Economic Update: November 2023

Change State Friends,

It’s (finally?) fall, y’all. The weather has been bouncing around here in Denver – from 80 degrees, to snow, and back again twice in the last two weeks. Hopefully, the weather where you are from has settled into a more predictable pattern, and you’re enjoying the cozy feeling of fall, whatever that means to you. Some changing weather, too, to discuss in this month’s newsletter. But first, since I love to share a good seasonal recipe – here’s a favorite in my fall rotation.

As for the economy, let’s rake up the leaves and get into it.

Cheers, Nicole

P.S. A happy Veteran’s Day, to those who have served and their families. For your service, your bravery and your hard work, we thank you.

Economic Snapshot

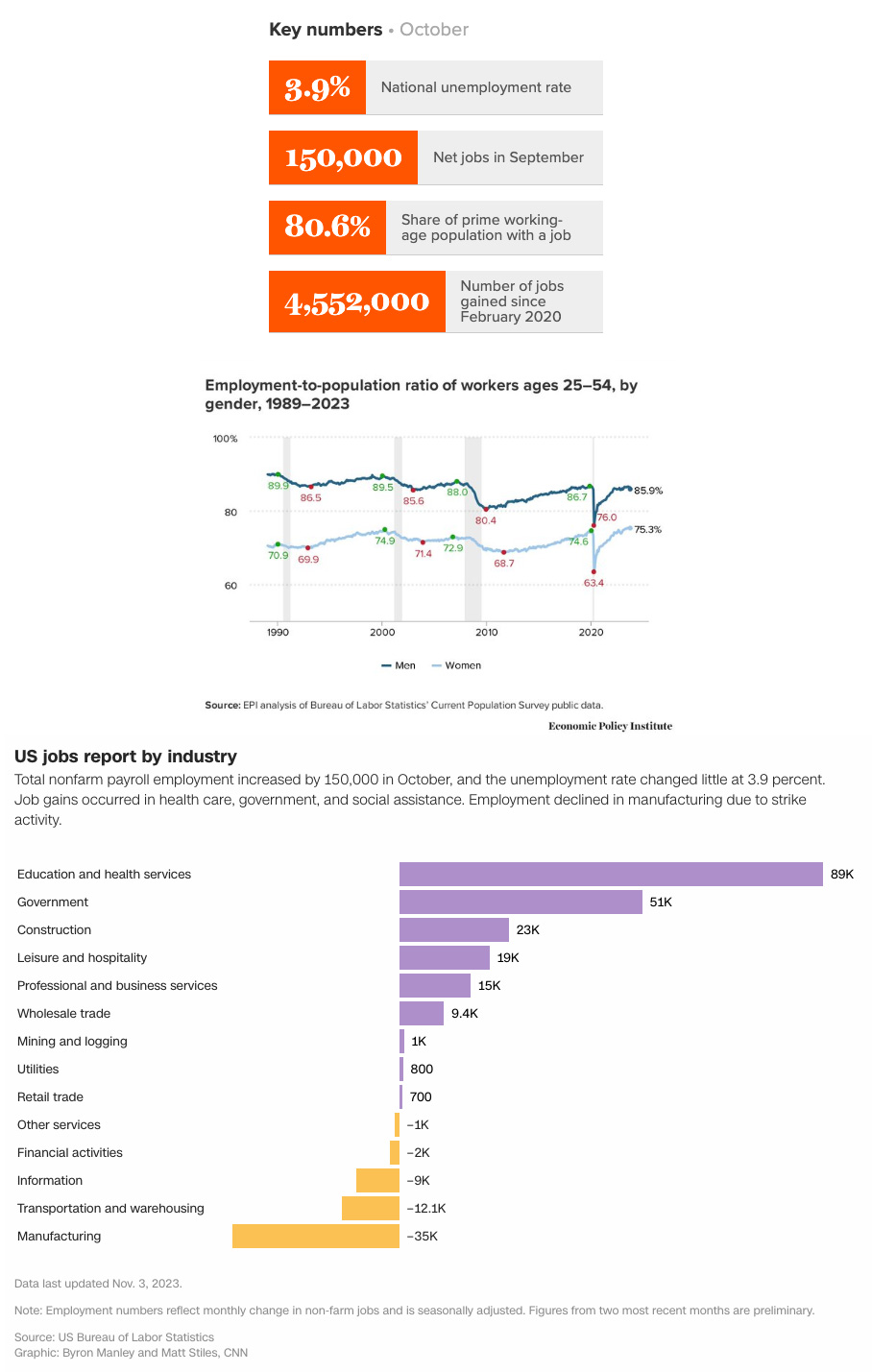

A mixed bag arrived in last week’s jobs report with the household and establishment surveys telling different stories. October saw payroll gains of 150,000, alongside an increase in unemployment and a reduction in LFPR. Job gains fell below expectations, which were closer to 180,000, and unemployment ticked higher to 3.9%, the highest since January 2022. Though that’s a somewhat foreboding sign, we should remember it has remained below 4% for nearly two years, a feat not replicated since the late 1960s. EPOP fell to 80.6%, the lowest since February, matching its pre-pandemic level. The losses in the prime-age employment-to-population ratio in October primarily affected men, while women’s employment rate remains significantly higher than ever. Finally, the job totals for the last two months were revised downward by more than 100,000. Initially reported at 336,000 openings, September was reissued at 297,000 and will be revised again next month.

Job gains were strongest in health care and social assistance last month, with 77,000 jobs added, nearly half of October’s total gains. Government added 51,000 jobs, but while overall jobs in this sector have rebounded to pre-pandemic levels, state and local jobs (particularly teachers) remain 0.4% under. Leisure and hospitality, which saw robust gains last month, added only 19,000 positions. The notable decline in manufacturing employment is unsurprising given the recent UAW strike, which likely reduced payrolls by around 30,000 in October. With a successful resolution, we should expect those workers to reappear in the data next month.

October’s rise in the unemployment rate suggests a possible increase in layoffs – something that until now, most employers have generally avoided. However, last month’s household survey showed a 200,000 increase in job losses or completed temporary assignments and that the number of layoffs increased in October by 92,000. In addition, some 96,000 people reported being out of work because of a strike or labor dispute in October, the most reported since 1997.

[A brief note on the divergence between October’s two surveys. The monthly jobs report contains two surveys: one surveys businesses about employment, hours and earnings, while the other inquires households about their status in the labor force. When the surveys show conflicting data, it’s standard practice to rely more heavily on the establishment survey because the larger sample size generally supports more precise estimates. The household survey’s smaller sample makes it more volatile, but it can also be an early indicator of turning points in the economy.]

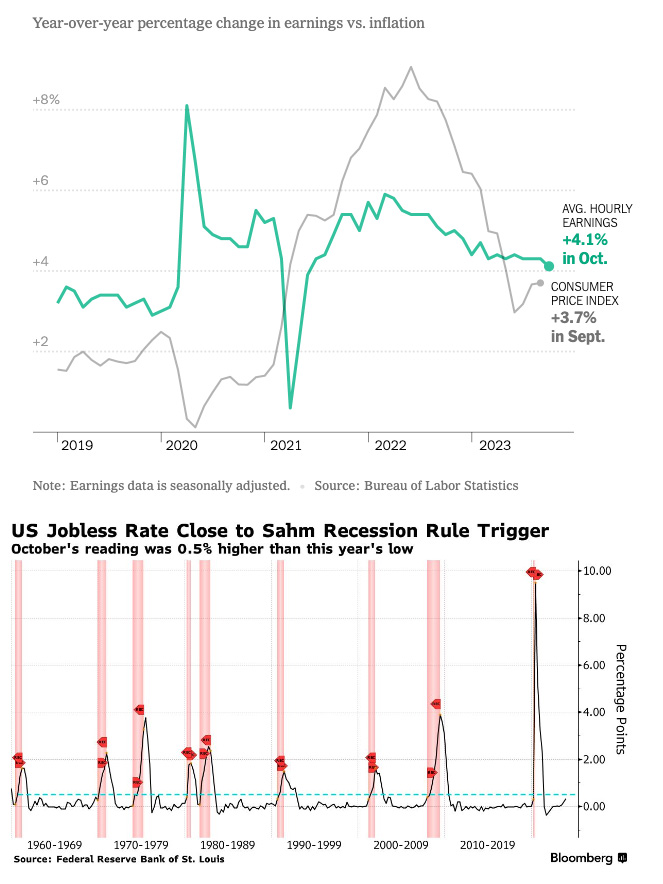

Wage growth continued to slacken in October, a data point that the Fed is watching closely. Average hourly earnings increased by 0.2% from September, which is less than economists expected and shows deceleration from September’s 0.3% gain. Annual wages rose by only 4.1% last month, the slowest pace since June 2021. October’s report also noted that the average workweek dropped slightly, indicating companies aren’t trying to squeeze more productivity from existing employees. Coupling wage data with the slowdown in hiring and increased unemployment, it would seem reasonable to believe some inflationary pressure is easing, and the job market has begun to slow its engines.

As noted in the opening, however, one data point troubling some economists is increasing unemployment and the factors surrounding the change:

- “What concerns me is when we see such an increase in the unemployment rate, it tends to trend higher, – Blerina Uruci, chief U.S. economist at T. Rowe Price.

- “The unemployment rate edged higher to 3.9%, which itself is not concerning given our expectation for ongoing softening… However, the reason for the uptick is more problematic: labor force participation backtracked for the first time since April, and employment as reported by the household survey swung significantly negative.” – Dante DeAntonio, senior director at Moody’s Analytics

- Bloomberg economists concurred: “The biggest signal from the report was the uptick in the unemployment rate— that outweighs the significant slowdown in headline nonfarm payrolls and large negative revisions, in our view.”

Several experts also acknowledged we are inching closer to triggering the “Sahm Rule”, which has until now proven to be a reliable predictor of recession. The rule was created by former Federal Reserve economist Claudia Sahm, and considers the start of a recession the point at which the three-month moving average of unemployment rises by a half-percentage point or more relative to its low during the previous 12 months. Ms. Sahm, for her part, has publicly commented she’d be quite happy to see her measure break in this environment: “Everyone who is a macroeconomist, including myself, has made some very big errors thinking about the economy since the pandemic showed up.” Per the “Sahm Rule,” we’re now at the point where recession risks are elevated, although not yet at the point where it’s likely that a recession has already begun.

In the decade before the pandemic (a period that notably included the lengthiest stretch of labor market expansion), monthly job growth averaged about 180,000. October’s payroll gains continue a 34-month streak, the fifth-longest job growth on record. And considering there are still about 1.5 open jobs for every unemployed person, there’s room for continued growth. Perhaps the most concise synopsis of last month’s report might come from Nick Bunker, head of economic research at Indeed: “[October]’s jobs report is consistent with both a mild loosening of the labor market on the way to a soft landing, and potentially the beginning of a more troubling downturn.”

Hopefully, the softer October jobs report is welcome evidence of the economy’s cooling. Officials now surmise that borrowing costs are elevated enough to pressure economic growth, and voted to leave them unchanged in last week’s meeting. Chair Jerome Powell also hinted we may be finished with rate hikes, provided we continue to see reduced labor demand in the coming months.

Naturally, plenty more data is needed to predict the path forward, as Minneapolis Fed President Neel Kashkari noted last Friday. While moderating job growth is a good sign, it remains just one piece of data. Future data will be eyed with scrutiny by the Fed: In case you haven’t noticed, our forecasting hasn’t been that great in the last few years, and so we just need to keep watching the actual data.”

As ever, our highly unusual economy continues to leave experts scrambling to make sense of it all. Last fall, a majority of experts were predicting imminent recession. Fast forward to 2023 and opinions are quite mixed. In a recent CNBC survey of economists and market analysts, 49% said that they still expect a recession in the next 12 months, while 42% predict a soft landing. Goldman Sachs suggests that while a recession may be in the future, the onset is delayed as “fiscal policy continues to do the heavy lifting.”

While I don’t have all the answers, I suppose we’ll do what we always do: stay on our toes and adapt and learn with each new report.

“A rock-solid American jobs market rolls on albeit at a moderating pace…Income gains continue to outpace inflation, which bodes well for consumption heading into the traditional holiday spending season.”

–Joe Brusuelas, chief economist at accounting firm RSM

(Sources: Economic Policy Institute, CNN, The Conference Board, New York Times, CNBC, Yahoo Finance, Bloomberg Ben Cassleman via LinkedIn, Bureau of Labor Statistics, Reuters, Fortune, KMPB, Indeed Hiring Lab)

What else?

What Else for November?

- X (née Twitter) commentary on the October jobs report from the EPI here and here.

- A favorite read from last year, updated for the next: Accenture’s Life Trends 2024, a set of predictions on which trends will impact business and society in the year ahead.

- Over the past several years we have seen the rise, fall, and reinvention of the Chief Diversity Officer (CDO) position. We’ve gone from the heralded “diversity tipping point” and one of the hottest jobs in human capital, to roles threatened by poor design and intense DEI backlash. This Fast Company article looks at five realistic scenarios facing companies reevaluating their DEI efforts.

- New research finds that nearly 50% of employees view their current job performance as unsustainable and only 50% of them actually trust their employer. Learn more how these trends are influencing HR in Gartner’s Top 5 Priorities for HR Leaders in 2024 and see what else is top of mind for CHROs today.

- Some interesting thoughts on the “most important” recruiting metric you’re probably not measuring: Time to Alignment.

- Another lens on the return to office mandate debate: why do organizations think employees perform more poorly when working from home, when in fact the data shows the opposite? It’s because managers lack the skillset to evaluate the performance of remote workers, ranking them lower while expressing dissatisfaction with flexible work practices.

- Not a surprise, new research from the Pew Research Center finds that more than 4 in 10 US workers only take some of their paid time off.

- And because you didn’t know you needed it, an illustrated guide to the world’s most beautiful cows.

(Sources: Economic Policy Institute, Accenture, Fast Company, Gartner, John Vlastelica via LinkedIn, Fortune, Pew Research Center, The Washington Post)