Economic Update: September 2023

Change State Friends,

Happy September! Are you and your family as gratefully back to school as we are? As much as I lament the premature end to summer, a predictable schedule (child care!) and cooler temps are most welcome. If you don’t have school-age children, but are looking to support working parents, here are some suggestions from Human Resources Executive to help ease the transition.

Oh, and Change State has forthcoming exciting “back to school” news to share, soon. Stay tuned!

Cheers,

Nicole

Economic Snapshot

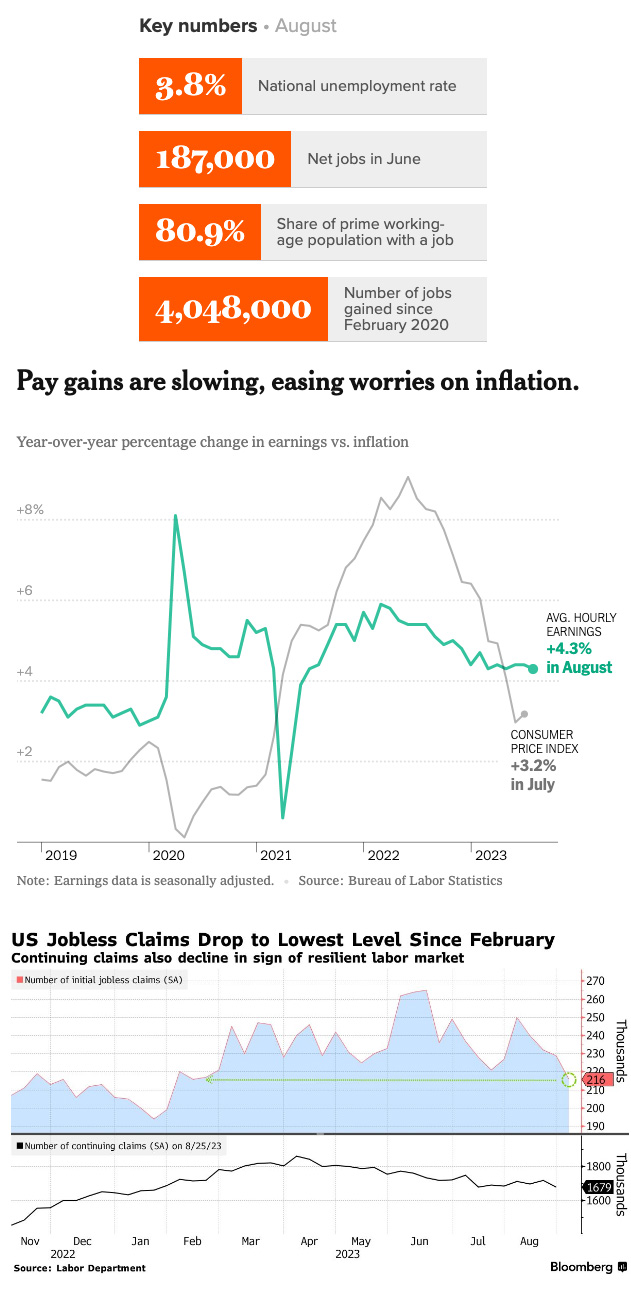

The latest report showed 187,000 jobs added in August with the unemployment rate jumping from 3.5% to 3.8% – more than was generally expected. That’s for a “good” reason however, as the raise is explained by an unusually large rise in the number of people looking for work, though unemployment remains well below average. LFPR ticked up to 62.8% and employment-to-population ratio (EPOP) has remained steady at 60.4%. Who is powering the continued labor force participation rate climb? Women, particularly those with children under 4! Notably though, the job growth figures for June and July were revised down by a combined 110,000 jobs, highlighting some weakness in the jobs reporting from earlier this summer.

The lion’s share of jobs growth for August was in health care and social assistance. The leisure and hospitality industry continues to recover (although it remains 290,000 jobs below its pre-COVID level) and construction growth has remained remarkably strong in light of persistently high interest rates.

The August report showed an increase of hourly earnings of 0.2%, or 4.3% annually. Fortunately for workers, wage gains are outpacing inflation, which continues to bolster purchasing power and hopefully sustain economic growth. That being said, wage increases are still floating above the 3.5% rate that the Fed believes is more in line with their inflation reduction goals. “Wages have certainly slowed…but the degree of slowing we’ve seen is just achingly gradual,” said Jonathan Millar, the senior U.S. economist for Barclays. Unemployment benefits applications dropped to the lowest level since February – decreasing by 13,000 to 216,000, well under levels projected by Bloomberg.

Though it may be “achingly gradual”, we are still trending towards a slowdown. July’s downward revision was at least partially attributed to some unexpected events like the SAG-AFTRA strike in Hollywood and trucking industry layoffs following the bankruptcy of Yellow Corp. Some of the trucking slowdown is also a post-COVID industry right-sizing as transportation grew to serve stay-at-home shopping and has now contracted over time.

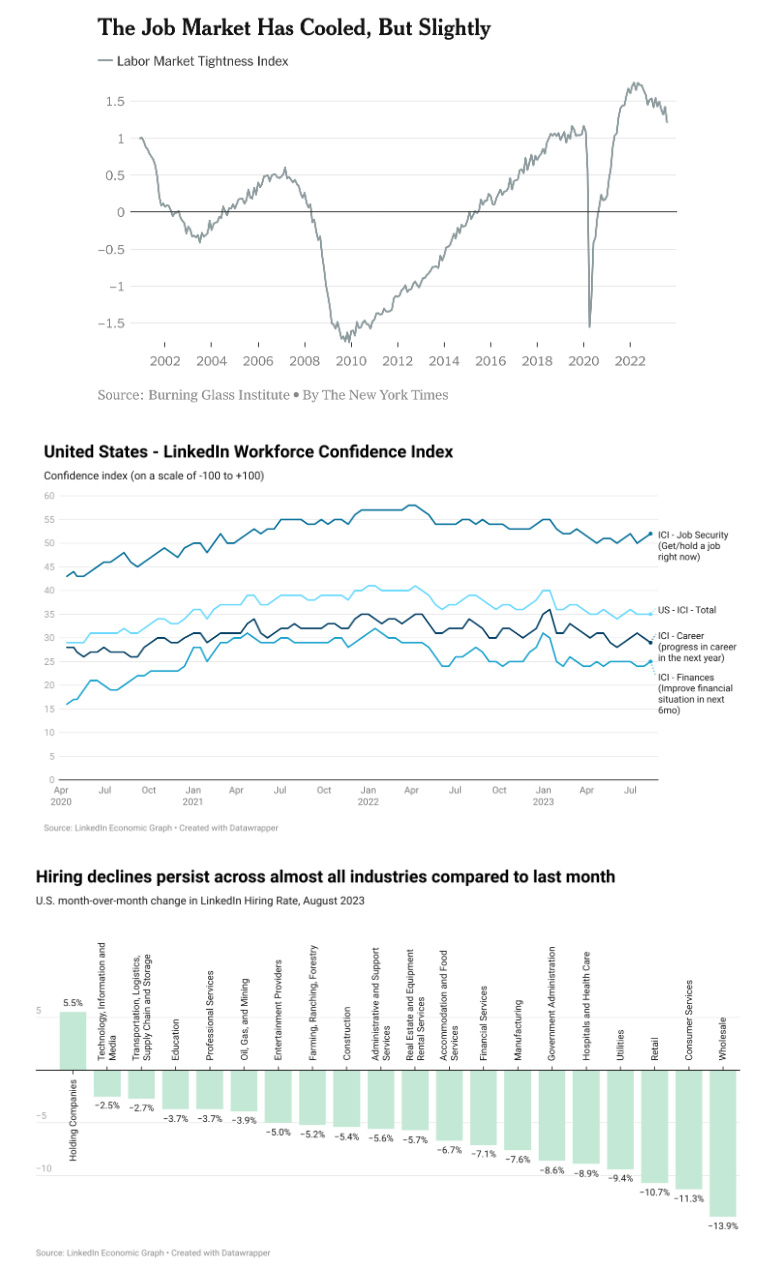

Hiring demand is also diminishing, primarily due to companies electing to reduce the number of open positions rather than enacting layoffs. With a decrease in job openings in the US alongside an uptick in job seeker search activity, we are clearly moving towards labor market softening. According to LinkedIn, hiring in the US declined across almost all industries in August 2023, dropping 3.6% over July. Pascal Michaillat, an economist at the University of California, Santa Cruz, measures labor market tightness by comparing job vacancies with the number of unemployed: in a balanced market, these numbers should be equal. The ratio fell to 1.4 in August from 1.6 in July, indicating a labor market that has loosened but remains uncomfortably snug.

So how do people actually feel about the economy? The reality has been a somewhat complicated about-face over the last several months. A year ago when fears of recession were at a fever pitch (cheekily dubbed the “vibecession”), some asked: could our negative talk actually manifest a recession? Reflecting on today, we might find that the opposite is true and perhaps we might be talking ourselves out of a recession. There’s evidence that firms are more concerned about being unprepared for an economic boom than they are a downturn. If that’s a good assumption, then we should see companies hold onto both workers and goods, a phenomenon that should hold off any sustained downturn.

An alternate possibility is that decreased hiring is just the first stage of weakness: labor hoarding also has a tendency to disguise labor market vulnerability. As banks have made lending terms more rigorous, American debt is also increasing. Many student loan repayments resume in October, and there’s still uncertainty over the ultimate lasting impact of the Fed series of rate hikes. If the durability of the American consumer fails, layoffs could increase rapidly.

And just when we think things couldn’t get more odd – there’s even a possibility that the economy slows or even shrinks, all with employment remaining low. “It never happened before[…] (b)ut theoretically it is possible, and I think now it is as close as we ever got to it” noted Gad Levanon, the Burning Glass Institute’s chief economist.

Many economists and investors do not expect an increase to come at the Fed’s next meeting on Sept. 19-20, but it is not entirely off the table. Fed Chair Powell recently emphasized slowing jobs growth and slowing pay gains as signs that the labor market is recalibrating. “We expect this labor market rebalancing to continue,” but it “remains incomplete”.

In interviews after the last meeting, other Fed presidents shared diverse opinions on the path forward:

- New York President John Williams: US monetary policy is “in a good place […] We’ll have to keep watching the data carefully analyzing all of that and really asking ourselves the question: is this sufficiently restrictive”?

- Dallas President Lorie Logan: skipping an interest-rate hike at the upcoming meeting may be appropriate, “but skipping does not imply stopping.”

- Atlanta President Raphael Bostic: “What I’m grateful to say is we’ve seen inflation come down […] I feel like we’re in a restrictive space now. And now we just need to let that restriction play out.”

- Chicago President Austan Goolsbee: “We are very rapidly approaching the time when our argument is not going to be about how high should the rates go […] it’s going to be an argument of how long do we need to keep the rates at this position before we’re sure that we’re on the path back to the target”

As the Fed circles in on the end of their contractionary policies, Mr. Goolsbee is probably right – the debate is beginning to shift from how high-interest rates need to go to how long they should stay elevated. Goldman Sachs Group economists anticipate the Fed will start lowering interest rates by the end of June 2024. A Bloomberg survey showed many are split on when the first cut will occur. Nearly 25% of participants predicted a reduction in January 2024, while the median estimated the first cut in March.

“The labor market was sprinting last year and now it’s getting closer to a marathon pace […] A slowdown is welcome; it’s the only way to go the distance.”

– Nick Bunker, head of economic research at Indeed

(Sources: Economic Policy Institute, Human Resources Executive, The New York Times, The Brookings Institution, The Washington Post, CNBC, USA Today, CNN, The Wall Street Journal, Reuters, Bloomberg, LinkedIn, Forbes, The Federal Reserve, Business Insider, Yahoo Finance)

What else?

What else for September?

- X (née Twitter) commentary on the August jobs report from the EPI here.

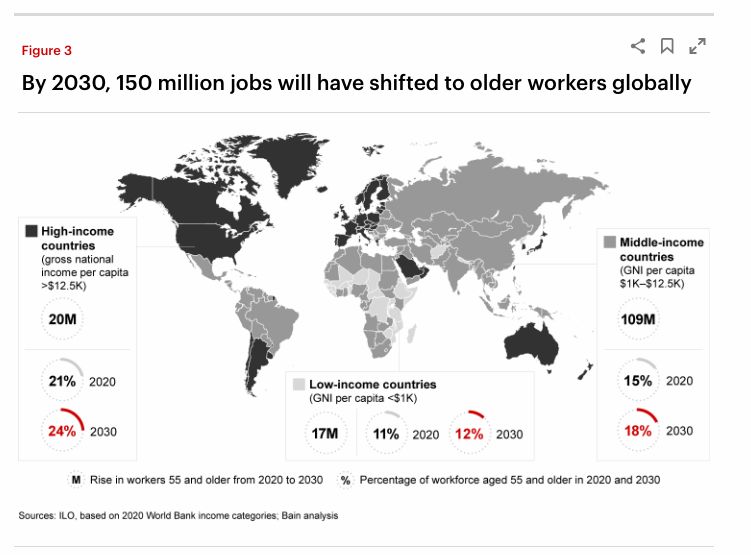

- With an aging population worldwide, more and more jobs will need to shift to older workers. Not only that, but data suggests age-diverse firms are lower in turnover and higher in productivity. Read more insights on how to recruit and retain older workers from Bain.

- On the other end of the spectrum, stimulus money is drying up and nearly 70,000 childcare centers are expected to close in the coming weeks – a disaster for working parents and the livelihoods of caregivers.

- Read LinkedIn’s August Future of Work Report, focusing on the intersection of AI and the world of work.

- The Conference Board’s recent publication highlights the importance of striking the right balance between return to work, hybrid and remote: the report reveals that 71% of organizations mandating their on-site work policy reported difficulty retaining workers.

- Opinions about hybrid work differ globally – HBR shares some insights for how to navigate this as a multinational organization.

- The summer of 2023 was a difficult one in climate change news – record-breaking heatwaves, wildfires, and more. How will our changing climate affect the way we work?

- Could autonomous taxis become one of the most important economic innovations of all time, potentially impacting global gross domestic product (GDP) by 20% over the next decade?

(Sources: Economic Policy Institute, Bain & Company, The Washington Post, LinkedIn Economic Graph, The Conference Board, Harvard Business Review, BBC, Ark-Invest)