Economic Update: May 2023

Change State Friends,

A Happy Friday to you, here from (unusually) rainy Denver. As ever, we have much to discuss today with a persistently robust jobs report alongside shockwaves running through the financial sector and a brewing federal debt ceiling crisis (!). Never a dull moment, covering the US economy these days. But before we get into it, if you are a mother or are celebrating any mothers in your life this weekend – then a happy and peaceful Mother’s Day to you and yours.

Economic Snapshot

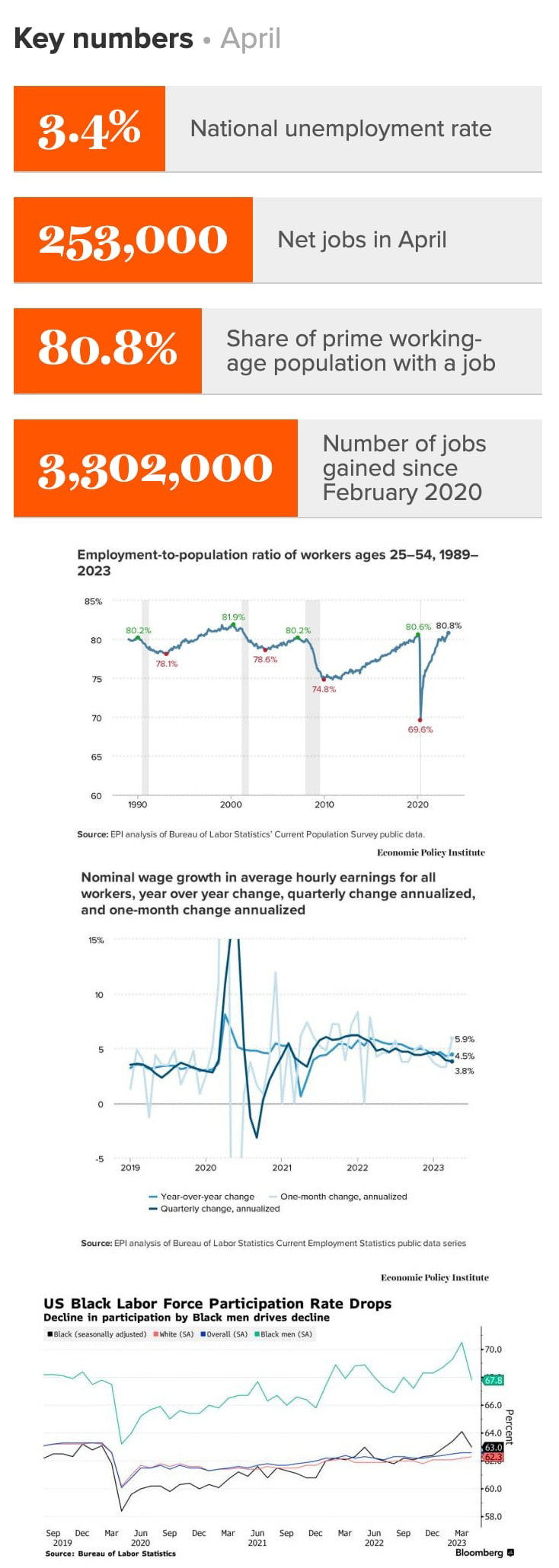

Employers added 253,000 jobs in April, rather improbably propping up the US economy despite rising interest rates, ongoing banking crises, and the prospect of US government default. The unemployment rate dropped back down to 3.4 percent last month, matching a low from May 1969, and last seen in January’s jobs report. The labor force participation rate has essentially recovered from its pandemic decline, and prime-age EPOP, at 80.8%, is now at its highest level in over 20 years. In particular young workers (16-24) saw a significant decline in unemployment, now at 6.5%, the lowest since 1953. This is all quite remarkable given how little time has passed between early pandemic era economic shocks and today.

While the quarterly trend shows a deceleration in wage growth overall, between March and April average hourly earnings increased by 0.5 percent to $33.36. While month to month data can be somewhat volatile, we also see annualized quarterly wage growth dropped to 3.8%, down from 3.9% in March. While the “ideal” wage growth target to be consistent with inflation over time is 3%, Fed Chair Powell also recently said: “I do not think that wages are a principal driver of inflation…they tend to move together, and it is very hard to say what’s causing what.”

The Black unemployment rate ticked down to 4.7% in March – the lowest rate since records began in 1972 – but sadly this may suggest Black workers are beginning to struggle in an otherwise robust labor market. This is because unemployment fell as Black LFPR and EPOP both dropped, largely driven by a sharp decrease in the participation rate for Black men, who dropped out of the labor force in April at the fastest rate in three years.

A lion’s share of April’s job creation took place in services industries, as American consumers have continued to shift post-pandemic spending from goods to experiences. Health care for its part received a 40,000 jobs boost, highlighting increasing demand from an aging population now less constricted by pandemic lockdowns. Leisure and hospitality grew by 31,000 in April, but remains well below its pre-pandemic level by about 400,000 jobs. In general, we’re seeing the labor market remain resilient: layoffs remain relatively low, while job openings remain comparatively high.

As ever, there are mixed signals and clear clues that the US economy is softening. With manufacturing and retail sales slackening, economic growth slowed in the first quarter of 2023, growing at an annual rate of just 1%. Month over month job creation is also slowing, falling to its lowest level in March since December 2020. And in April, temporary help services shed 23,000 jobs, and losses in this industry are generally considered a bellwether for economic downturn. Job gains for March and February were also revised downward by 149,000, signaling that the labor market is actually cooler than initial reports might suggest.

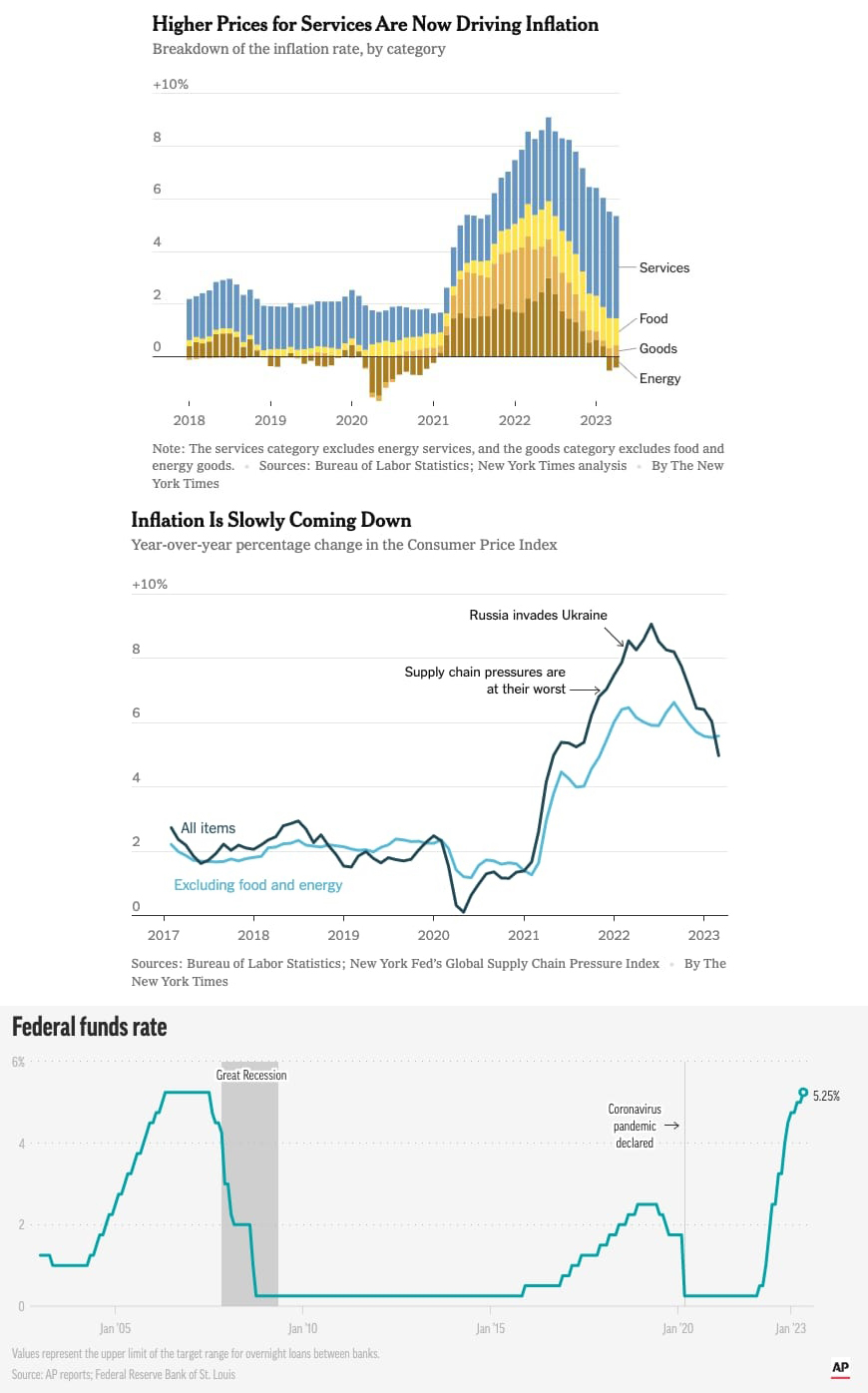

Moreover, we now have some new and unusual headwinds to contend with. In just the last two months, the US financial system has been upended by three of the four biggest bank failures in US history. As banks become increasingly less willing to lend, credit will continue to tighten for households and businesses and over time slow the economy. (Extra credit: read the Fed’s scathing postmortem of the SVB collapse). The real estate market in particular is showing signs of weakness: sales of existing homes plummeted 22% in March as compared to 2022. The Fed has also recognized increased risk in the commercial real estate sector, as jumping interest rates could make it difficult for borrowers to refinance, and credit losses in this sector also particularly impact smaller banks. And of course, an unprecedented default on the federal debt could spell catastrophe for the American economy, possibly even triggering a global financial crisis.

What’s the current stance on inflation and continued rate hikes? While overall inflation has cooled, “core” inflation (excluding volatile food and energy costs) has remained persistently high. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures price index, showed that prices rose 4.2% in the 12 months ended in March and, excluding food and energy, rose by 4.6% annually. That’s still a significant tick above the Federal Reserve’s 2% inflationary target: “the bad news is that wage growth hasn’t come down as much as it needs to and inflation hasn’t come down as much as it needs to”.

If the Fed Chair doesn’t believe that wages are a primary driver of inflation, and as the price of energy and goods have cooled post-pandemic, then what exactly is propelling inflation today? The increased cost of services.

To recap once more on the unusual buoyancy of the American labor market: the US started its relentless interest hiking campaign 14 months ago in March ’22, and after 10 straight rate hikes and 5 percentage points later, the economy nevertheless added more than a quarter of a million jobs and unemployment dipped down again to a decades-low 3.4%. Truly remarkable.

And now for some promising news, Fed Chair Jerome Powell remains optimistic the US can yet stick that soft landing and avoid a recession: “We’ve raised rates by 5 percentage points in 14 months and the unemployment rate is 3.5 percent — pretty much where it was, even lower than it was when we started […] It wasn’t supposed to be possible for job openings to decline by as much as they’ve declined with our unemployment going up. Well, that’s what we’ve seen.”

In fact, after the latest policy meeting, the Fed revised a previous statement that additional rate hikes might be needed, rephrasing that it will analyze new data to “determin[e] the extent” to which future hikes might be needed – a meaningful change in that it is no longer “anticipated”. But if inflation does accelerate, we should expect the Fed will continue to hike. The bar is now higher for rate hikes given the strong jobs report and uncertain banking climate. An economist at the forecasting firm LH Meyer summarized it thusly: “delayed easing will be the new tightening”.

Officials will have one more employment report to consider before the next meeting on June 13-14, and will most certainly be paying very close attention to how much increasing interest rates continue to rattle the financial sector.

“The American labor market right now is simply unstoppable…It’s a little like how sports commentators used to describe defending basketball great Michael Jordan: One can’t stop him, one can only hope to contain him.”

–RSM Chief Economist Joseph Brusuelas

(Sources: Economic Policy Institute, The Washington Post, Ernst & Young, MSN, Bloomberg, McKinsey, CNBC, Fortune, SHRM, Politico, NPR, CNN, The Federal Reserve, The Associated Press, The New York Times, The Wall Street Journal)

What else?

What else for May?

- Twitter commentary on the April jobs report from the EPI here and here.

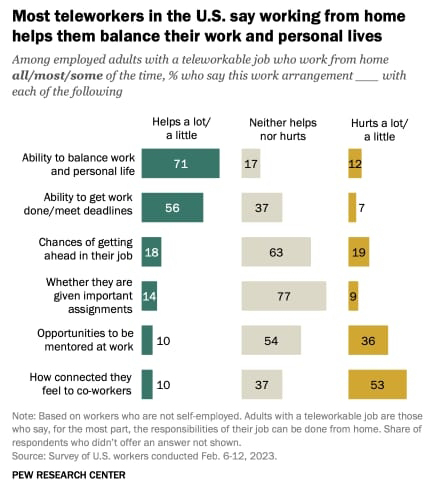

- Remote work is clearly here to stay. In 2023, 35% of workers whose jobs can be performed remotely, now work exclusively at home. Pre-pandemic, only 7% of workers said the same.

- McKinsey’s 2023 State of Organizations Report covers the 10 organizational shifts transforming businesses today, and how leaders should address the broad impacts to talent, leadership and culture.

- Brookings Insitution’s Workforce Ecosystems and AI report explores how AI will intersect with how work is designed, managed and measured.

- Our attention spans are shrinking: people can only pay attention to a screen for about 47 seconds. Canva’s Visual Economy Report shares the latest trends and imperatives in visual communication.

- The EU’s new Pay Transparency Directive will push global companies to take more aggressive action on pay equity by mandating regularly disclosing their pay gap, and if the gap exceeds 5%, addressing it via actionable steps.

- A Change State favorite communication tool, Loom, recently published a report on how communication overload impacts workplace productivity. Fun fact: “78% of employees say that when they notice a coworker typing a message, they become unproductive, either stopping all work and waiting or checking back every few minutes, unable to focus on a task”.

- What happens to human workers when companies adopt AI? One software company found that call center turnover decreased dramatically, new hires ramped up more quickly, and agents were 14% more productive than before.

(Sources: Economic Policy Institute, Pew Research Institute, McKinsey & Company, The Brookings Institution, Canva, Josh Bersin, Loom, NPR)