Economic Update: February 2024

Change State Friends

Happy February!

We are now exactly halfway through winter, and depending on how much you like the cold and wet weather, February is either your winter playground or … you’re just really over it by now. I personally love the snow, but if you fall into the opposite camp, may I offer you some escapism via some 2024 travel inspiration, a checklist to prepare for spring gardening, or just a really good salad?

And if none of those fit the bill for your winter blahs, maybe just give your house a really good clean before the Lunar New Year begins this Saturday, and welcome in some new luck this coming Year of the Dragon.

Cheers,

Nicole

Economic Snapshot

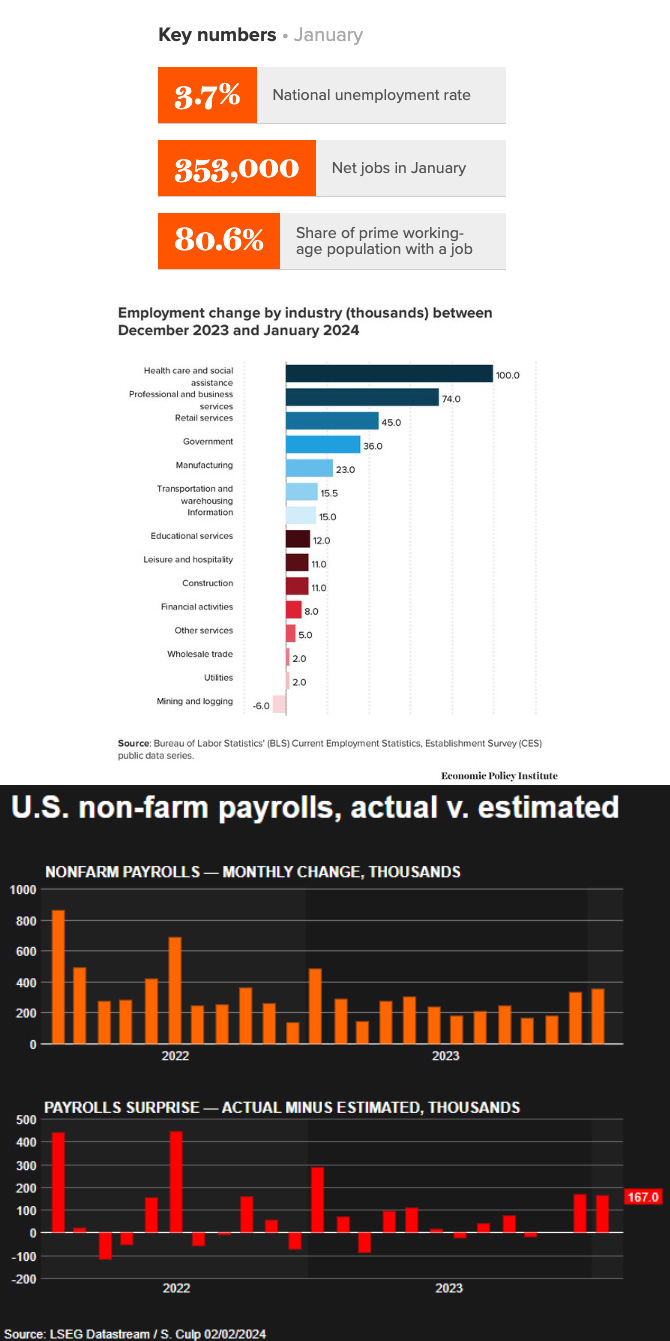

I’ve lost count of the number of times in the last year that a jobs report was referred to as “blockbuster”, and yet here we are again. January added an astonishing 353,000 jobs – a very strong start to the year – up from the average job growth of 255,000/month in 2023. The unemployment rate held steady in January at 3.7%, continuing a streak of 26 months in a row at a rate below 4.0%. Meanwhile, prime-age employment ticked up, and at 80.6% is once again above pre-pandemic benchmark. This report comes as a rather significant surprise, as economists polled by Reuters had forecast payrolls increasing by only 180,000 last month. November and December’s numbers were also revised upwards by a combined 126,000 jobs.

While annual revisions also reduced total 2023 jobs by 266,000, employment gains last year amounted to 3.1 million, well above the previous estimate of 2.7 million. Unemployment may have remained so steady in recent months (in spite of robust job creation) as new workers entering the labor market found employment quickly. Women and immigrants in particular have been fueling the labor market’s growth. But while 2023 generally paints a robust picture in terms of jobs gains, there is always data underneath the surface that complicates the interpretation. One such detail: 2023 was the year with the most months recording a downward jobs revision since the survey began in 1979. Experts less favorable on the long-term economic outlook point to this as a sign there is more weakness in the labor market than is currently reported.

In contrast to recent months, January’s jobs gains were across the board rather than tightly clustered in a handful of industries. In fact nearly two-thirds of industries increased payrolls, the most seen in about a year. Professional and business services added 74,000 jobs, healthcare payrolls rose by 70,000, retail increased by 45,000, and manufacturing hired 23,000 more workers. Mining and logging was the only sector to shed jobs in January. Every sector, including leisure and hospitality, is now less than 100,000 jobs from pre-pandemic levels. Finally, temporary help services employment – often the canary in the coal mine on labor market outlook – rebounded by 3,900, upending a 21-month streak of declines.

On the less rosy side, the average workweek fell to 34.1 hours, which, discounting the pandemic, was the shortest reported since June 2010. This is often a sign that layoff activity may be increasing as employers look to lighten their payrolls before permanently reducing staff. One possible culprit? Winter weather. More than 500,000 missed work in mid-January because of bad weather, the largest for any January since 2011. There was also an increase in the number of people who had full-time employment but were only able to work part-time. This probably partially explains the marked decline in January’s average workweek. And it may also be a contributing factor in the wage growth seen in January: when salaried workers work fewer hours, their average hourly pay also increases.

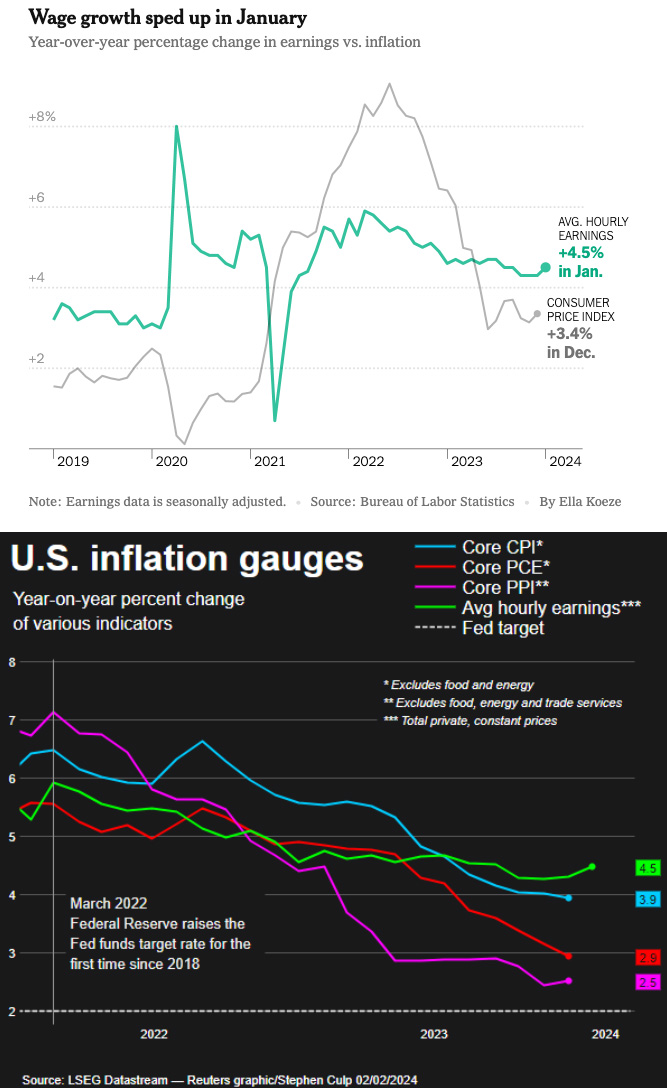

Indeed, last month saw average hourly earnings increase by 0.6%, the biggest gain since March 2022, and following a rise of 0.4% in December. Not great news for the Fed, as this means wage growth is higher than the 3.0%-3.5% range that most policymakers view as suitable for attaining a 2% inflationary target. However current quit rates, generally considered a reliable predictor of wage trends, have slowed to pre-pandemic levels. We could infer that if workers are less sure of their ability to leave and find new employment elsewhere, employers may feel less pressure to raise wages to hold on to talent.

Recent job gains have highlighted that employers are willing to keep hiring in response to sustained consumer spending. And, as we’ve seen in recent months, consumer sentiment continues to rise despite persistently high prices. The University of Michigan’s Index of Consumer Sentiment has surged in the past two months by the most since 1991. In tandem, consumer confidence reached its highest point in two years in the latest Gallup Economic Confidence Index, and The Associated Press recently found that 35% of American adults believe the economy is favorable, an increase from the 30% who agreed late last year.

“Corporate America hit the accelerator to meet the increase in demand,” said Joe Brusuelas, chief economist at the accounting firm RSM. “The economy accelerated in the fourth quarter of the year. We’re seeing a rational response by firms to meet that demand.”

“The overall picture looks to be one of a still quite strong labor market, and an economy starting 2024 with plenty of forward momentum,” agreed Michael Feroli, chief U.S. economist at JPMorgan in New York.

Despite significant publicity, most experts dismiss recent high-profile layoff announcements from companies like UPS, Google and Amazon. Historically speaking layoffs are still relatively low; those companies that received a boost in sales during the pandemic are now right-sizing as conditions stabilize.

Regardless, January’s numbers will not put the Fed at ease, and are more likely than not to delay any decision towards rate cuts. Federal Reserve officials left interest rates unchanged last month and suggested that while the next move is likely to be a cut, they’re planning to take their time. Reporting can be volatile, one month does not make a trend, and the Fed will be keeping an eye on hiring and wage growth numbers. “This is not a report that is commensurate with cutting in March,” said Lauren Goodwin, an economist at New York Life Investments.

To deliver that message to those who, presumably, don’t subscribe to an economic newsletter, Fed Chair Powell took to CBS’s 60 Minutes for an interview as the Fed occasionally does to highlight and comment on major developments. The “danger of moving too soon is that the job’s not quite done, and that the really good readings we’ve had for the last six months somehow turn out not to be a true indicator of where inflation’s heading.”

In light of Mr. Powell’s comments — and receding inflation — Kathy Bostjancic, the chief economist at Nationwide, indicated the Fed could still press on with rate cuts even in a robust labor market. “It seems like inflation is the primary driver …This should have a very modest impact on the timing — and even the degree — of rate cuts.”

Financial markets now see a 70% chance of the Fed cutting rates at its April 30-May 1 meeting. The Fed will also have a slate of several economic indicators to consider before their next meeting on March 20.

“Powell doubled down on the idea that a cut in March is ‘not likely’ given the information he has so far. This makes it crystal clear that his characterization at the post-FOMC press conference that a March cut is ‘unlikely’ was no slip of the tongue. That said, some of his remarks suggest a March cut isn’t off the table, either.”

– Anna Wong, chief US economist at Bloomberg

(Sources: Economic Policy Institute, Reuters, Yahoo Finance, The Washington Post, The Wall Street Journal, U.S. Bureau of Labor Statistics, SHRM.org, Bloomberg, Guy Berger via Substack, AP News, University of Michigan, Gallup, US News, Fortune, The New York Times, CNN)

What else?

What Else for February?

- X (née Twitter) commentary on the January jobs report from the EPI here.

- Gartner’s 9 Future Work Trends for 2024 looks at four themes reshaping work in the year ahead, including a shift in how employees view the EVP.

- New from Josh Bersin: HR Predictions for 2024, focusing on navigating persistent labor shortages, AI transformation and “employee activation” (empowering the workforce).

- Since we may as well make it a trio – another set of 2024 Global Talent Trends, this time from Mercer, highlighting how “relatable” organizations are bringing back the joy in work, and rethinking what matters most to employees.

- Fun fact: using ‘you’ rather than ‘we’ language in job ads might be hindering performance. New research from Textio analyzing over a billion job descriptions shows how job seeker behavior has changed in recent years, and what top-performing job descriptions look like today.

- Check out LinkedIn’s Jobs on the Rise for insight into the fastest-growing jobs in the last 5 years, a list that includes recruiters in the top 10.

- It’s probably not a surprise, but opportunities for remote work now skew heavily towards the highly paid. Read more on the recent analysis from HBR and learn how managers can best acknowledge and manage the work-from-home divide.

- In case you missed it: last week Elmo (yes, that Elmo) decided to check in and ask the internet how everyone was doing. He was probably not expecting the magnitude of the response.

(Sources: Economic Policy Institute, Gartner, Josh Bersin, Mercer, Textio, LinkedIn, Harvard Business Review, The New York Times)