Economic Update: July 2024

Change State Friends

Are you staying cool this July? Heatwaves have been blasting the US this past couple of weeks, including here in Denver. When it’s unthinkable to turn on the oven, but you still have to eat, here are some fun no-cook summer recipes to help you beat the heat (just take care not to give yourself “avocado hand”). My personal favorite when the weather is scorching? A cold Spanish soup and a charcuterie board. Check last August’s update for a recipe and my tips. Stay cool, stay safe, and I hope you manage to fit in some summer fun this month despite the heat.

Now, unlike the weather, the economy is showing signs of cooling. Let’s get into it.

Cheers,

Nicole

Economic Snapshot

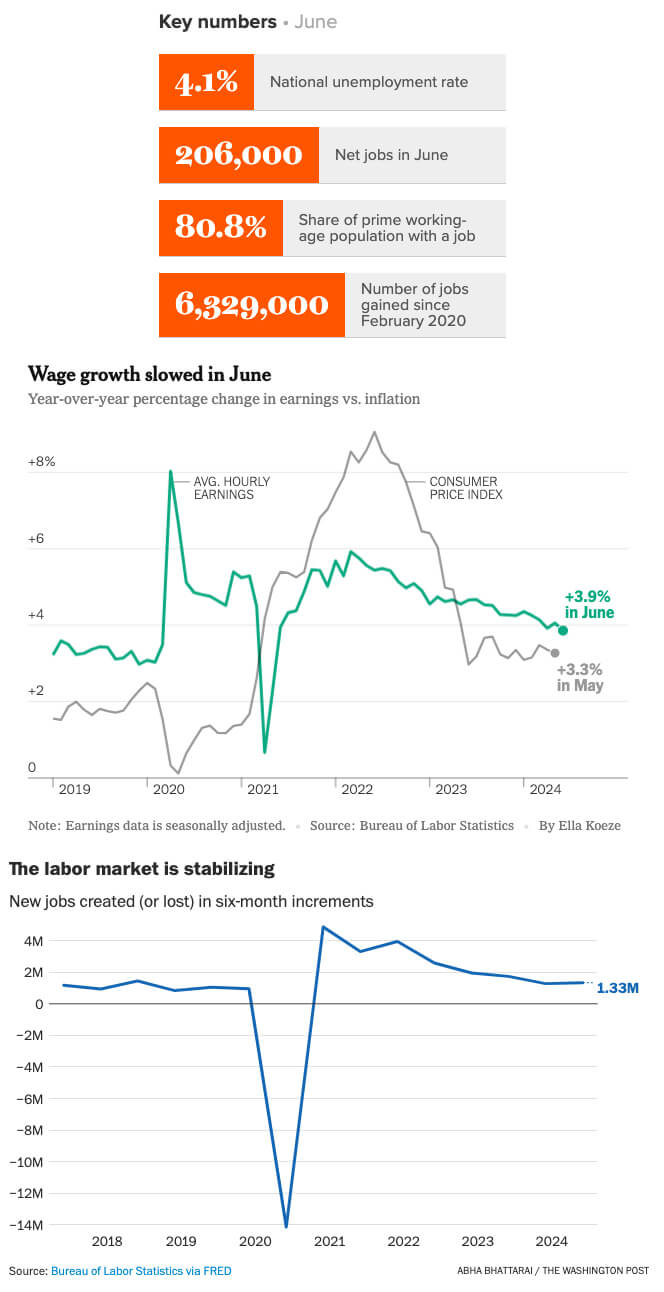

Payrolls increased by 206,000 in June, generally in line with consensus expectations for the month. That being said, we are seeing signs of decline: last month’s report revealed the economy created 111,000 fewer jobs in April and May than were previously estimated, reducing the 3-month average of payroll gains down to 177,000, the slowest seen since January 2021. June also saw yet another unemployment increase, up to 4.1%, largely due to an increase in labor force participation, as more jobseekers entered the market. The prime-age employment-to-population ratio (25-54 years old) remained solid last month, and is resting near its 23-year high.

Unlike recent months, June’s gains were concentrated primarily in health care and government, which together accounted for nearly 75% of job creation. Manufacturing and retail saw losses last month, with temporary help services featuring some of the greatest losses – down 48,900 in June. Temp help numbers are closely watched by economists as a leading indicator of where the economy may be headed. More promisingly though, after a decades-long period of decline, teen summer jobs have returned! In the highest rate of employment since 2007, over 37% of 16-to-19-year-olds held jobs last month.

And if you’re looking for signs of labor market cooling, well, you don’t have to look too hard this month. April, May and June now represent the weakest three-month stretch of job growth in the last four years. April was revised down to just 108,000 job gains, the lowest seen since last October. As a benchmark, analysts estimate the economy needs to create between 180,000 and 200,000 jobs per month to keep up with population growth, given the recent rise in immigration. What’s more, a lagging measure of employment, the Quarterly Census of Employment and Wages (QCEW), has recently suggested that jobs growth at the end of 2023 may actually be slower than has been reported in the payrolls survey. “So far, we don’t see apocalyptic signs within the labor market, but investors should be wary when the labor market is supported by government payrolls […]The downward revisions to the previous two months is consistent with an economic slowdown,” remarked Jeffrey Roach, chief economist at LPL Financial.

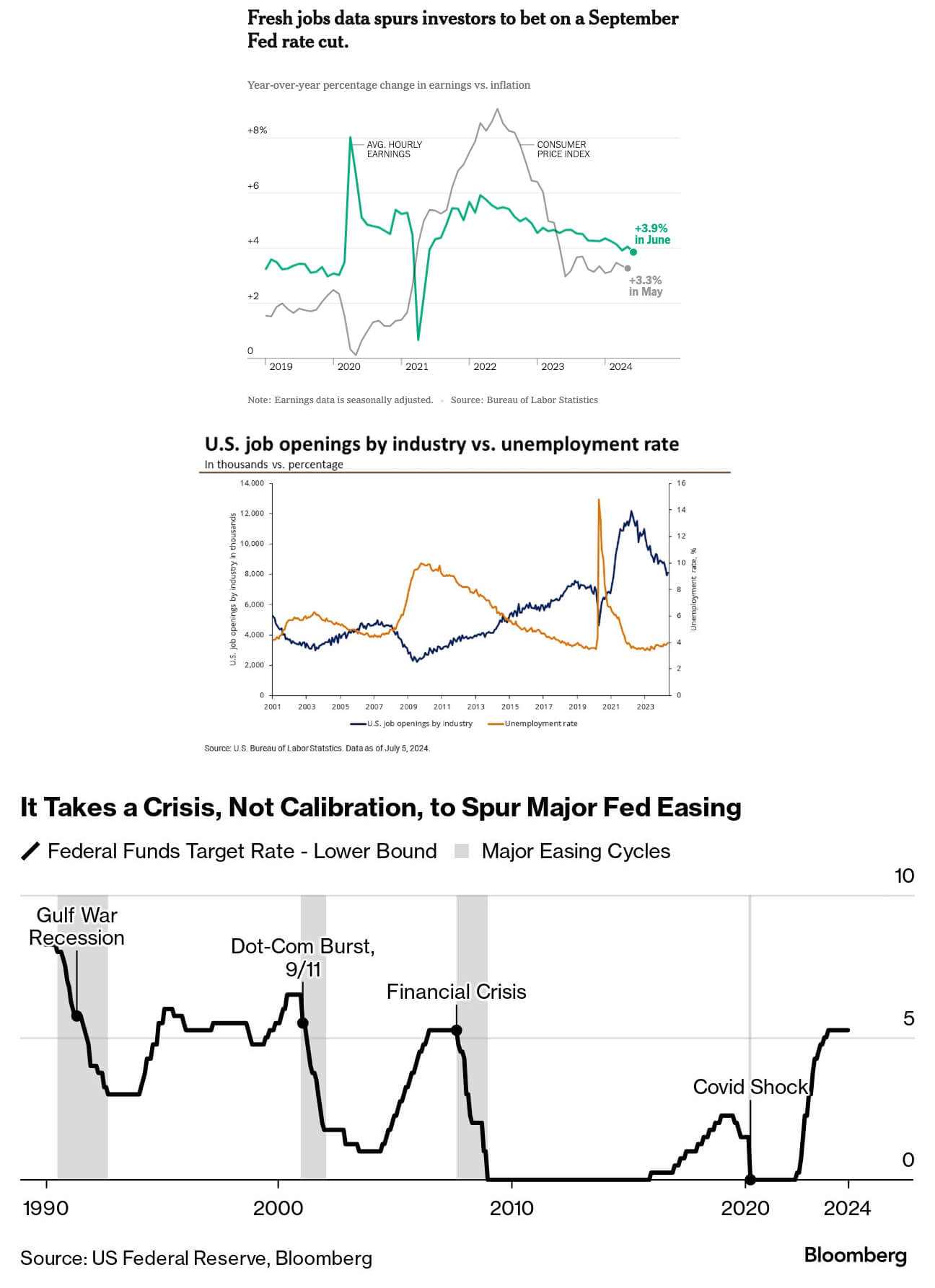

Unemployment has also been inching higher in recent months, ever since hitting a 50-year low of 3.4% early last year. June’s 4.1% reading, while still low, represents the highest rate since November 2021. Joblessness rose in part because while 277,000 people began looking for work in June, many of them did not secure jobs immediately. Simultaneously, long-term unemployment rose to the highest level in more than two years. And as for wage growth, average hourly earnings increased only 3.9 percent last month, the lowest reading in some time.

Aside from the jobs report, this month’s JOLTS data also offers evidence that the economy is losing some steam. Job openings have been steadily waning since March 2022. While there are 1.25 jobs for every unemployed American today, that rate was 2-to-1 as recently as January 2023. That may partially explain why long-term unemployment is now above its 2017-2019 average.

Fed rate hikes themselves are now more clearly weighing on the economy. Consumer spending, (which accounts for about 70% of all economic activity) rose at just a 1.5% pace in Q2 after growing more than 3% in the two prior quarters.

Taken all together, it’s now possible the US economy is on the precipice of cooling more drastically. A sudden and notable uptick in unemployment is a precursor to recession; a rule of thumb created by economist Claudia Sahm and often referred to as the “Sahm Rule.” “These numbers are good numbers,” observed Sahm, also a former Federal Reserve economist. “The labor market is in a good place, but it’s definitely softening […] Consumer spending is down, the housing sector looks weak — you put those pieces together and, yes, the economy is rebalancing. But the question becomes: How long will this continue?”.

“We’re not at the tipping point into recession yet, but I don’t have a lot of confidence about the distance from that tipping point” notes Guy Berger, Director of Economic Research at the Burning Glass Institute. He adds that it could prove problematic if downward jobs revisions continue to trend alongside rising unemployment, but a key indicator he’s watching for a true inflection point is prime age EPOP, which is currently holding firm.

Just days before the jobs report emerged, Fed Chair Jerome Powell described the US job market as “strong,” while hinting we may be approaching a critical juncture.

Current JOLTS and jobs report data reveal a distinct slowdown across just about every leading metric. And as of last week, the Fed also has a new round of inflation statistics to ponder. Last Thursday’s Consumer Price Index shows that prices are down 0.1% from May, and indicate a YoY increase of 3% – much closer to the official target. This means US inflation cooled to the slowest pace since 2021, an achievement Chicago Fed President Austan Goolsbee calls “excellent.” However New York Federal Reserve President John Williams cautioned that policymakers are not yet within reach of their goal.

As the economy softens, Fed officials are clearly trying to strike a delicate balance: ensure that inflation is in check while avoiding lasting damage to the job market. And they have signaled in recent months that intensifying market weakness could prompt them to slash borrowing costs. “We now have definitive evidence of labor market cooling with a somewhat alarming rise in the unemployment rate in recent months that should give policymakers ‘more confidence’ that consumer inflation will soon return to the 2.0% target on a sustainable basis,” said Scott Anderson, chief U.S. economist at BMO Capital Markets.

While it seems clear rate cuts are in our near future, it’s less certain how rapidly they will play out. The most recent “Dot Plot” shows Fed officials penciled in just one quarter percentage point move this year and four in 2025. However, looking back at historical trends, they have never delivered easing of that magnitude unless triggered by some crisis. Fiscal easing of that significance only came alongside the Covid-19 pandemic, 2007-08 financial crisis, and September 11 terror attacks, among other events.

The Fed meets again at the end of July, and while no one expects a surprise cut, they may start to manage expectations against a possible September rate move. Let’s hope those cooling winds continue to blow…but gently.

“There’s broad evidence that we are seeing a downshift in the economy […] We’re seeing slowdowns across the board, but it’s too early to tell right now whether we’re going toward a ‘soft landing’ or a bumpier, harder landing.”

(Sources: Economic Policy Institute, JP Morgan, MarketWatch, AP News, CNN, PBS, The New York Times, Reuters, CNBC, Federal Reserve Bank of St. Louis, The Washington Post, Conor Sen via X, Thomson Reuters, Guy Berger via Substack, Bloomberg, Forbes)

What else?

What Else for July?

- X (née Twitter) commentary on the May jobs report from the EPI here.

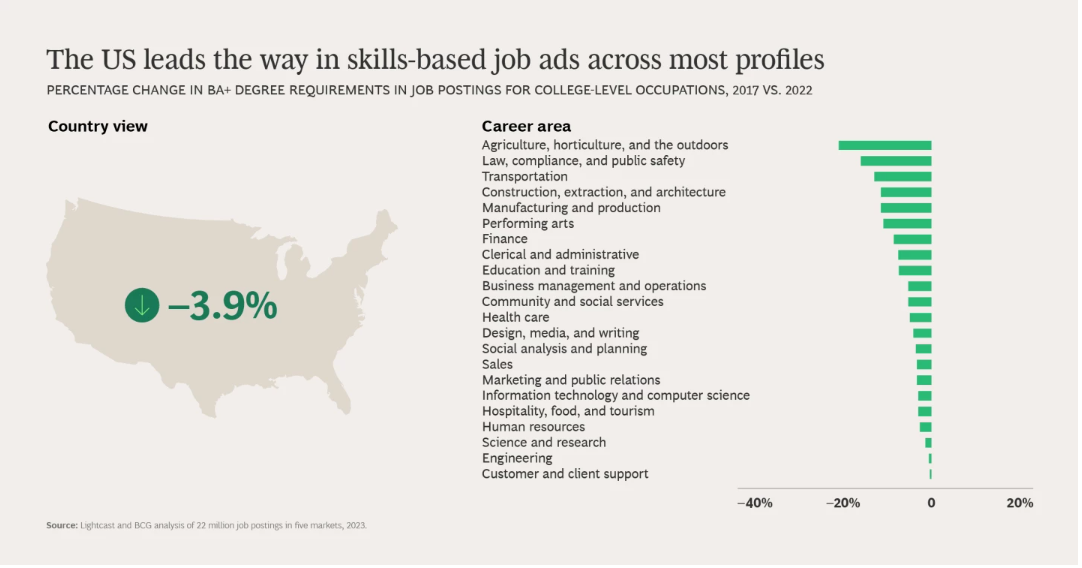

- New research from Lightcast and BCG on skills-based hiring shows the US is actually leading the way in de-emphasizing degree requirements in many job ads. Also, skills-based hires have a 9% lengthier tenure at their organizations than traditional hires.

- Check out Gallup’s State of the Workplace 2024 report for insights into how the world’s employees experience work and life. One positive change: Global employee stress declined in 2023 from 44% to 41%. This is the first time reported daily stress dropped since the pandemic in 2020, although it remains higher than the pre-pandemic average.

- How well do you know your workforce? SAP SuccessFactors 100 Critical People Analytics Questions includes questions to help HR teams decide which few vital questions are most important to their organizations and provides criteria for selecting key performance indicators.

- Phenom’s new 2024 State of Candidate Experience Report helps TA professionals to better understand how well some of the world’s leading brands are attracting, engaging, and converting candidates. One highlight: while 89% of the Fortune 500 used six or more job aggregators (such as Indeed) to distribute their jobs, none of them used UTM source tracking consistently on third-party sites.

- Check out the World’s Most Pointless Website for a bit of idle fun.

- Headed to Korea for a summer vacation? Don’t bring this Trader Joe’s seasoning as a host gift – it’s illegal.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Gallup, Lightcast/BCG, SAP SuccessFactors, Phenom, The Washington Post)