Economic Update: July 2023

Change State Friends,

Happy July! Do you have a theme for the summer? For the remainder of this season, I’m determined to have a “slow summer”: trying to delay time a bit after these last few all-too-brief months and instead recall the long, lazy summers of youth. My goal is as much as possible, shut down the computer early to spend time working in the garden, take my daughter to the neighborhood pool before dinner, or head to the mountains for a long weekend in the sun. I hope you’ve found a summer theme that resonates with you, too.

As we move into this month’s analysis, you may have noticed there was no economic update last month. I took a pause in June as we suddenly and unexpectedly lost our beloved family dog to cancer. We’re firm believers here in putting family before work, and I’m grateful to our team for giving us the time and space we needed. Thank you to all our readers as well, and in honor of our Loki, please enjoy your July economic update.

Cheers 👋

Nicole

P.S. Do you have a great photo or story to share of your family dog(s)? We’re very much dog people here at Change State – we’d love for you to share! (Plus, my 6 year old would also be quite delighted) 🐾

Economic Snapshot

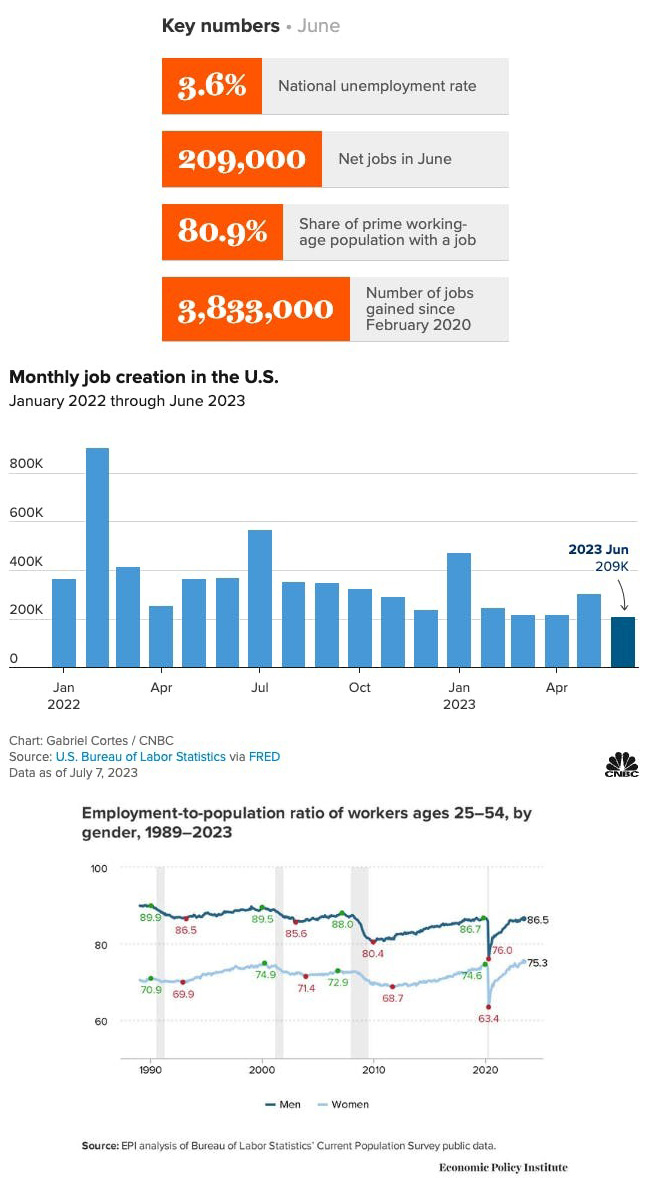

Payrolls increased by 209,000 in June: continued growth, yet falling below initial consensus estimates for 240,000. It also represents the smallest monthly gain in 2 1/2 years. Women’s prime-age EPOP (women ages 25 to 54 with a job) hit a series high at 75.3% in June, the highest reported since records began in 1948. This boost has been reinforced by prime-age women rejoining the labor market at record-breaking levels across the past two months. The labor-force participation rate, or the share of Americans who are working or actively seeking work, has stagnated for the last 4 months and remains below its pre-pandemic level of 63.3%. In part, this reflects an aging U.S. population that continues to drive ongoing labor shortages.

Black unemployment, sadly, ticked up again in June for the second straight month. After reaching a record low in April at 4.7%, it rose in May and then again in June to 6%. A large body of evidence shows that Black workers are the first to lose their jobs when the economy softens, though economists caution that month-to-month data on race can be volatile.

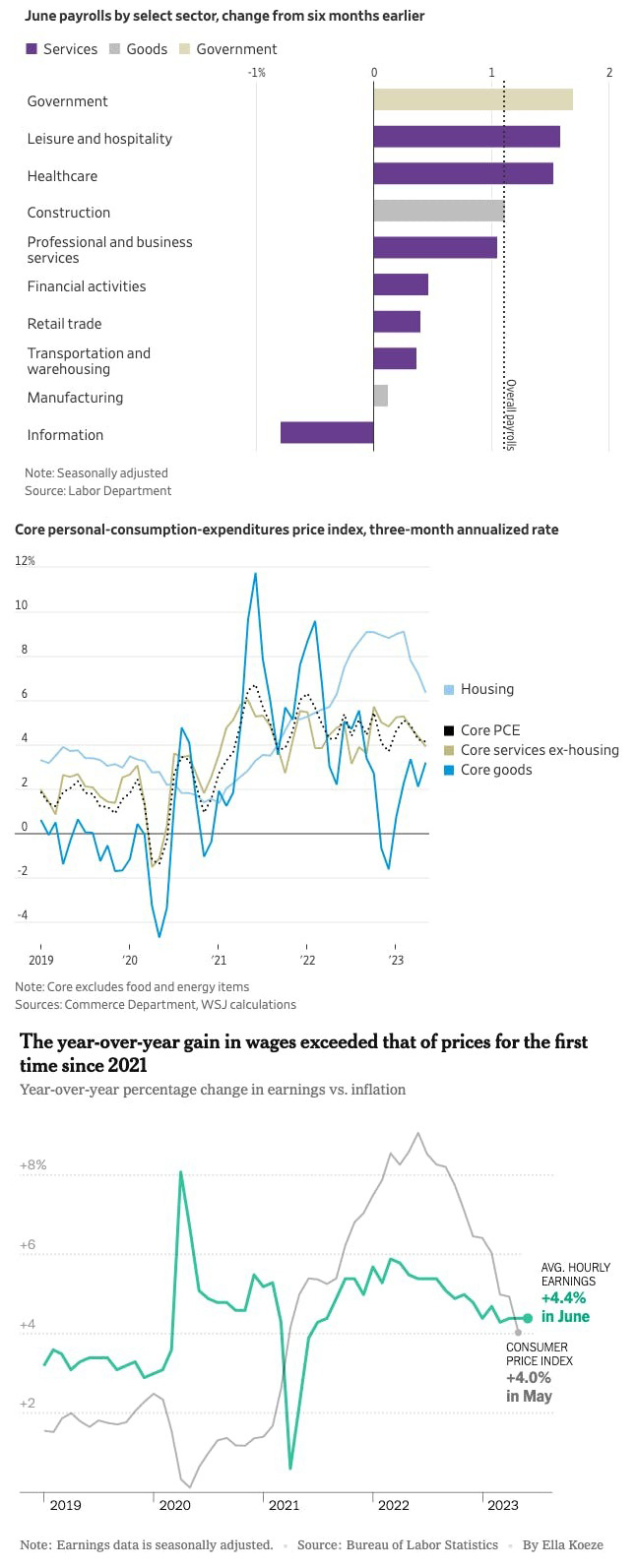

A significant share of last month’s gains were in the government sector, which added 60,000 jobs. State and local governments, after struggling to staff post-pandemic, made significant land grabs in June. Government employment grew at twice the 2022 pace in the first half of the year, as well as public schools and hospitals. Construction also saw robust gains, adding 23,000 jobs, in spite of rising interest rates.

Average hourly earnings increased in June, rising by 4.4% over the year, to $33.58 per hour. In fairness, average hourly earnings only rose 0.36% from the previous month earlier, (just barely exceeding the 0.3% forecast) and increased 4.35% from June 2022 (compared to a forecast of 4.2%). However these earnings gains are still well above the 3% to 3.5% target that’s in line with a 2% inflation goal, and Fed policymakers are closely monitoring all signs of wage growth.

June’s data accentuated labor market themes that have been with us for months: while job growth is progressively tapering, wage growth persists and unemployment remains low at 3.6%. Overall we’re seeing signs of cooling alongside a labor market that remains unusually resilient. In fact, economists have monikered June’s data the “Goldilocks Report”: not too hot, not too cold. Let’s look at some available evidence. While job openings are in fact cooling, the reported 9.8 million openings in May is still high by pre-pandemic standards. In 2019, for example, the monthly totals generally lingered around seven million. The economy has remained resilient likely because most of the U.S. economy is made up of services industries that tend to be less impacted by interest rate hikes. And despite elevated inflation and high rates, industries that are typically more susceptible to rising borrowing costs appear to have adjusted somewhat. For example, mortgage rates have nearly doubled since 15 months ago, but in recent months, housing has shown signs of reviving.

Simultaneously things are clearly slowing down. An obvious indicator that hiring is easing is that fewer industries are adding jobs. Excluding government hiring, private-sector job gains totaled only 149,000 in June, not exactly gains of a blistering pace. There are also other signs of cooling such as the “U-6 unemployment rate”, a measure of labor market underutilization that includes those working part time even though they would prefer full-time work. In June the U-6 climbed to 6.9%, the highest seen since August 2022.

And on the horizon, hopefully more good signs that will appeal to the Fed. This week, the Labor Department is expected to report that overall inflation fell to about 3% in June, the lowest in two years. Removing volatile food and energy prices, core inflation is expected to scale down to around 5% from 5.3%, an 18-month low. Economists also think core inflation could continue to abate to between 3.5% and 4%, in the coming months. The less good news is that reducing inflation further towards the Fed’s 2% target will prove more challenging if the economy keeps steaming ahead. The final stretch may prove more arduous (except for…*eyeroll*… those experiencing a “richsession”).

With all that being said, more expert chatter is coalescing around the U.S. sticking its much anticipated soft landing. Last fall Bloomberg Economics forecast a 100 percent chance of a recession by October, but has pivoted to suggest we’ll “narrowly dodge” a downturn in 2023. Only about two months ago 47% of economists working for corporations were predicting a recession by the end of the year.

“As long as the economy continues to produce more than 200,000 jobs a month, this economy is not going to slip into recession”, noted Joe Brusuelas, Chief Economist at RSM.

Last month the Fed elected to leave interest rates steady in June after raising them for ten straight meetings. At the time, many Fed policymakers were vocal in support of skipping a hike to “see more data before making decision”. However, officials also predicted in June that they would raise rates twice more in 2023 — and that the labor market would soften, but only moderately. Fed Chair Jerome Powell and other officials believe robust hiring is likely to keep inflation high because employers tend to then pass on their higher wage costs in the form of higher consumer prices.

In these last few days, Fed officials have provided more indication that further rate hikes are likely. Minutes from the June meeting released last week indicated most officials consider more hikes appropriate. In addition to strong hiring, core inflation remains a concern for the Fed: “Inflation is our No. 1 problem,” said Federal Reserve Bank of San Francisco President, Mary Daly.

While Nearly all Fed participants support additional hikes this year, there’s a notable outlier: Atlanta Fed Chief Raphael Bostic, who has called for holding fast for this year and “well into 2024”, as “inflation is still moving steadily back to target”. Many others agree: “This is not as strong of a jobs report as we had expected, but it’s representative of a labor market that is healthy and improving […] We’ve had millions of people return to the labor market [over the past year] and seen inflationary pressures fall without creating any job loss whatsoever” said Adam Ozimek, Chief Economist at Economic Innovation Group. Promisingly, the labor market and consumer inflation appear to be slowing in tandem, which could bring about the outcomes policymakers are looking for, if they can be patient in the meantime.

Fed officials will be watching today’s reports on consumer prices for June, as they prepare for a rate decision at the next meeting, July 25 and 26th.

“That’s the golden path — and I feel like we’re on that golden path”

-Austan Goolsbee, President of the Federal Reserve Bank of Chicago, on the possibility of reducing inflation while avoiding a U.S. recession

(Sources: Economic Policy Institute, CNBC, The New York Times, Axios, The Washington Post, CNN, Business Insider, The Wall Street Journal, The Guardian, Fortune, The Associated Press, MSN, USA Today, RSM, The Federal Reserve, PBS, Bloomberg, Reuters)

What else?

What else for July?

- Twitter commentary on the June jobs report from the EPI here.

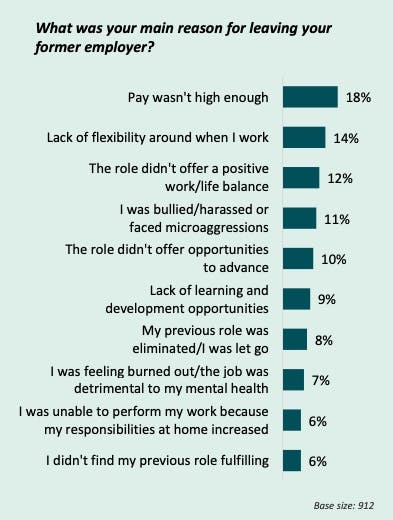

- Deloitte’s new Women @ Work 2023 researches the experiences of women in the workplace, around the world. While many are reporting reduced rates of burnout, many women still face limited flexibility at work, and more women have left jobs in the past year than in 2021 and 2020 combined citing flexibility as a top reason for their departure.

- What do the states that are currently reporting the most hiring have in common? They are all Republican-leaning states. There are a few reasons for the disparity, but one certainly is increased rates of job-hopping.

- Read General Assembly’s State of Tech Talent Report for insight into how talent leaders have been approaching the global tech talent shortage and best practices to help address critical talent needs.

- Explore how the evolution of the remote work labor market and local housing markets have affected urban and suburban migration patterns post-pandemic in the Economic Innovation Group’s new analysis.

- Most office workers in 2023 (59%) now work in a hybrid team. Check out this new Global Hybrid Working Report for more insights into how organizations can successfully navigate the pros and cons of hybrid work design.

- Candidate experience is a hot topic for TA right now – did you know that only 11% of Fortune 500 companies have an intuitive search and apply process that requires less than three clicks to apply? Check out Phenom’s 2023 State of Candidate Experience Report for more insights, and where organizations are making gains, today.

- For iPhone users, in case you haven’t heard, a new iOS update later this year will make some changes to Apple’s autocorrect functionality. In short, they announced you’ll soon be able to type that certain curse word (if you want to), without your messages being modified to say “duck” instead…an announcement met with much fanfare across the Twitterverse.

(Sources: Economic Policy Institute, Deloitte, The Washington Post, General Assembly, Economic Innovation Group, Insights.com, Phenom, Twitter)