since January 2020, up from 82.7% in January. Some more welcome news: labor force participation in this age group has now fully recovered for women, many of whom were forced out of the labor market due to the coronavirus pandemic. (The difference between EPOP and LFPR? LFPR includes the number of people with a job as well as the number actively looking for work.)

If you’ve been following along with this newsletter, you’ll know these are all hopeful signs of the labor market’s resilience and point against the likelihood of recession.

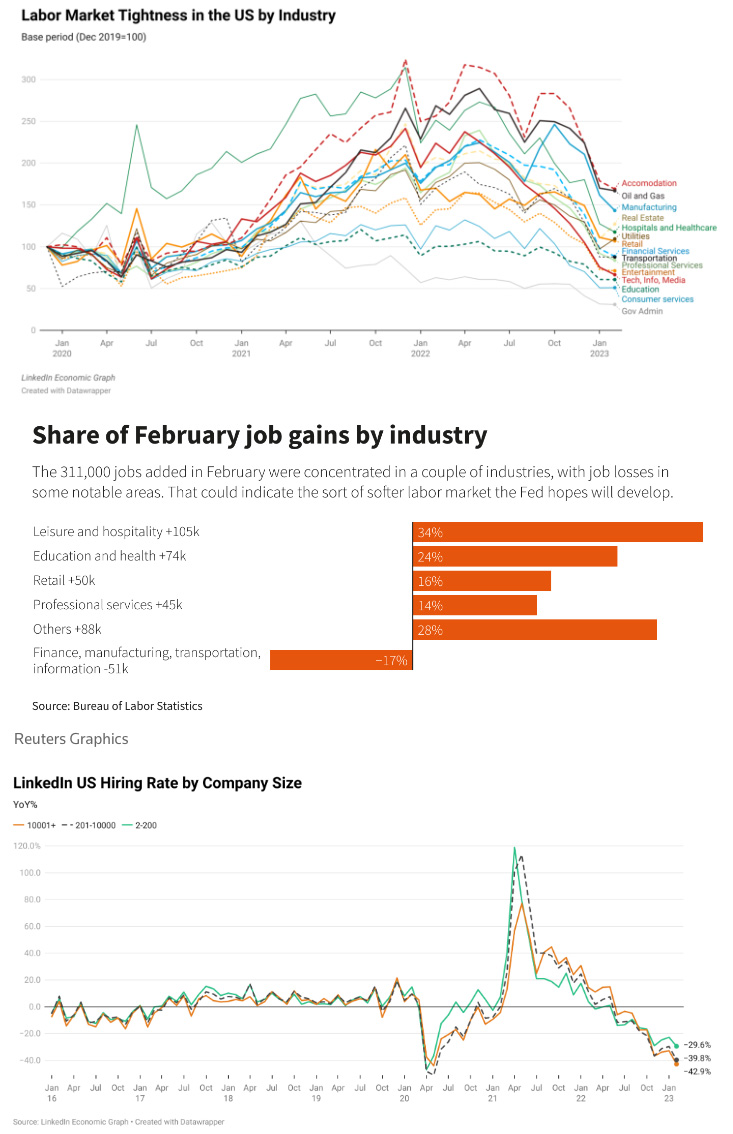

While hiring remained higher than expected, it was concentrated in a narrower range of industries, suggesting that the tight labor market might be ready to soften. Over a third of job gains from February were focused in retail, restaurants, and hotels – chipping away at the deficit of one of the hardest-hit industry sectors post-pandemic. This concentration could foreshadow slower job growth and lessening price pressures that would reduce the need for aggressive rate hikes.

January’s bombastic report could also be a fluke. The increase in consumer spending and hiring in January likely reflects unseasonably warm weather, according to Fed Chair Powell. Weather in many locations was unusually warm, which could have caused more people to go out and spend, therefore allowing more construction projects to proceed. The Federal Reserve Bank of San Francisco estimated that weather conditions alone were responsible for about 120,000 of January’s jobs.

So if 300K jobs is too much, then what target are we supposed to be aiming for? It’s suggested that job gains of about 100,000 a month would keep up with population growth and prevent unemployment from rising. It would also indicate that employers aren’t as desperate for workers and further reduce the need to keep raising wages.

Coming back to the topic of recession, notably, corporate America has largely stopped talking about it. A recent Goldman Sachs survey found that during Q4 2022 earnings calls, only 12% of businesses mentioned the term “recession”, down from Q3’s decade-high peak of 45%. Just last summer a KPMG survey found that 91% of CEOs predicted a recession was coming over the next 12 months. Goldman Sachs itself recently reduced predicted odds for a recession over the next year from 35% to 25%.

There are those, of course, still predicting recession. Forbes opinion writers suggest that the possibility of soft landing is a “head-fake”, as most of the reports with unexpectedly high upside represent data of a lagging nature, and might reveal more about where the economy has been than where its future will be. Fun fact: Google searches for “soft landing” soared to a 15-year high last month.

LinkedIn also predicts recession and that resilience in the labor market is unlikely to last. The ratio of job openings to active applicants – their measure of labor market tightness – is slowly returning to pre-pandemic levels. They note that while all businesses have seen hiring slow, larger organizations have been disproportionately compelled to make difficult workforce decisions, contributing to a more significant decrease in hiring.

And now to address the elephant in the room. The SVB collapse exposed the risks inherent in higher interest rates, and is likely to make the central bank more cautious: “It shows us: No, we haven’t really digested all of the effects of what the Fed has done so far,” said Aneta Markowska, chief financial economist at Jefferies. “There’s still a lot of policy pain in the pipeline that hasn’t hit the economy yet.”

As the Fed has shown reluctance to abandon rate hikes altogether, a better question to ask is whether we’ll see a half point or quarter point raise? While it’s less likely a hike will risk more systemic disruption to the financial system, the risk of stirring financial instability might nudge the Fed to move for a smaller increase on March 22. Most economists believe that while the chance of the March hike being 50 basis points has fallen significantly, the Committee will still end up hiking.

Subadra Rajappa, head of U.S. rates strategy at Société Générale, suggests the current banking tumult should engender caution against moving rates too drastically – and that while raising rates is the “only tool they have at their disposal” to control inflation, it also has the potential to expose the weakness of the system as a whole. Economists at J.P. Morgan have also argued the case for a smaller quarter point move this month.

This relative consensus comes after investors have made major swings in predictions about interest rate moves this year. After Fed Chair Jerome Powell’s speech last week, many sharply revised upwards their 2023 forecasts, even noting a small chance that rates would rise above 6 percent this year. But after the weekend’s upset, many now expect the Fed to cut rates to just above 4.25 percent by the end of the year.

William Dudley, a former president of the Federal Reserve Bank of New York said it’s also possible the entire banking situation will have blown over by the time the Fed regroups next week. “I am totally confused about the Fed at this point,” he said.

I suppose that might ring true for all of us, these days. More to come, next week.

“We’re in kind of a brave new world when it comes to inflation and the job market … Nothing about the pandemic recovery or the economy since that time of the pandemic really reflects historical trends”

– Nela Richardson, Chief Economist for ADP

(Sources: Economic Policy Institute, NPR, Reuters, Forbes, Fortune, The Federal Reserve, Business Insider, LinkedIn, The New York Times, Bloomberg)

What else?

What else for March?

- Twitter commentary on the February jobs report from the EPI here and here.

- Is the entire economy gentrifying? “Premiumization” is the new buzzword as everything from WD-40 to donuts shift focus to premium offerings to maintain profit margins.

- Following January’s revelation that China’s population has started to shrink, India now overtakes China as the most populous country on earth.

- More than one third of all stores opening between 2021-2022 were dollar stores. Many local communities are pushing back on the industry by voting down zoning applications and enacting outright bans on dollar store development.

- With many healthcare workers leaving the industry in droves, what actually makes them stay? One study found that it’s the organization’s commitment to quality and patient-centered care: when employees ranked their employer poorly in these areas, they were more than six times as likely to say they intended to quit.

- Discussion around flexible work has largely been dominated by whether to offer remote work, or how many days employees should be required to come into the office. But employers may be missing a crucial factor to consider: a growing set of regulatory requirements which could make compliance challenging, particularly for multinationals.

- And to those who say remote work has a negative impact on culture and collaboration, you may need to think again. A new survey shows that flexible workers are more likely to feel connected to their immediate teams, direct manager, company values, and were 57% more likely to say their company culture has improved over the past two years.

- It’s women’s history month, and a new IBM report on gender parity in the workplace shows that while growth in female representation has increased at senior and junior levels, since the pandemic women have massively exited the workforce from mid-level leadership tiers that feed the leadership pipeline at the top levels.

- While on that topic, the U.N. has recently said that as women’s reproductive rights are being rolled back and as millions of girls and women have either left education or the workforce due to the coronavirus pandemic, gender equality is now 300 years away. Woof.

(Sources: Economic Policy Institute, The New York Times, Pew Research Center, Harvard Business Review, MIT Sloan Management Review, Forbes, IBM Institute for Business Value, The Washington Post)