Economic Update: April 2023

Change State Friends,

Spring has sprung!  And if you celebrated either Easter, Passover, or Ramadan in the last week (a rare overlap that only occurs once every 33 years or so), then we hope you enjoyed a wonderful holiday with friends and loved ones.

And if you celebrated either Easter, Passover, or Ramadan in the last week (a rare overlap that only occurs once every 33 years or so), then we hope you enjoyed a wonderful holiday with friends and loved ones.

Getting back to the labor market. We’re used to mixed signals in our reporting, but signs this month seem more clear that the labor market is softening, not heating up. There’s also strong consensus for yet another Fed hike in May. But everyone still disagrees on whether or not we’re headed for recession. Two out of three isn’t bad, I suppose. Let’s get into it.

Economic Snapshot

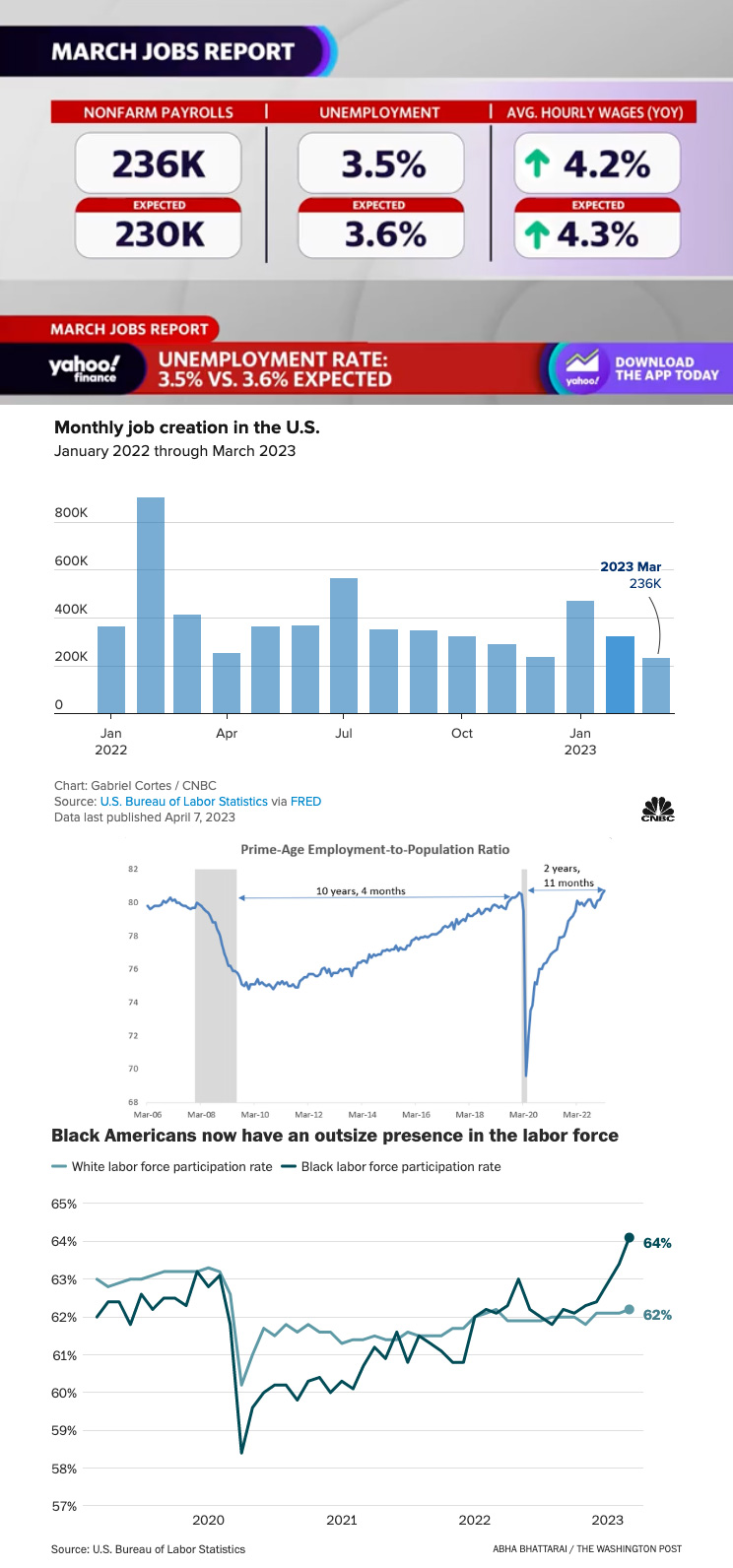

March added 326,000 jobs to the US economy and marked the 27th straight month of strong job growth. The unemployment rate fell further to 3.5%, against expectations that it would remain at 3.6%. LFPR also jumped in March, rising to 62.6% from 62.5% in February, its highest level since before the Covid pandemic. Prime age EPOP is now back to pre-Covid levels, an astonishing development as it took over 10 years to recover post Great Recession. This time it took just shy of 3 years.

Leisure and hospitality once again lead the pack in jobs gains, though remain short of pre-pandemic levels. And while state and local government jobs increased by 39,000, there remains a gap of 362,000 since Feb 2020, with two-thirds of that, problematically, in the education sector.

Some good news from March’s report, Black unemployment rate tumbled to a record low 5%, according to the data going back to 1972. What’s more, it dropped for the “right” reasons as Black LFPR and EPOP both rose, and for the first time, the Black EPOP ratio is now higher than white EPOP (meaning a higher share of Black people are working than white people). In fact, Black employment has been rising steadily in the last 5 months – possibly due to increased availability of remote work. Recent studies indicate remote work is particularly attractive for employees of color, who may be drawn to work at home to avoid microaggressions in the workplace.

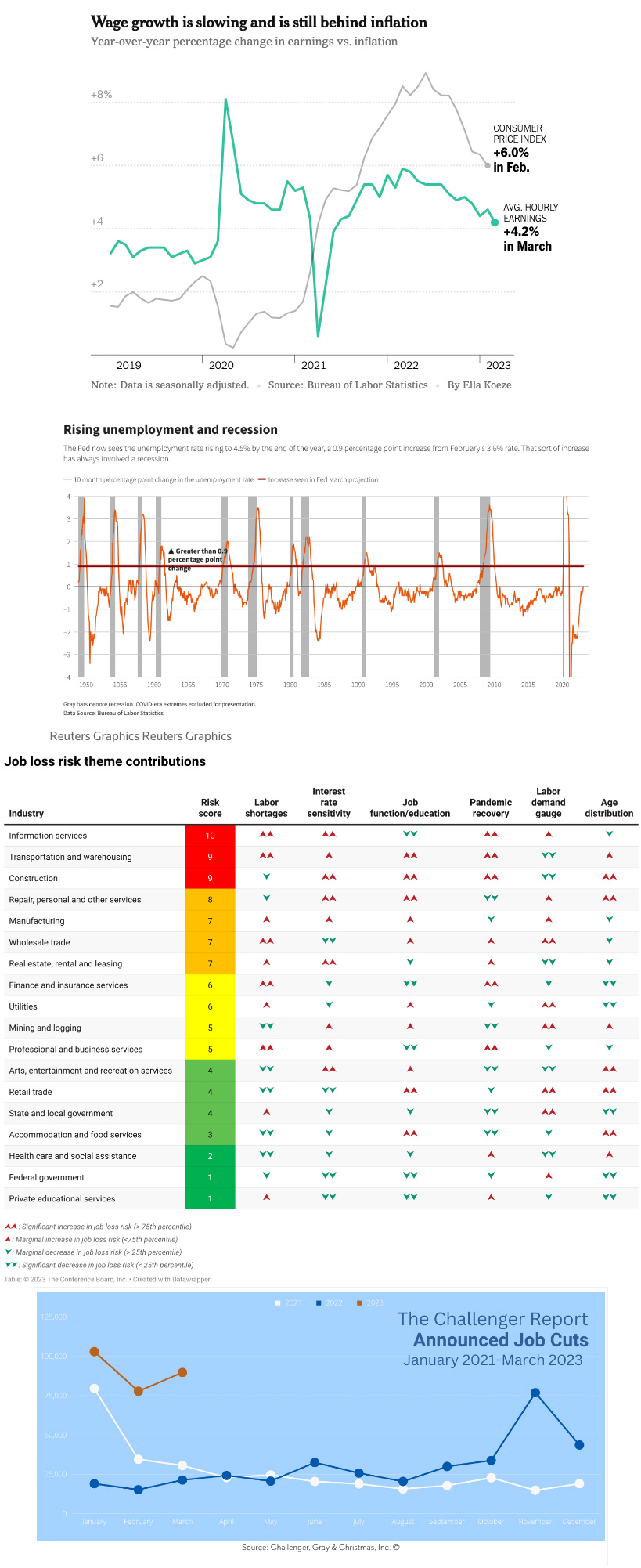

Despite the resilient jobs report, the consensus seems to be that the job market is, in fact, cooling down. Wage growth continues to slow, and the 3-month annualized wage growth was 3.2%. The standard target for wage growth is the Fed’s 2% inflation goal + about 1.5% “long-term productivity growth”. With this formula March’s numbers don’t seem to indicate wage growth is driving inflation, and certainly not the “wage-price spiral” economists were worried about just a few months ago.

Other indications we are in a deceleration: temp agency employment, a strong indicator of labor market conditions to come, declined for the first time in 3 months and has been essentially flat in 2023. Job openings data for February from last week’s JOLTS report showed open roles are decreasing, and February was the first time since June 2021 that fewer than 10 million jobs remained open at the end of the month. Finally, the average number of weekly hours worked (another statistic economists closely watch for signs of a labor market slowdown) fell in March from 34.5 to 34.4. LinkedIn reports that as labor markets cool down, job seekers are intensifying their search efforts, and in March 2023, the average number of applications per applicant in the U.S. increased 35% over last year.

While layoffs still remain historically low, we may be poised for an uptick. Labor hoarding might be artificially inflating jobs market strength by supporting extra spending throughout the economy. The question remains on how long employers can justify keeping extra workers on their payrolls as the economy slows. A recent report from outplacement firm Challenger, Gray & Christmas that showed U.S. job cuts in March increased by 15% from February. And just last week, the Conference Board launched its new Job Loss Risk Index: a tool to measure the likelihood of layoffs across the economy and which industries are most at risk. The Fed, for its part, expects unemployment to rise to 4.5% by the end of this year, an increase in magnitude that historically has always involved recession.

On the topic of recession, we’ve still got a mixed bag of opinions moving into the second quarter of the year. In analyzing the bond market the New York Fed is indicating about a 58% probability of recession in the next 12 months. Wall Street’s overall consensus is hovering around a 65% chance of recession, but Goldman Sachs is pegging the odds at closer to 35%. Forbes has built a helpful recession tracker, if you’d like to keep tabs on key indicators of economic health.

And as always we find some interesting anomalies in our analysis along the way. While many major employers have been laying off thousands of people, small businesses are growing in a significant way. In fact, 8 in 10 new hires in February were at companies with fewer than 250 employees. At the same time, the National Federation of Independent Business’s Small Business Optimism Index decreased in March to 90.1, marking the 15th consecutive month below the 49-year average of 98. Their survey of small business owners shows a group who, at the same time, see deteriorating business conditions. Credit availability has also tightened after last month’s sensational bank failures, which could make it harder for small businesses to access funding, and retain that talent.

Now on to next steps for the Fed, consensus is that it seems likely that we’ll have at least one more hike for 2023 before they slow their pace. Markets expect the Federal Reserve to hike rates 0.25% at their upcoming May 3rd decision predicting a 7 in 10 chance of a hike, with a 3 in 10 chance of holding rates firm. Forecasts from the central bank released last month also suggested one additional 0.25% rate increase is likely this year.

Although the likelihood is that the Fed hikes in May, predictions diverge beyond that point. The Fed indicates potential for a few more small hikes, while bond markets predict the Fed starting to cut by summer, likely due to greater economic instability than the Fed anticipates.

I’ll be keeping that recession tracker handy, in the next few months.

“Despite weakening in employment readings […] employment growth has not yet collapsed though there are visible signs of continued moderation […] In all the Federal Reserve will be pleased by the details of the employment report, but still is supportive of another rate hike in May — which we think could be the last for the tightening cycle. Followed by a long pause.”

– Nationwide Mutual Chief Economist Kathy Bostjancic

(Sources: CNBC, Economic Policy Institute, CNN, The Washington Post, Bloomberg, Marketplace, Yahoo!Finance, LinkedIn, Business Insider, Challenger, Gray & Christmas, The Conference Board, CBS News, Reuters, NBC News, Fortune, Forbes, Bureau of Labor Statistics, NFIB)

What else?

What else for April?

- Twitter commentary on the March jobs report from the EPI here.

- Even in 2023, children are working dangerous jobs that violate labor laws. Nearly 130,000 unaccompanied minors entered the US last year — three times what it was in 2017 – and they are ending up working in factories that produce Cheerios, Ben & Jerry’s ice cream and auto parts. Read the New York Times investigation.

- If you’re not feeling productive, you’re not alone: work about work takes up 58% of the workday, with skilled work taking up 33% and strategic work just 9%. Check out Asana’s 2023 Anatomy of Work Report for more analysis.

- Despite the many high-profile tech layoffs in 2022 (and 2023), the demand for tech talent remains strong. Read more in Dice’s 2023 Tech Salary Report.

- LinkedIn’s Future of Recruiting Report shares 17 trends and predictions for the coming year, and highlights the importance of internal mobility: employees at companies with high internal mobility stay at the organization 60% longer.

- A new Goldman Sachs paper finds that roughly two-thirds of current jobs are exposed to some degree of AI automation, and that nearly 300 million jobs could be lost or diminished if it delivers on its promised capabilities. Read more on the anticipated impact of job loss and creation, and what questions HR leaders should be considering, today.

- And, because it has resurfaced on my newsfeed lately, read a 2016 report on how the average American worker takes less time off each year than a medieval peasant.

(Sources: Economic Policy Institute, The New York Times, Asana, Dice, LinkedIn, Goldman Sachs, Business Insider)