Economic Update: May 2024

Change State Friends

A Happy May to you all, and I hope spring has brought you something to celebrate – be it Mother’s Day, warmer weather, outdoor exercise, or a rare dual cicada emergence? Our family has something sweet to celebrate this coming weekend – we’re finally welcoming a new puppy to the family after losing a very special dog this time last year. We are all very excited, though perhaps a bit nervous to be entering the puppy phase again after such a long break. I do know one thing however – nothing goes better together than puppies and springtime. And if you’re a dog lover like our Change State team – here’s some food for thought on whether your dog might need more friends. As for now, there’s lots to get into on the economy so let’s dive in paws first.

Cheers,

Nicole

P.S. And if those cicadas are terrorizing you where you live, you can do as the old saying suggests when life hands you “lemons”… find a way to eat them.

Economic Snapshot

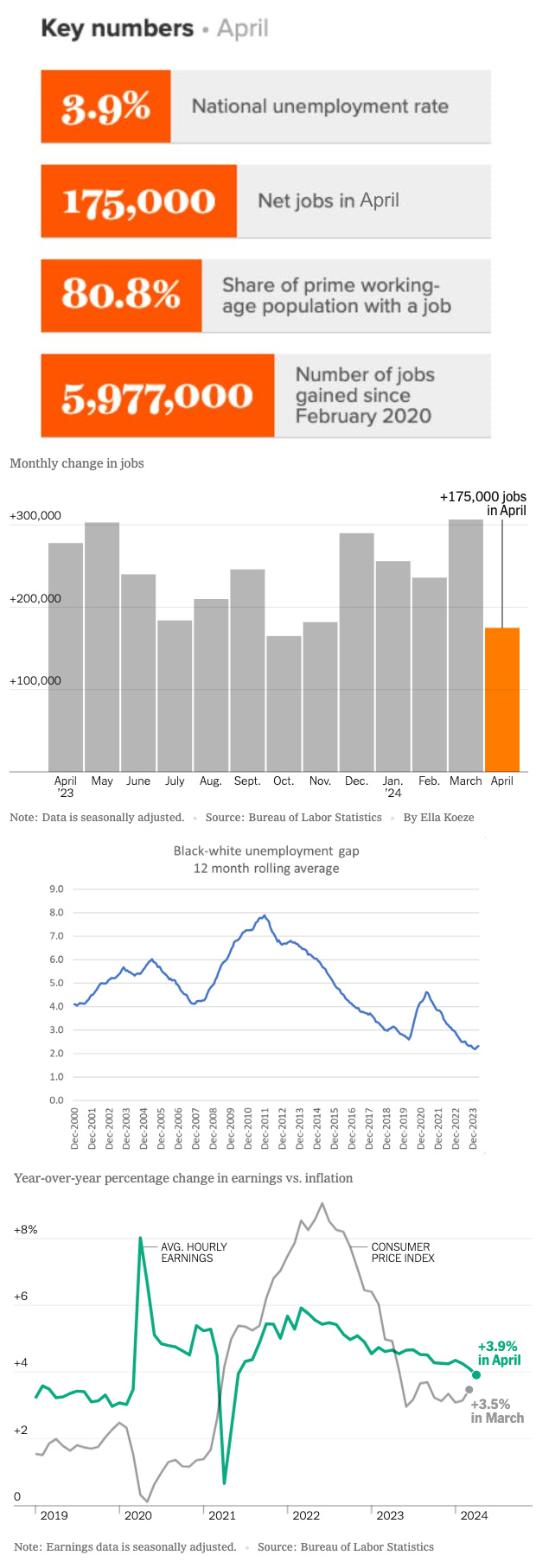

The economy added 175,000 jobs in April, representing a sudden shift from the outsize gains earlier this year, and coming in well below the 240,000 economists had expected. In fact, last month’s numbers were the lowest reported since October 2023. While April’s gains are still well above the historically recognized breakeven level of 100,000, it would seem jobs growth is slowing as the economy nears full employment. However, there’s been a lot of discussion lately on whether the recent influx of immigration has recalibrated “breakeven”, and even the US Treasury believes that level now sits closer to 200,000. The unemployment rate ticked up to 3.9% as the overall employment-to-population ratio dropped slightly last month. One bright spot to note in the report: the share of women 25-54 years old with a job hit an all-time high in April at 78%.

While an increase in unemployment can be worrisome, it’s remarkable that unemployment has remained below 4% for 27 straight months now, a feat not achieved since the 1960s. Something else to celebrate from April is Black unemployment dropping back down to 5.6%. This is a hopeful sign as Black workers’ employment has historically been first at risk during an economic downturn and the increase in recent months has been troubling.

While the overall pace of hiring appears to have slowed, the economy is still seeing pretty broad-based growth as more than 60% of sectors reported gains. Warehousing and transportation in particular are seeing a resurgence after a post-pandemic dip in e-commerce, adding 22,000 jobs last month. One surprise however, is that April brought a significant sea change for leisure and hospitality with merely 5,000 added in comparison to 53,000 gains in March. This sector had otherwise been a significant contributor to total jobs growth in recent months.

The Fed should also see welcome news in the deceleration of wage growth, as average hourly earnings rose just 3.9% year over year in April, compared to 4.1% in March and 4.3% in February. Most economists had predicted a 4% YOY increase, and the continued tapering in wage growth is strong evidence that the labor market is not reheating. In fact, April’s gain was the weakest since May 2021.

There are other recent signs that the job market is starting to moderate. Last week’s JOLTS report showed job openings dropped to 8.5 million, the lowest number reported in three years. Admittedly, it’s still high by historical standards as prior to 2021, openings had not exceeded 8 million. Temporary help jobs also fell by more than 16,000 – a possible indicator of labor market inflection as wary employers often rely on flexible labor during uncertain times.

Several non-governmental reports reveal a softening labor market as well. The Conference Board’s employment trends index fell to 111.25 in April following a downward revision in March: “The labor market is beginning to show signs of cooling following a period of very strong growth since the pandemic recession.” Indeed’s Job Postings Index found that employer job postings were down 12% year-over-year. Also the Burning Glass Institute’s director of economic research notes that with fewer vacancies and a declining quits rate: “this really is a cooler job market than a year ago”. And to be sure, if we are to see interest rates fall, we should all welcome any signs of a gradual slowdown.

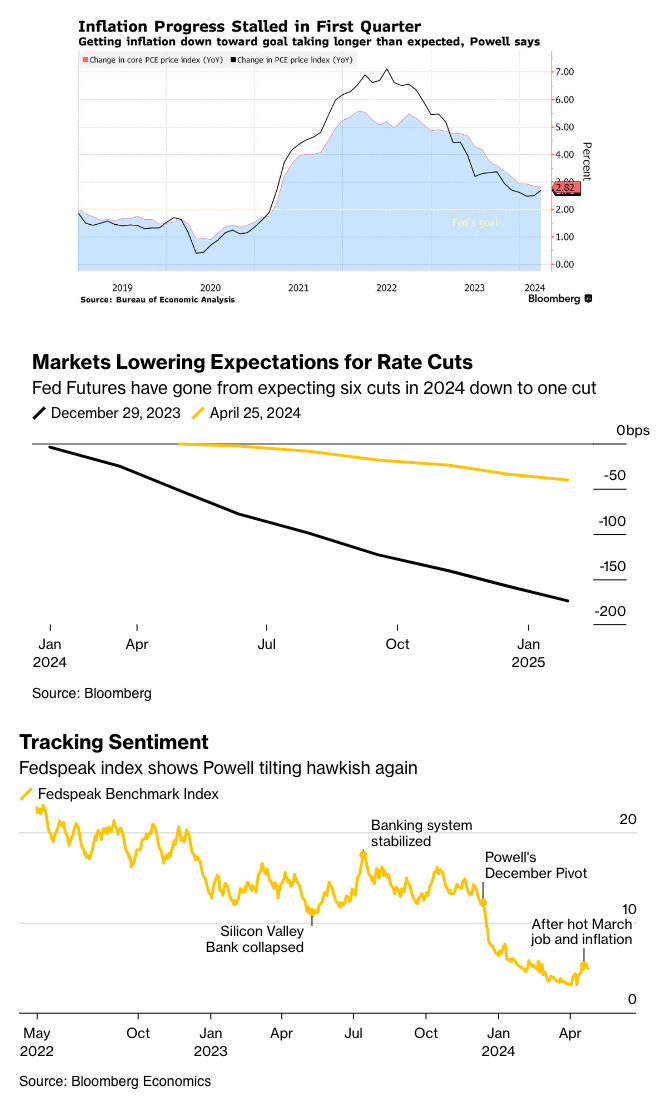

At last week’s FOMC meeting, officials voted to keep interest rates at 5.3 percent. Heading into 2024 the central bank hinted at several rate cuts across the year. But since then, inflation has remained tenacious, and if the labor market refuses to slacken that could delay cuts for several more months. Conversely, evidence that the job market has suddenly cooled could hasten cuts, however “It would have to be meaningful and get our attention and lead us to think that the labor market was really significantly weakening for us to want to react to it,” said Fed Chair Powell, noting that a small increase in unemployment such as we saw in April would not be sufficient to change course.

Mr. Powell does believe the restrictive policy is working however, referencing the slowdown in hiring and declining numbers of workers quitting their jobs. He also suggested that current inflation numbers have remained stubborn despite the slowdown in housing rents, as this is lagging data that has not yet appeared in official inflation measures. The Fed’s preferred measure of core inflation, the core personal consumption expenditures price index, most recently came in at 2.8%. “Of course we’re not satisfied with 3% inflation …[however] evidence shows pretty clearly that policy is restrictive and is weighing on demand,” noted Powell, referencing the recent JOLTS report which shows US job openings at a three-year low.

By and large, most experts highlighted the favorable in April’s report:

- “This is the jobs report the Fed would have scripted […]Today’s weaker numbers need to mark the start of a new slower trend for multiple rate cuts to seriously be back on the agenda, but by then the new fear could be a slowing economy,” said Seema Shah, chief global strategist at Principal Asset Management

- “The more jobs reports you get like this, the more confident we can be that the economy is not overheating,” commented Austan Goolsbee, the president of the Federal Reserve Bank of Chicago

- “One month does not make a trend, but today’s jobs report likely gives the Fed some much-needed assurance that higher rates may be starting to do their job,” noted Jason Pride, strategist at asset management firm Glenmede

Recent Fed commentary aside, some intriguing new data may reveal some skepticism lurking in the senior central banker’s outlook. Powerful words from a powerful seat can have reaching effects, something Bloomberg Economics’ new Fed sentiment index aims to track. Supported by a natural language processing algorithm, the index scans speeches and headlines and scores them on a scale from ultra-hawkish to super-dovish. Bloomberg’s analysis suggests that Powell’s December hints at rate cuts gave markets a boost and even avoided a US recession (!). But with current inflation stuck above goal, Powell has required a sudden change in position. Bloomberg even suggests this December pivot may have avoided a downturn at the price of adding to the inflationary problem (really a thought-provoking read, if you click on just one link today!).

Most experts now predict the Fed will cut rates once, with an upside to twice this year, the first falling in September. Estimates of a September cut sit at roughly 70%, according to CME Group, with an outside chance of 36.6% in July if the labor market plays its cards right.

The next FOMC meeting is scheduled for June 11-12, and we’ll have three more key reports for officials to weigh before their next decision.

“Are there signs that the labor markets are reheating? Not really…The case for weaker inflation is still strong, and until that changes, the Fed should maintain a dovish bias, quite frankly.”

(Sources: Economic Policy Institute, The Wall Street Journal, Treasury.gov, The New York Times, MSNBC, The Washington Post, Reuters, Indeed Hiring Lab, AP News, Guy Berger via Substack, Forbes, Fortune, Axios, Bloomberg)

What else?

What Else for April?

- X (née Twitter) commentary on the April jobs report from the EPI here.

- Deloitte’s annual Women at Work report is rather sobering. More than 50% of women say their stress levels are higher than a year ago, and are concerned or very concerned about their mental health. And only 1 in 10 feel they can openly discuss the need for greater work flexibility with 95% believing that requesting or utilizing flexible working opportunities affects their promotion prospects.

- A new Gartner article outlines five primary approaches to deploying GenAI in HR and explores the current use cases and practical applications including key questions HR teams should be asking tech vendors.

- An interesting article showcasing how today’s organizations are supporting “returnships” such as Chevron’s “Welcome Back Returnship Program,” which assists experienced professionals in re-entering the workforce after a career break.

- A new MIT case study details how Johnson & Johnson leveraged artificial intelligence to assess its workforce’s current skills to guide employees’ career development and leaders’ strategic workforce planning.

- Take a peek at the future of hiring in the 2024 Workday Hiring and Talent Trends report, on why the hiring slowdown may be ending soon, and how that impacts the outlook on talent acquisition in 2024.

- In response to sustained public backlash, many major companies are scrubbing “DEI” from filings and proxy statements, listing DEI as a “risk factor” in shareholder reports or removing mentions of diversity goals outright. Check the article for more insights into how many employers are rebranding their diversity efforts as “inclusion”.

- Check out Aspen Tech Labs Q1 US Jobs Report for insights into labor market and salary trends from the beginning of the year.

- Love a good scandal? Read on for how one vegan blue cheese upended a prestigious food award.

Do you know someone who would like this newsletter? Share it with them.

(Sources: Economic Policy Institute, Deloitte, Gartner, WorkLife, MIT Center for Information Systems Research, Workday, The Washington Post, Aspen Tech Labs)