Economic Update: October 2023

Change State Friends,

Change State Friends,

First things first – I wish a spooktacular October to all those who celebrate

. Did you know that the origin of the “trick or treat” tradition may have emerged from an older Germanic Christmas custom where children would disguise themselves and shout “belsnickel!” to attempt to procure treats from neighbors? Read more about that, along with other fun facts about Halloween, if you are interested. Whether September’s jobs data is a trick or a treat, well, that’s up for some debate. Let’s get into it.

. Did you know that the origin of the “trick or treat” tradition may have emerged from an older Germanic Christmas custom where children would disguise themselves and shout “belsnickel!” to attempt to procure treats from neighbors? Read more about that, along with other fun facts about Halloween, if you are interested. Whether September’s jobs data is a trick or a treat, well, that’s up for some debate. Let’s get into it.

Cheers,

Nicole

Economic Snapshot

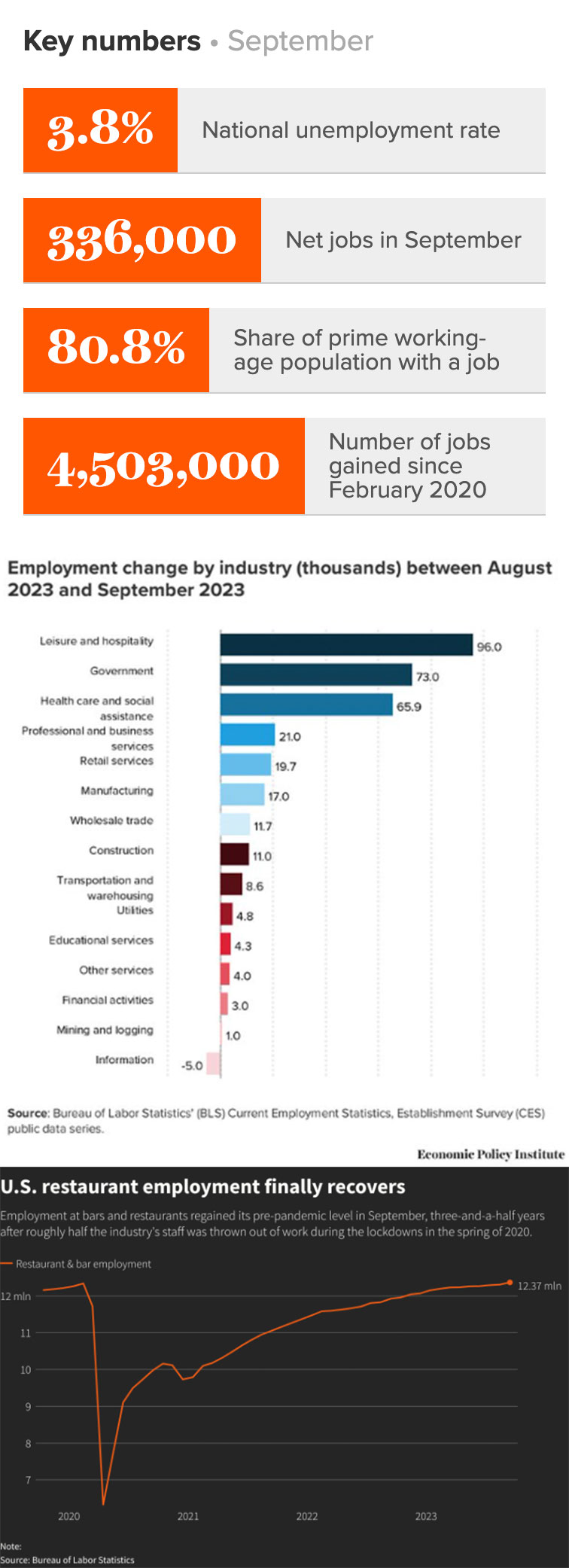

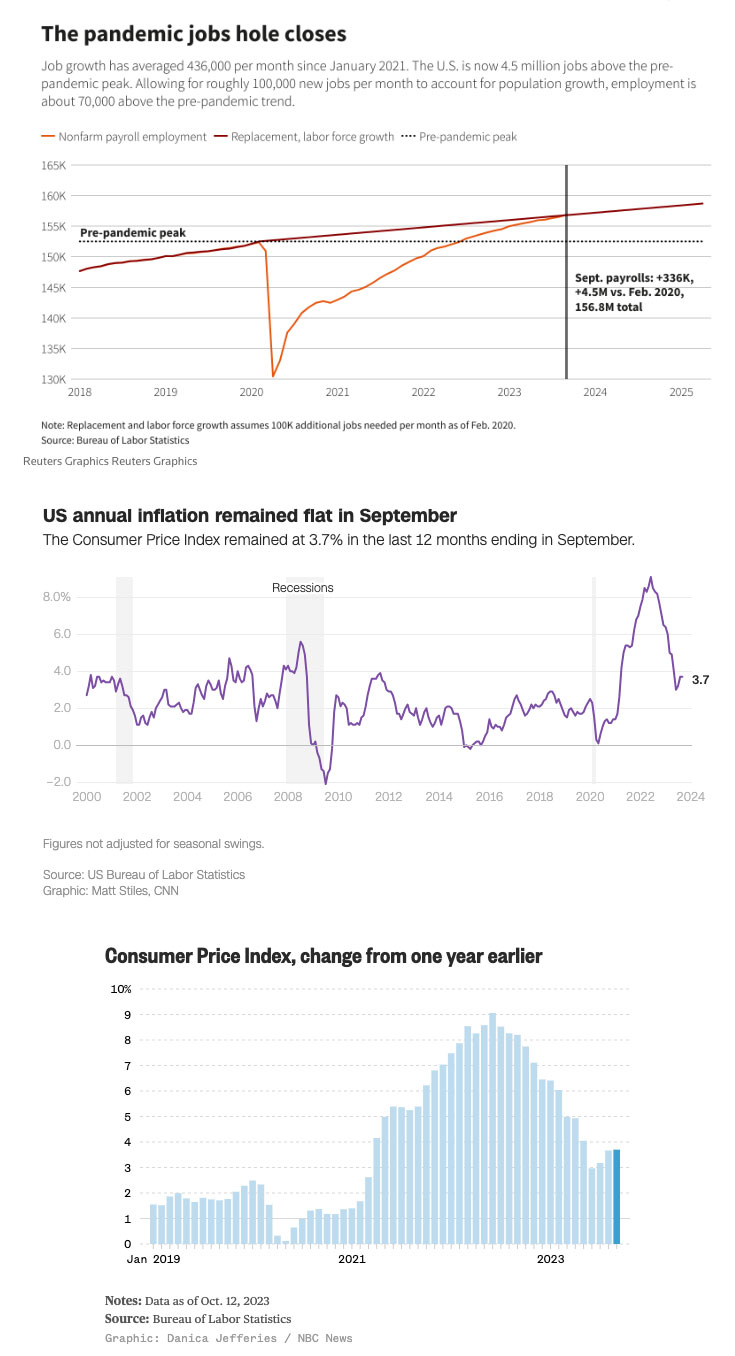

September’s jobs report certainly had a few surprises up its sleeve: U.S. employment increased by the greatest amount seen in eight months to 336,000 – nearly twice the number widely anticipated. Economists polled by Reuters had expected job growth of only 170,000 in September. Not to be outdone, the July and August job totals were also revised upwards by 119,000, flip-flopping the slowdown trend and becoming a likely headache for Fed officials. By way of benchmark, the economy needs to create roughly 100,000 jobs per month to keep up with population growth. Unemployment held steady in September at 3.8%, along with employment to population ratio and the labor participation rate. Men’s EPOP remains just shy of its pre-pandemic peak and women’s prime-age EPOP continues to surpass pre-pandemic rates.

September’s biggest winner: the restaurant industry! U.S. restaurant employment reached pre-pandemic levels in September for the first time in three-and-a-half years. Food service employment was among the most devastated by the COVID-19 pandemic: employers in the industry lost 6 million workers in March and April 2020 as patrons shifted towards dining at home. Yet, while the food industry has seen a boon in recent months, leisure and hospitality overall retains an employment deficit since the pandemic.

September’s hiring boom upended expectations of a slowdown driven by interest rates, inflation, the resumption of student loan repayments, and rising oil prices. Instead, the numbers suggest the economy picked up steam through the summer, no doubt boosted by continued consumer spending: “It was a blockbuster jobs report, but just as important was how well-rounded hiring was,” said Robert Frick, Navy Federal Credit Union’s corporate economist. The breadth of hiring also thumbed its nose at recent arguments made that job gains were too narrowly focused on healthcare and social assistance, as last month’s job gains saw nearly every industry adding workers.

Many experts are rejecting the suggestion that the bombshell report is indicative of an unsustainable jobs market. Acting U.S. Labor Secretary Julie Su noted that Q3’s average employment gain of just over 266,000 was far below last year’s pace of more than 400,000. “This is no longer … overheated,” she said. “It is strong, stable growth.” Indeed’s economic research director Nick Bunker added: “Underlying this report is a labor market that is still incredibly resilient…I think it’s the sign of a labor market that has sustainable strength moving forward.”

At the same time, the report continues to complicate the picture for the Fed: job growth is moving apace, wage growth remains contained, hiring is rebounding in industries that have been expected to soften, and an expanding labor force has held unemployment flat. The Fed’s expectations for the last 18 months of rate increases has assumed that hikes should cool demand for goods and services, and companies would naturally pull back on hiring, attempting to avoid widespread layoffs by cutting the number of vacancies. And yet, astonishingly, the opposite appears to be happening. Consumer spending remains strong, and the number of job openings rose in August, from 8.9 million to 9.6 million.

Inflation tapered off to 3.7% in September compared to last year, continuing the trend of a gradual slowdown. Prices rose less in September than in August when inflation sped up again after the cost of gasoline had spiked 10% in July. There are signs inflation is easing, but it’s not happening very fast, and inflation is still well higher than the Fed’s widely publicized 2% target. Promisingly though, while overall inflation sped up due to increased fuel costs, the Fed’s preferred measure of inflation has slowed.

Slowing wage growth may also help to appease economic policymakers, as average hourly earnings rose 0.2% after a similar rise in August. That lowered the annual increase in wages to 4.2%, likely because most of the jobs added last month were in lower-paying industries. Many believe that monitoring wage growth is a key trend to follow to interpret the Fed’s next move. Deceleration of wages coupled with high demand for workers suggests there remains additional labor supply to be unlocked. Job gains of this magnitude are large enough to draw more workers into the labor force, even as wage growth continues to moderate.

The labor market also faces new headwinds. Although the federal government avoided a September shutdown, which could have hurt the economy, another looms in November, with no clear path forward to solving government funding issues.

The Fed left interest rates alone last month but cracked the door open to make one more rate move in 2023. Popular opinion suggested “a majority” of Fed officials believed one more hike would be necessary, while others advocated to stay the course, knowing that soft landings are rare, and wanting to remain attentive to risk to the overall economic outlook. They also indicated that they would leave interest rates at a high level for a long time, lowering them perhaps only modestly in 2024. Officials also highlighted the autoworkers’ strike as a new economic threat with the potential to both increase inflation and slow overall growth. (“Fun” fact: as of August, the U.S. had lost more working days to labor disputes in 2023 than in any year since 2000).

September’s report briefly rattled stock and bond markets, before making a comeback. That’s notable as Wall Street has been repeatedly surprised by the strength of jobs reports in recent months, increasing investor skepticism on peak interest rates and how long the Fed may maintain its tightening policy. The about-face also continues to fuel debate on whether good economic news is good or bad for stocks.

Financial markets and many economists believe the Fed is probably done hiking rates because long-term U.S. Treasury yields have jumped to a decade-plus high. “If financial conditions, which have tightened considerably in the past 90 days, remain tight, the need for us to take further action is diminished,” commented San Francisco Fed President Mary Daly. But the unexpectedly strong jobs report may cause others to err more on the side of caution. Cleveland Fed President Loretta Mester suggested she would support raising rates on Nov. 1 “if the economy looks the way it did…at our recent meeting.”

The “goldilocks economy” continues to defy all odds and expectations, and the Fed will meet two more times in 2023 to decide its fate.

“The knee-jerk reaction to September’s surprisingly hot nonfarm payroll is that the Fed may have to hike more — but the details favor another interpretation. Household employment is weak, and the soft increase in wages and flat hours worked suggest labor-market conditions are not quite so rosy.”

– Bloomberg economists Anna Wong, Stuart Paul and Eliza Winger

(Sources: Economic Policy Institute, The Washington Post, Reuters, Restaurantbusinessonline.com, The Wall Street Journal, NPR, The New York Times, NBC News, CNN, Indeed, Fortune, AP News, Yahoo Finance, Bloomberg)

What else?

What Else for October?

- X (néeTwitter) commentary on the September jobs report from the EPI here.

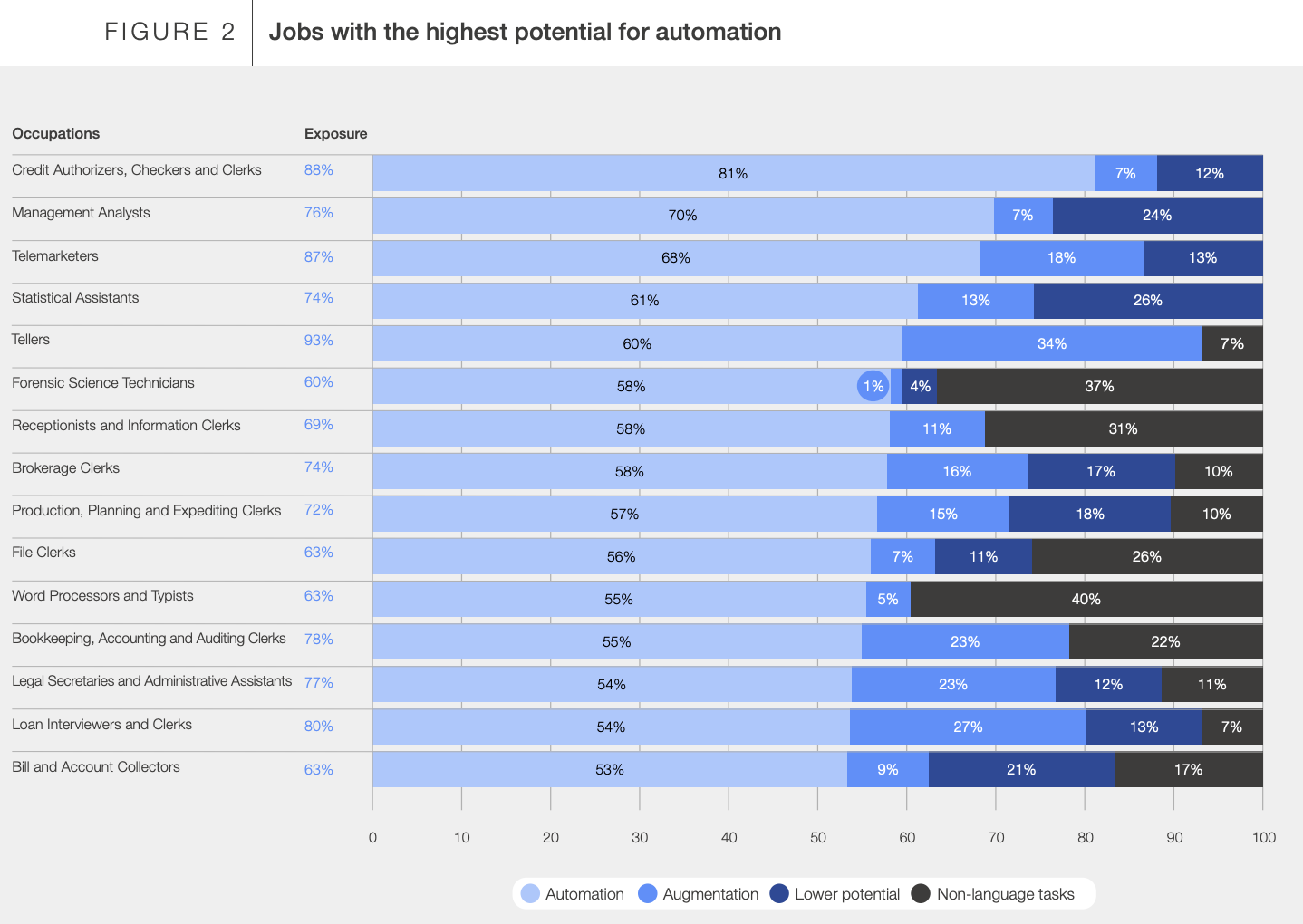

- A new report from the World Economic Forum explores the direct impact of Generative AI, specifically Large Language Models (LLMs), on various jobs and tasks.

- Despite increased scrutiny at home, with geopolitical tensions rising against China, many uber-wealthy Gen Z graduates are repatriating to begin their careers – another indicator of the decoupling of the world’s two largest economies.

- Meanwhile, China’s Great Resignation is just getting started: according to a recent survey, nearly 30% of employees quit their jobs between Jan-Oct 2022, and young workers are increasingly so burnt out they’re also throwing resignation parties.

- Some new research on setting expectations for in-office work suggests focusing on “moments that matter” over setting a minimum number of office days per week. Read more to understand the three scenarios where in-person connections offer distinct advantages.

- Around the world, only one in eight workers has one or more green skills, and demand continues to outpace supply. Check out LinkedIn’s 2023 Global Green Skills Report for more insights.

- No pay, no play. A recent study by Gartner found that nearly 50% of job applicants won’t apply if a pay range is not listed in the job description.

- As noted in last month’s update, working women with children under four are largely fueling the nation’s increasing labor force participation rate. When federal funding ends and threatens to close nearly 70,000 childcare centers, what will happen to the gains they’ve made?

- More bad news for women: more women than men stand to lose their jobs to AI and automation by the end of the decade.

- A blast from the past: could cargo ships go wind-powered to dramatically cut emissions?

(Sources: Economic Policy Institute, The World Economic Forum, Bloomberg, CNN, Microsoft, LinkedIn, Human Resource Executive, The Hamilton Project, The Washington Post, NPR)