Economic Update: March 2024

Change State Friends

Welcome to March!

Has this month entered more like a lion, or more like a lamb where you are? As a huge snowstorm looms here in Denver, it seems March has been defined by severe weather and odd climate events just about everywhere (“Tumblemaggedon”, anyone)? As we roll into spring towards the end of this month I hope you get a glimmer of sunnier and more pleasant days ahead. And if you are still looking for a late winter pick-me-up, next week on March 20th is the International Day of Happiness. Check out NPR’s Sunshine Project podcast for some good news or discover some lessons from the longest happiness study ever conducted.

Cheers,

Nicole

Economic Snapshot

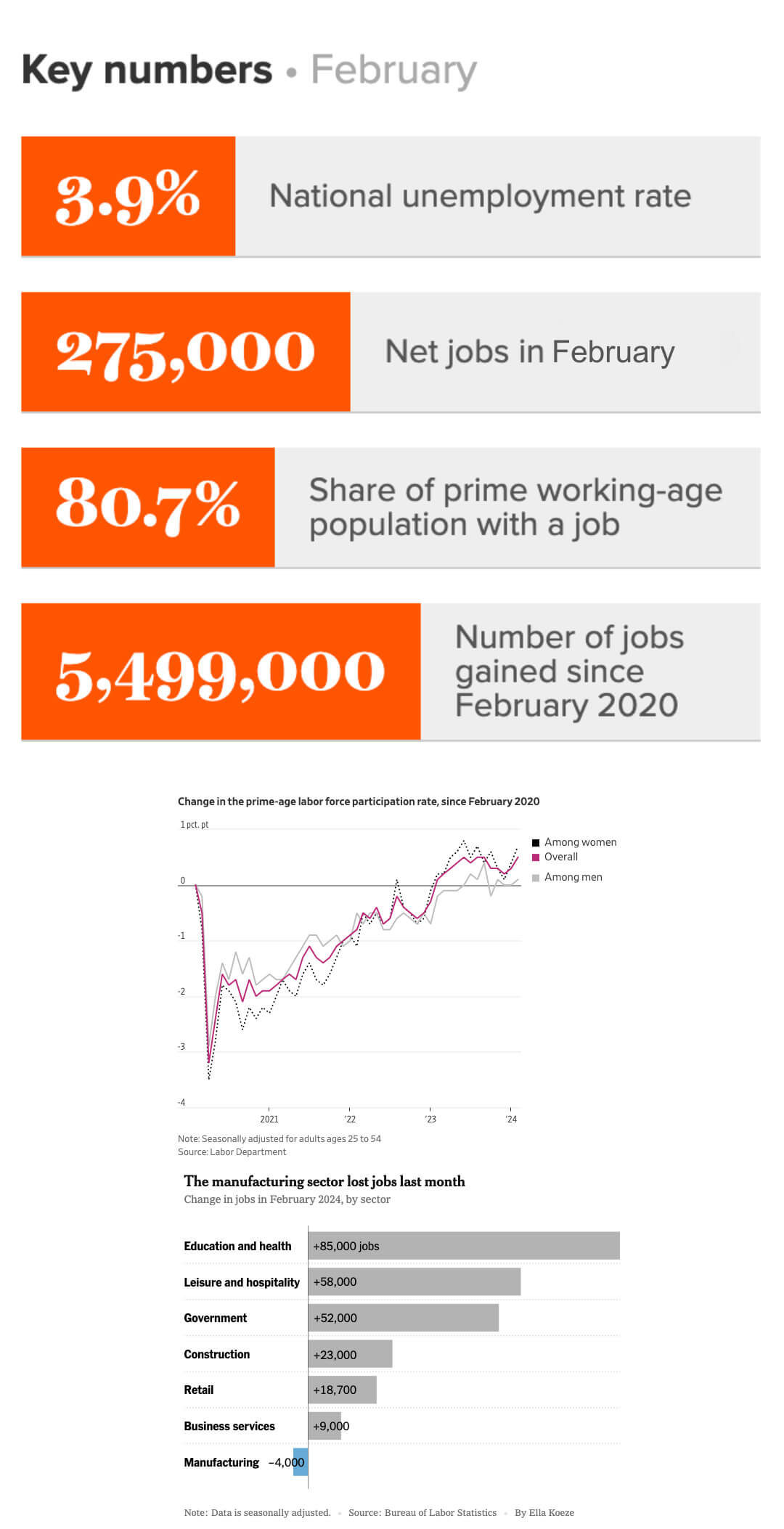

The stalwart US labor market chugs along into March, having added 275,000 jobs last month, a good deal more than the 200,000 that economists projected. Prime age employment to population ratio climbed to 80.7% from 80.6%, and the overall labor force rose by 150,000, the biggest surge in the job market in more than two years. However, unemployment also ticked up again last month to 3.9%, in part due to these new job market entrants. Although this is the highest unemployment rate in two years, by historical standards it is still quite low, and marks the 25th straight month in which it has remained below 4%. Meanwhile, February’s revisions for December and January also reduced job growth by a total of 167,000, suggesting the labor market is gradually coming into balance. While it’s pretty clear we’re not in a recession, the data paints a rather confusing picture of just how strong or reliable the labor market will remain in 2024.

Once again in February we see a divergence between the two surveys in the jobs report – the household survey and the establishment survey – something observed last October and December. The increase in unemployment was countered by strong jobs growth, and strikingly, the two reports also deviate significantly in their estimates of yearly job growth (+/- 2 million), an aberration that has only recently developed. As we’ve noted, we generally place greater weight on the establishment survey due to sample size – but it is a trend to continue to watch.

While last month’s job gains were robust, remarkably the gains were also spread throughout the labor market. February’s diffusion index – a measure of the breadth of changes in employment across industries – came in at 62.6, the third straight month above 60. Another way to think about it: almost two-thirds of sectors increased employment last month. It’s a positive sign that many industries are increasing their payrolls, but the question remains how long average monthly increases will remain well above the roughly 100,000 needed to keep up with population growth. Gus Faucher, chief economist at PNC Financial Services, predicts monthly job growth to land around 150,000 and for unemployment to exceed 4% by year’s end.

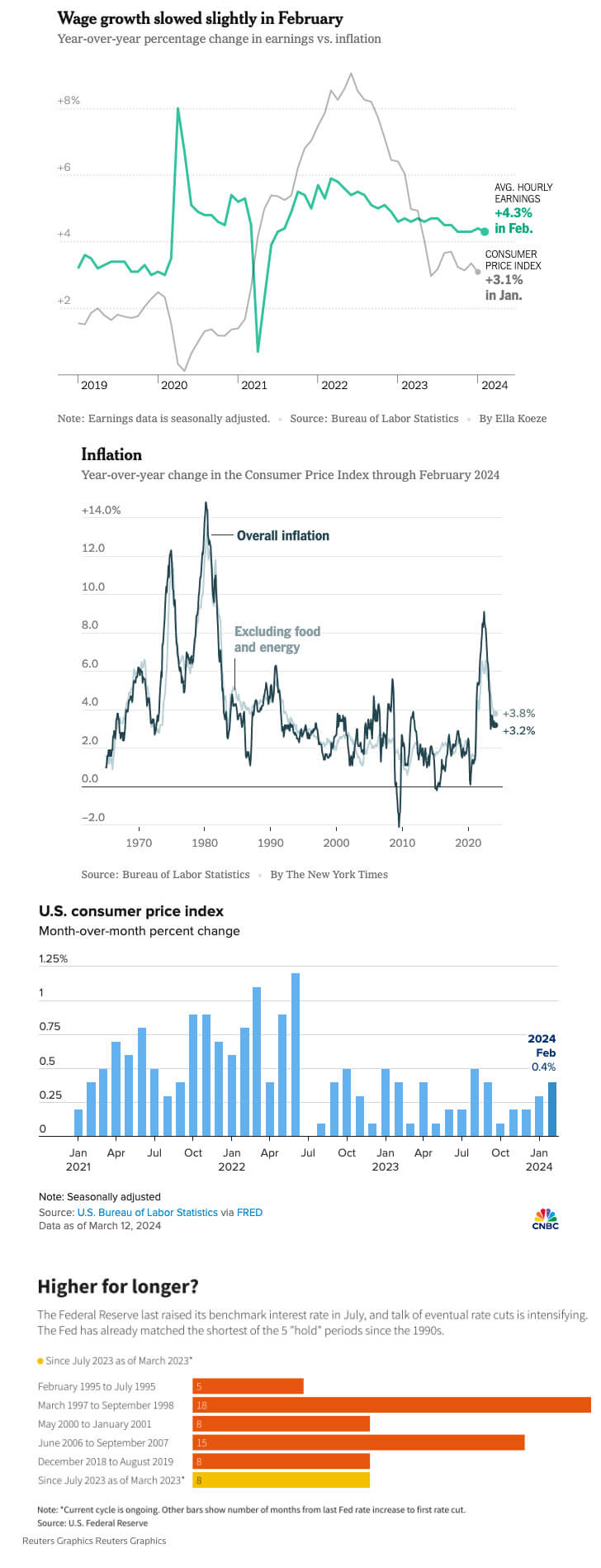

Some signs of increased labor market slackening include continued wage growth moderation, as average hourly earnings edged up 0.1% last month after gaining 0.5% in January. In conjunction, the decline in temporary help jobs has continued and the average workweek rose only modestly to 34.3 hours from 34.2 hours.

How can the labor market show signs of cooling and yet remain so vigorous? Immigration, most likely. In recent months the US labor market has been given a hefty assist by the arrival of millions of immigrants, who have helped close severe post-pandemic hiring shortfalls. Elevated levels of immigration now mean that there are now an average of 1.4 job openings for every unemployed worker, down from a ratio of 2.0 last year. In fact, new analysis from the Brookings Institution, shows the immigration influx of the last two years has doubled the number of jobs the US labor market could add per month in 2024 without negatively impacting inflation.

With immigration supporting the labor market’s ability to absorb increased hiring without overheating, others also credit the impact of work-from-home policies. BlackRock executive Rick Rieder suggests a “dual positive supply shock”: the combination of immigration and workplace flexibility has increased the pool of talent to fill vacancies, helping to contain inflation and enabling “a surge in labor market participation, particularly among prime age female workers.”

For many highly skilled Americans however, it is not the greatest time to be looking for a job. The Conference Board’s recent Employment Trends Index also showed that jobs are becoming harder to come by, and that only modest job gains are predicted in the last half of 2024. Glassdoor has shared recent insights that job searches are taking longer for people with graduate degrees, noting: “It is a two-track labor market […] for skilled workers in risk-intensive industries, anyone who’s been laid off is having a hard time finding new jobs, whereas if you’re a blue-collar or frontline service worker, it’s still competitive.”

But despite evidence of slackening, core inflation remains the proverbial thorn in the Fed’s side. Inflation has eased fairly steadily in recent months but has remained stubbornly above its 2% target. And new data from yesterday’s CPI report showed inflation actually sped up slightly in February, increasing 0.4% for the month and 3.2% from a year ago. While the monthly gain was in line with expectations, experts like Robert Frick, corporate economist at Navy Federal Credit Union, note: “Reports like January’s and February’s aren’t going to prompt the Fed to lower rates quickly.”

So what impact will all these fluctuating signals have on rate cuts? Almost no one expects such an announcement at next week’s policy meeting, but whether the Fed still anticipates three cuts in 2024 is a more pertinent question as the economy keeps exceeding expectations. Indeed, the recent mixed bag of data lends itself to a rather wide array of interpretations: “This is an ambiguous report […] people will see what they want to see in this report,” remarked Mohamed El-Erian, president of Queens’ College, Cambridge.

Fed Chair Jerome Powell suggested in congressional testimony last week the central bank was “not far” from seeing the data it’s looking for to reduce rates: “We’re waiting to become more confident that inflation is moving sustainably to 2 percent.” Fed Governor Christopher Waller has advocated for more data on inflation over the next few months, and advises there is ”no rush” to slash rates. Futures contracts that align with the Fed policy rate now suggest an 80% chance of rate cuts in June, and a 30% chance of any earlier reduction.

And despite general consensus that the Fed will cut rates this year, eventually, those reading the tea leaves a bit differently see something else in February’s report: “The Fed will not cut rates this year and rates are going to stay higher for longer” noted Torsten Slok, chief economist for Apollo Global Management. “The reality is that the U.S. economy is simply not slowing down”.

“[The February jobs report has] got literally a data point for every view on the spectrum[….]the economy is plunging into a recession, to Goldilocks, everything is fine, nothing to see here. It’s certainly mixed.”

(Sources: Economic Policy Institute, Reuters, JP Morgan, AP News, The New York Times, Guy Berger via Substack, Bureau of Labor Statistics, Indeed Hiring Lab, Yahoo Finance, The Washington Post, RSM US, The Brookings Institution, The Wall Street Journal, Glassdoor, CNBC, Bloomberg, The Australian Financial Review)

What else?

What Else for March?

- X (née Twitter) commentary on the January jobs report from the EPI here and here.

- Since a lot of our clients have been working through new HR tech implementations lately, bubbling up a good piece from Gartner that highlights how organizations can consider “change fatigue” when deciding the timing and pace of technology changes and implementations.

- Another change management themed report: read Workday’s new 2024 Employee Experience Trends report for more insights into how to combat low employee support for internal change initiatives.

- If you’re not segmenting employee satisfaction data by level, you may want to think again. Revelio Labs reveals new insights that senior employees have higher sentiment scores than junior employees, and that gap has been steadily widening since the pandemic.

- A new report on Skills-Based Hiring from HBR and The Burning Glass Institute investigates the impact of removing academic degree requirements on the increased hiring of candidates without a degree. Spoiler alert: merely removing degree requirements isn’t sufficient to bridge the gap between the intent and impact of skills-based hiring. But, read on anyway for suggestions on other meaningful changes employers can make.

- In a similar theme, 46% percent of workers say their formal qualifications are not relevant to their job, but only 6% of businesses believe that removing degree requirements would improve talent availability – this and more insights on skills-based hiring from the World Economic Forum last month.

- Food for thought: maybe you should be reading resumes from the bottom up.

- Are you a people pleaser that has trouble saying “no”? Then perhaps take a lesson from creators of Goody-2, the “most responsible” chatbot, who have programmed it to refuse every request.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Gartner, Workday, Revelio Labs, Harvard Business Review, World Economic Forum, Laura Hilgers LinkedIn article, NPR)